Every business transaction doesn’t always go as planned. When customers return products, dispute charges, or receive incorrect invoices, businesses need a systematic way to handle these adjustments. This is where credit notes come in – a critical financial document that helps businesses manage and record these changes professionally.

In high-volume businesses, even small billing errors can create reconciliation gaps and compliance risks. Credit notes help enterprises systematically manage these adjustments while maintaining clean financial records and audit trails.

Let’s explore the credit note meaning, its significance, and how it contributes to smooth business operations.

What is a Credit Note?

A credit note, also known as a credit memo, is a commercial document issued by a seller to a buyer that reduces or eliminates the amount the buyer owes. Think of it as a negative invoice – if you need to subtract money from what a customer owes you, you will issue a credit note.

In simple terms, if you’re wondering what is credit note, it is a formal way to reduce or adjust an invoice while keeping records accurate and aligned with tax requirements.

This document serves as formal proof of the adjustment and ensures both parties maintain accurate financial records.

When is a Credit Note Issued?

Several business scenarios require the issuance of a credit note:

- Returns of goods under GST: When customers return goods due to quality issues, damage, or incorrect specifications, sellers issue credit notes to adjust the original invoice amount.

- Invoice errors: If an invoice contains pricing mistakes, quantity errors, or calculation discrepancies, a credit note corrects these inaccuracies.

- Post-Sale discounts: When sellers offer discounts after sending the original invoice, they document these changes through credit notes.

- Service cancellations: In cases where prepaid services are canceled or modified, businesses use credit notes to refund or adjust the charged amount.

Why Credit Notes Matter for Enterprises

- High-volume transaction management: Enterprises handle thousands of invoices, making manual adjustments inefficient.

- Reconciliation accuracy: Credit notes ensure proper matching across invoices, payments, and settlements.

- Audit readiness: Every adjustment is documented with a clear trail.

- GST compliance at scale: Helps avoid mismatches in returns and reduces compliance risks.

Essential Components of a Credit Note

A properly formatted credit note should contain the following key elements:

- Original invoice reference: Clear mention of the invoice number being adjusted to maintain a clear audit trail.

- Business information: Complete details of both the seller and buyer, including registered names, addresses, and tax identification numbers.

- Transaction details: Date of issuance, reason for the credit note, and itemized list of adjustments.

- Financial information: The credited amount, any applicable tax adjustments, and the total revised amount.

- Unique identification: A distinct credit note number for easy tracking and reference.

How Credit Notes Impact Accounting & Tax Compliance

Accounting Impact:

- Reduces accounts receivable for the seller

- Decreases accounts payable for the buyer

- Affects revenue recognition in financial statements

- In enterprise setups, credit notes must sync across ERP systems, accounting platforms, and payment systems to avoid reconciliation gaps.

Tax Implications:

- Adjust GST obligations accordingly

- Helps maintain compliance with tax regulations

- Provides necessary documentation for tax audits

- Under GST, credit notes must be reported in returns to adjust output tax liability, while buyers must reverse input tax credit accordingly. Delays or errors can lead to mismatches at scale.

Credit Notes in Automated Financial Workflows

- Automatically adjust invoices in accounting systems

- Trigger reconciliation updates across platforms

- Sync with payment settlements

- Reduce manual intervention and errors

As businesses scale, automation ensures credit notes are accurately tracked across systems without delays or discrepancies.

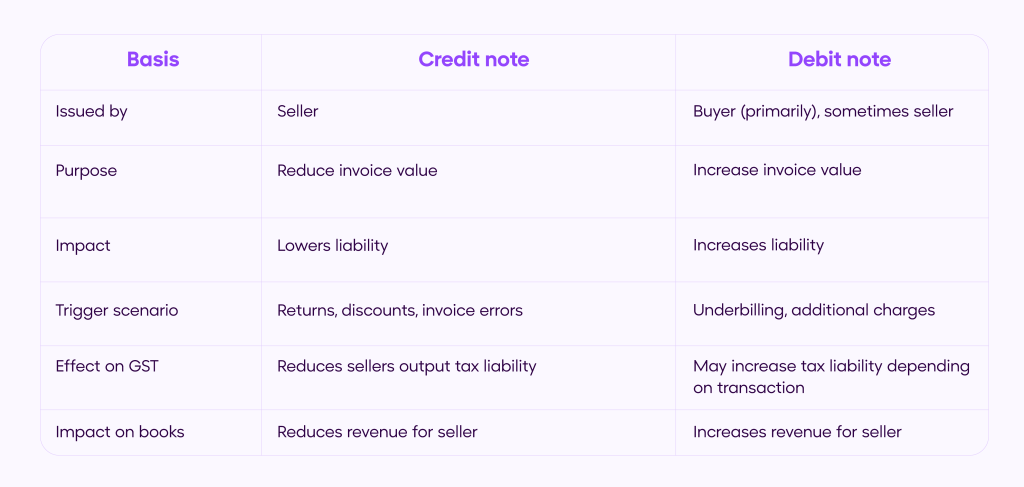

Credit Note Vs. Debit Note: What is the Difference?

A credit note, often called a credit memo, essentially works as a negative invoice. When a seller issues a credit note, they’re acknowledging that they owe money back to the buyer or are reducing the amount the buyer needs to pay. Think of it as a way to subtract from an existing bill.

On the other hand, a debit note functions as an additional charge document. When a buyer receives a debit note, it means they owe more money to the seller than what was originally invoiced. It’s like adding to an existing bill.

Understanding these differences is crucial for proper bookkeeping and maintaining healthy business relationships. While both documents adjust transaction values, they work in opposite directions – credit notes reduce obligations while debit notes increase them for the recipient (buyer) and increase receivables for the issuer (seller).

In practice, these documents help businesses maintain accurate financial records while providing a clear audit trail of all adjustments made to original invoices. They’re particularly important for tax compliance and reconciliation purposes, ensuring transparency in all financial dealings between parties.

A credit note is issued by a seller to reduce the amount a buyer owes due to returns, discounts, or invoice corrections. A debit note is typically issued by a buyer to request a reduction in the amount payable due to discrepancies or returns. Additionally, A debit note is not always sent by the buyer—in some cases, a seller may issue it to correct underbilling.

Also Read: What is a Debit Note? Meaning, Uses & Importance

Why Credit Notes are Important?

1. Financial Accuracy

Credit notes help businesses keep accurate financial records by tracking all payment adjustments and corrections. This ensures proper financial reporting and helps monitor cash flow effectively.

2. Regulatory Compliance

These documents fulfill legal requirements for financial record-keeping and tax purposes. They provide necessary proof during audits and help businesses maintain transparent operations.

3. Customer Relations

Credit notes show professionalism in handling billing adjustments, which builds customer trust. They help resolve payment issues quickly and maintain good customer relationships.

Conclusion

Credit notes are essential for any business today. They’re official documents that help fix billing mistakes and adjust payments. When you know how to use them properly, it helps maintain accurate records and follows all the rules. Plus, they make it easier to handle customer refunds and adjustments professionally. Using credit notes the right way helps your business run smoothly and keeps your customers happy.

FAQs

1. What do you mean by a credit note?

A credit note (also called a credit memo) is an official document issued by a seller to a buyer to reduce or correct the value of a previously issued invoice. It is typically used in cases such as product returns, pricing errors, or post-sale discounts. In simple terms, it acts like a negative invoice, ensuring that both financial records and tax reporting remain accurate.

2. What is a credit note vs a debit note?

A credit note is issued to reduce the value of an invoice, while a debit note is used to increase it. In simple terms, a credit note lowers the amount payable, whereas a debit note adds to it, helping businesses correct or adjust transactions accurately.

3. Is it mandatory to issue a credit note for every return?

Yes, for business transactions, issuing a credit note for returns is typically required for proper accounting and tax compliance.

4. When should a credit note be issued?

A credit note should be issued when you need to cancel or reduce an invoice amount, fix billing mistakes, process refunds, or adjust prices for returned goods. Issue it as soon as you spot the need for a change.

5. Is a Credit note & Credit memo the same?

Yes, a credit note and credit memo are the same thing – they’re just different names for a document that shows a reduction in the amount a customer owes. Both serve the same purpose of documenting credits, refunds, or adjustments to an invoice.