Key Takeaways

- AP automation fixes documents, not money: Traditional AP software is a pre-payment tool. It brilliantly streamlines invoice approvals but completely ignores the actual execution of funds.

- Fragmentation is a control risk: Once an invoice is approved, forcing finance teams to jump into separate bank portals and treasury systems creates massive gaps for errors, duplicate payouts, and reconciliation nightmares.

- Connected Banking bridges the gap: Integrating your bank accounts directly into your AP workflow gives you a single dashboard to view real-time balances, auto-sync statements, and execute payments instantly.

- AI requires unified workflows: The future of autonomous, agentic finance cannot exist in a fragmented tech stack. AI can only govern and optimize what is actively connected from invoice receipt to final settlement.

Accounts payable automation has become a standard line item in enterprise finance transformation roadmaps.

The promise is familiar: centralize invoice processing, reduce manual effort, and bring structure to approval workflows. At the process level, it delivers. Invoices move faster. Approval chains are documented. Data is more consistent across entities.

Modern AP systems also go further, reducing duplicate invoices, improving data accuracy, and enabling near real-time visibility into invoice status and approvals.

But once an invoice is approved, finance teams often find themselves back in the same place, manually coordinating payments across banking partners, managing exceptions through email chains, and reconciling transactions across ERPs and spreadsheets.

At enterprise scale, this is not a minor inefficiency. It is a systemic control problem.

The limitation is not in execution, but in scope.

AP automation improves how invoices move. It does not control how money moves.

What AP Automation Was Built to Do

AP automation software digitizes and streamlines the invoice-to-approval workflow. It handles invoice capture and data extraction, multi-level approval routing, validation checks, and audit logging.

For enterprises managing high invoice volumes across multiple business units, this is a meaningful operational upgrade. Processing costs decrease. Cycle times shorten. Visibility into approvals improves.

It also strengthens process accuracy—helping reduce duplicate invoices, standardize data, and create reliable audit trails within the workflow.

But AP automation is a pre-payment tool. It was designed to manage the flow of documents—not the flow of funds. Everything that happens after approval sits outside its scope.

Where the Control Gaps Begin

The assumption that automating AP workflows eliminates financial risk is one of the most persistent misconceptions in enterprise finance.

Automation significantly improves efficiency and accuracy within invoice processing. But if the broader system remains fragmented, gaps still exist beyond the workflow.

At enterprise scale, those gaps have real consequences.

Payment execution happens outside the system

After approvals are completed, finance teams move to bank portals, treasury platforms, and file-based payment runs. The disconnect between approval and execution is where control can weaken.

Errors shift, rather than disappear

AP automation reduces invoice-level errors. However, risks can still arise at the payment stage—such as incorrect transfers, duplicate payouts due to process gaps, or misrouted transactions across systems.

Real-world variation introduces complexity

Enterprises operate across vendors, geographies, and formats. While AP systems handle structured workflows well, inconsistencies across systems can still create exceptions that require manual intervention.

Reconciliation remains a separate effort

Across entities, cost centers, and banking relationships, reconciliation often happens outside the AP system. ERP updates, payment tracking, and audit consolidation still require coordination across tools.

The Fragmented Enterprise Finance Stack

Large enterprises operate across a constellation of disconnected systems:

- AP platforms for invoice management

- Treasury systems for cash visibility

- Multiple banking portals for payment execution

- ERP instances for accounting

- Spreadsheets to bridge the gaps

Each system performs its function in isolation. None operates as a unified workflow.

At scale, this fragmentation creates compounding challenges—financial leakage, inconsistent controls across geographies, limited real-time visibility, and audit processes that require significant manual effort.

This is not just an operational issue. It is a governance and compliance risk that grows with the business.

Why This Is a More Urgent Problem in 2026

Finance is evolving rapidly. The industry is moving toward AI-driven, agentic systems—platforms that can reason across workflows, detect anomalies, and execute with minimal human intervention.

That shift is real. But the organizations that will benefit most are those that have already solved a more fundamental problem: connected, controlled workflows from invoice to payment.

AI cannot govern what is not connected. Autonomous finance only works when data, approvals, and execution exist within the same system.

Before AI can deliver value, the workflow must be unified.

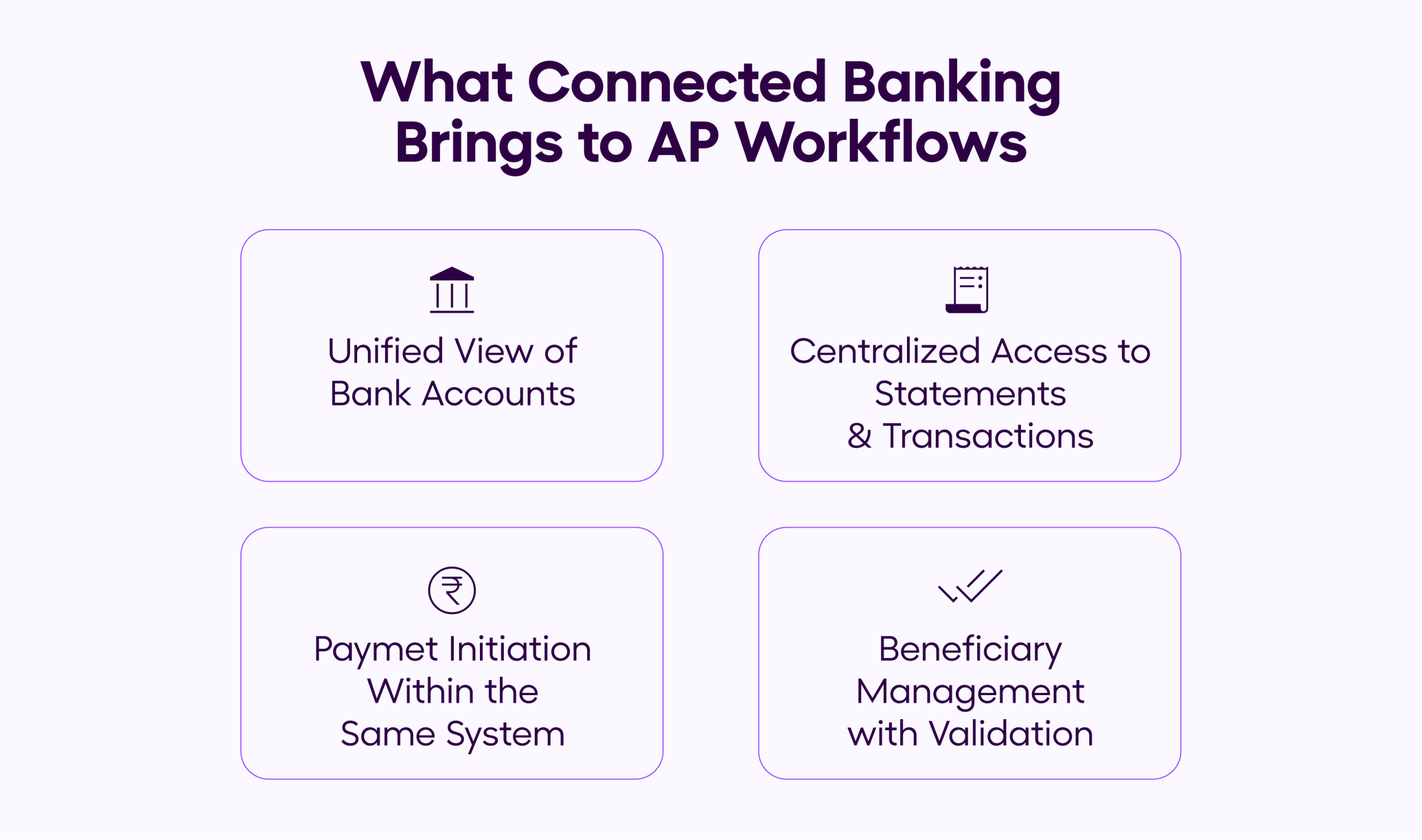

What Connected Banking Brings to AP Workflows

AP automation improves how invoices are processed.

Connected banking brings payments and visibility into the same system.

This reduces the dependency on multiple banking portals and manual tracking.

At a practical level, connected banking enables:

1. Unified View of Bank Accounts

Finance teams can view balances across multiple bank accounts within a single interface.

- All connected accounts in one place

- Clear identifiers for each account

- Support across major banks (ICICI, HDFC, Axis, SBI, and others)

This improves visibility without switching between banking platforms.

2. Centralized Access to Statements and Transactions

For each connected account, teams can:

- View transaction history (credits and debits)

- Access account statements

- Download data from the date of connection

This removes the need to log into multiple bank portals for reporting and tracking.

3. Payment Initiation Within the Same System

Instead of moving to a bank portal after approvals, finance teams can initiate payments directly.

- Select debit account

- Choose beneficiary

- Enter the amount and payment mode

- Add remarks and execute

Transactions initiated are recorded within the platform, improving traceability.

4. Beneficiary Management with Validation

Connected banking includes a centralized beneficiary layer:

- Add beneficiaries with account number and IFSC

- Auto-fetch and validate bank details

- Maintain a structured list for payments

This reduces manual errors during fund transfers.

What This Actually Solves

Connected banking does not replace AP systems.

But it reduces key operational gaps by:

- Bringing payment execution closer to workflows

- Improving visibility across bank accounts

- Creating a single system for tracking transactions

- Reducing reliance on multiple banking interfaces

How OPEN Enables Connected Banking for Enterprises

Closing the gap between AP automation and execution requires more than adding tools. It requires a system where workflows, payments, and visibility are naturally connected.

OPEN is built to provide that layer.

With OPEN, enterprise finance teams can:

- View and manage multiple bank accounts from a single interface

- Access statements and transaction data without switching platforms

- Initiate and track payments within the same system

- Manage beneficiaries with built-in validation

- Maintain a centralized record of payment activity

These capabilities reduce operational friction while improving visibility across financial workflows.

The Bottom Line

AP automation brought structure to invoice processing. But it did not solve how money moves, and at enterprise scale, that gap is where the real risk lies.

The industry is moving toward AI-driven finance. That future is worth investing in. But the foundation it requires is a connected workflow, one where execution and visibility are not fragmented across systems.

That is what connected banking begins to address.

And in 2026, for enterprises still managing payments across multiple disconnected platforms, it is one of the most practical and immediate upgrades they can make.