Before we dive into how to improve your CIBIL score, let’s briefly explore why CIBIL scores even exist in the first place. A CIBIL score is essentially a credit report – the record of a business’s financial health. It helps lenders like banks or NBFCs ascertain the creditworthiness of a business and decide on whether or not to sanction loans.

In countries around the world, there exist credit bureaus which produce credit reports and credit scores. They do this based on a set of parameters like the business’s repayment of loans, overall value of debts and its length of credit history.

Some popular credit bureaus in India include Equifax, CRIF High Mark, CIBIL, and Experian, of which CIBIL is the most widely accepted.

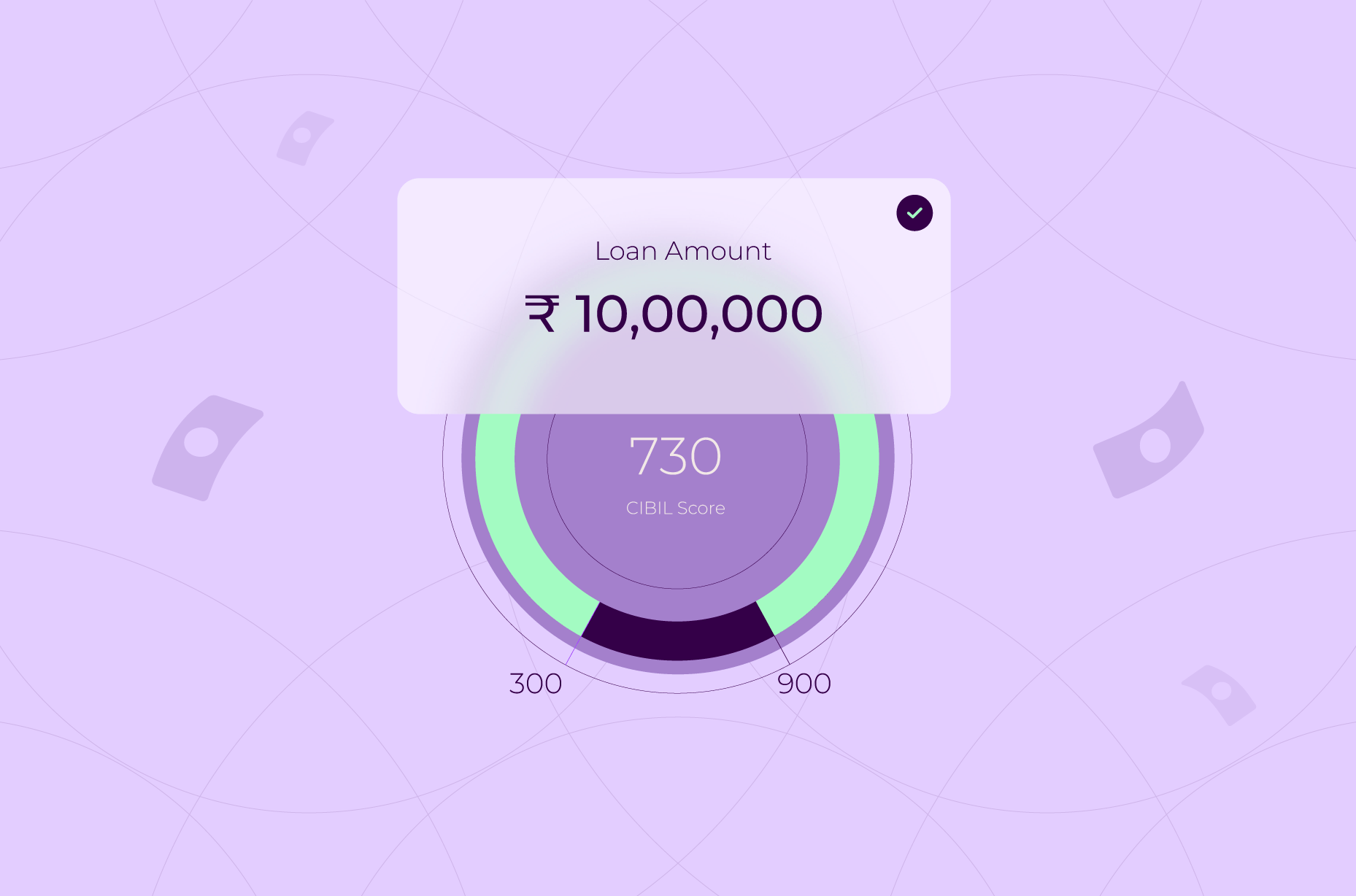

A CIBIL score ranges from 300 to 900. A score between 550 to 700 is considered fair, while that above 750 is considered good. Whether you’re a business looking to expand your operations, buy new equipment or hire across teams, a favourable credit score is what you should aim for. It not only signals a higher loan eligibility but with a strong score, your business can also get lower interest rates and better loan deals.

But for whatever reason, if your score falls below the mark, there are measures you can take to improve your CIBIL score. Take time to understand the factors that influence your CIBIL score and keep working on them consistently to reach your target score.

Here’s how to improve your CIBIL score to get loans without hassles:

Nothing succeeds like discipline

When it comes to maintaining a clean credit history, repayment of outstanding debt is necessary. Delay in EMI payment incurs penalty and decreases your credit score. Set good habits around repayment of debts, perhaps even have a monthly reminder in place to make sure that the bills are paid on time.

Opt for a loan tenure that matches your ability to repay

One of the common mistakes that many businesses make is misjudging their ease of loan repayment. Opt for a longer loan tenure if it allows you to relieve some of the pressure around paying back the borrowed amount. It allows you to spread out your EMIs and pay in smaller instalments over a longer period of time.

Stay below your credit limit

Yet another disciplining measure, it is good practice to avoid utilising your full credit limit. Put a cap on your credit usage every month and try as best as possible to stay within the limit you’ve set for yourself. As a rule of thumb, restrict your credit usage to 30% of the limit allotted to you.

Maintain a longer, fuller credit history

Businesses’ needs are diverse and so are their spending habits in various situations. Maintain old credit cards and previous credit histories to average out any small misses in payments. Over a longer period, minor lapses in credit repayment are often overshadowed by positive credit behaviour. Moreover, you may also consider creating a richer credit history by choosing different forms of credit.

Keep a check on taking on too much debt at once

For growing businesses, debt is often essential, but it is also important to take on the right kind and amount of debt. Although it is conventional wisdom to take small loans, business exigencies might require a decision to take on a debt amount larger than the business can comfortably pay off. But this can weigh heavily on a business later on and so it is always useful to err on the side of caution and not take too much debt at once.

Check CIBIL for mistakes

Like any other records, those from credit bureaus can also be subject to errors. Track your company’s credit scores from time to time as even small errors or discrepancies can impact your credit score. Should you notice any mistakes or inaccuracies – like high credit utilisation, bounced cheques, or loan defaults – report it to CIBIL and get it updated at the earliest.

To Sum up

A CIBIL score is built over time as your business progresses and creates a map of its financial behaviour. Improving a credit score overnight is not possible, since it takes time to build a track record. But with structures in place, you can encourage positive habits around credit limit setting and debt repayment. Over time, consistency and timely repayment will help improve your CIBIL score and you will surely find your business and yourself in a more favourable position.

Open offers a cutting-edge solution for easy loan application for SMEs such as yours, covered in 3 simple steps, and trusted by 30,00,000 businesses around India.

Support your business dream with instant loans. Explore Open Capital Loans below.