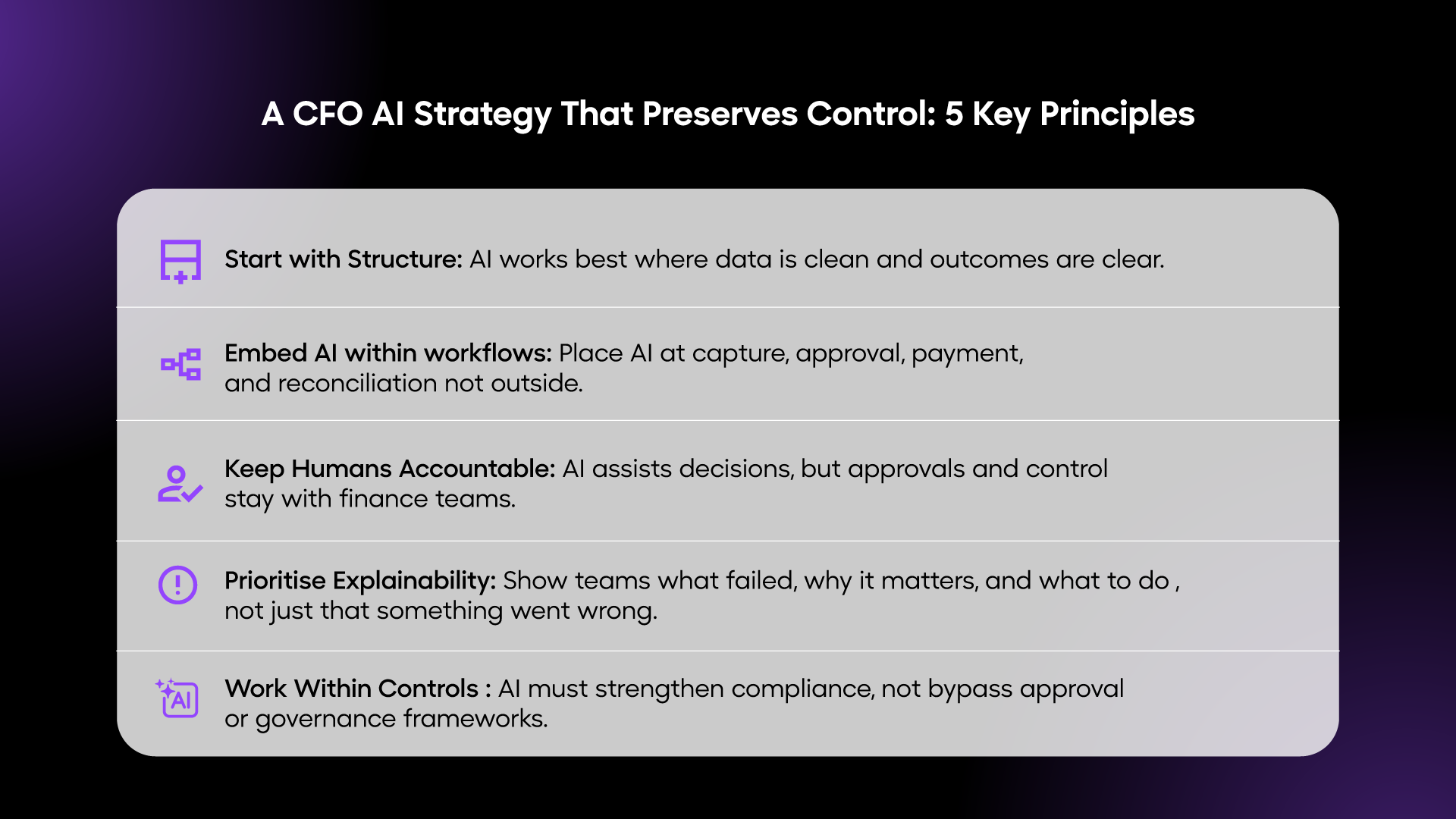

5 Key Principles for CFOs

- Start with Structure: AI works best where data is clean and outcomes are clear.

- Embed AI within workflows: Place AI at capture, approval, payment, and reconciliation — not outside.

- Keep Humans Accountable: AI assists decisions, but approvals and control stay with finance teams.

- Prioritise Explainability: Show teams what failed, why it matters, and what to do — not just that something went wrong.

- Work Within Controls: AI must strengthen compliance, not bypass approval or governance frameworks.

Most AI deployments in finance don’t fail loudly. They fail quietly—buried under unverified outputs, broken approval chains, and the slow erosion of financial trust.

Across the industry, a common concern is emerging: AI tools are being introduced into finance workflows, but control and accountability are not always keeping pace.

That concern is not irrational. It reflects a deeper shift in how financial systems are evolving.

Because the question in 2026 is no longer whether to adopt AI in finance. It is whether you can deploy it without introducing a new class of operational risk—one that is harder to audit, harder to explain, and harder to reverse.

This is the problem this playbook is designed to solve.

Why Finance Teams Resist AI (And Why They’re Right To)

Finance has never been an early adopter’s game. And for good reason.

The entire structure of a finance function is built on determinism: rules, hierarchies, approvals, and audit trails. Every output has an owner. Every decision has a rationale. Every exception has a process.

AI disrupts all of this – not because it is wrong, but because it operates differently:

- It produces probabilistic outputs, not deterministic ones

- It learns continuously, rather than following fixed logic

- It recommends actions, rather than executing defined rules

The result? Finance teams face a trust gap. Not in the technology itself, but in the operational layer around it.

When your team cannot answer the three questions below, AI adoption stalls – or worse, goes ahead without guardrails:

1. Can we trust the output?

2. Who is accountable when something goes wrong?

3. How do we audit a decision the system made?

Until those questions have answers, you don’t have an AI strategy. You have an AI experiment – and your balance sheet is the test environment.

The Hidden Cost of AI Layered on Broken Processes

There is a pattern I see repeatedly in organisations that rush AI adoption: they add AI on top of existing workflows rather than embedding it within them.

The result is a parallel system – one where work happens, and one where AI generates insights – and teams spend significant time manually reconciling the two.

More tools. Same workload. Higher verification burden. That is the opposite of transformation.

In India specifically, this creates acute risk. Regulatory requirements – GST compliance, vendor verification, payment audit trails – demand system-level accuracy. AI that operates outside these frameworks does not make compliance easier. It makes it harder.

The real risk of AI in finance is not that it replaces human judgment. It is that it creates the illusion of control while quietly eroding it.

The most effective finance leaders I’ve observed are not asking ‘Where can we use AI?’ They are asking a fundamentally different question:

Where can AI reduce verification effort without reducing financial control?

That shift – from capability to governance – changes everything about how AI is deployed. And for CFOs operating in India’s regulatory environment, it is not optional.

1. Start where rules are clear, and data is structured

AI delivers highest-confidence outputs where ambiguity is lowest. The right entry points are:

- Invoice data extraction and three-way matching

- Bank reconciliation and UTR mapping

- Anomaly detection in transaction patterns

- Vendor master verification (PAN, GSTIN, bank details)

Avoid starting with areas requiring subjective judgment – strategic forecasting narratives, M&A modelling, or scenario planning. These are high-value, but not the right place to build trust in a new system.

2. Embed AI within the transaction lifecycle – not outside it

AI tools that sit outside core workflows create reconciliation overhead. Instead, intelligence should be present:

- At the point of invoice capture – flagging discrepancies before they enter the system

- At approval – surfacing risk signals before sign-off

- At payment execution – validating vendor details in real time

- Post-transaction – reconciling automatically with payment references

When AI is inside the workflow, it enhances decisions. When it’s outside, it creates additional steps.

3. Maintain human accountability with system enforcement

AI should augment decisions – not replace accountability. CFOs must ensure:

- Approval hierarchies remain enforceable and cannot be bypassed

- Exceptions are flagged for human review, not auto-approved

- Every AI-assisted action generates an audit trail

- Escalation paths are clearly defined when AI confidence is low

The goal is not autonomy. It is controlled augmentation – where humans remain accountable, and AI makes that accountability easier to exercise.

4. Build trust through explainability, not just accuracy

Accuracy alone does not drive adoption. Explainability does.

Finance teams are more likely to act on AI outputs when those outputs tell them not just what happened, but why it matters and what to do next.

A well-designed system does not simply flag a mismatch. It tells you:

What failed: GST number on the invoice does not match the vendor master

Why it matters: Payment would violate input tax credit eligibility

What action is required: Hold payment and request a corrected invoice from the vendor

This kind of explainability turns AI from a black box into a decision-support layer – one your team can defend in an audit.

5. Align AI with existing financial controls – not around them

AI must operate within your governance framework, not as an exception to it. This means aligning deployments with:

- Existing compliance frameworks and internal audit requirements

- GST validation and filing workflows

- Vendor onboarding and KYC processes

- Payment approval matrices and delegation of authority

Any AI implementation that requires you to make exceptions to these controls is not yet ready for production.

AI Change Management in Finance: The Problem No One Talks About

Technology adoption is only half the equation. The other half is behavioural – and it is where most implementations of deploying AI across a finance team quietly fail.

Finance teams are not resistant to AI. They are resistant to uncertainty. The solution is not more training sessions. It is operational clarity.

The most effective deployments follow a phased trust-building approach:

Phase 1 – Assist: AI surfaces information; humans make every decision

Phase 2 – Augment: AI handles defined tasks; humans manage exceptions

Phase 3 – Optimise: AI improves decision quality; humans focus on strategy

Skipping phases does not accelerate adoption. It accelerates resistance.

Finance Automation Leadership: The Shift AI Demands from CFOs

Traditional finance automation asked: how do we do this faster?

AI-driven finance asks: how do we consistently make the right call?

That is a different problem. And it requires a different kind of leadership.

The CFOs navigating this best are making three transitions:

From tool adoption → System design

From efficiency metrics → Control metrics

From process ownership → Outcome ownership

AI is not a feature you deploy. It is an operational layer you design. And the CFO is the only person in the organisation with both the mandate and the visibility to design it correctly.

Before You Deploy: A CFO’s Pre-Flight Checklist

Before any AI deployment in finance operations, honestly assess the following:

Before deployment

- Is our financial data structured, consistent, and clean enough to produce reliable outputs?

- Are our workflows clearly defined with enforceable rules?

- Have we mapped which decisions AI will assist vs. which remain fully human?

During deployment

- Does AI operate within – not around – existing controls and approval hierarchies?

- Are outputs traceable and explainable to an auditor?

- Are exceptions routed to humans with clear escalation paths?

After deployment

- Has the manual verification burden decreased – or just shifted?

- Has financial predictability improved?

- Can we demonstrate compliance and control to auditors without additional effort?

If AI is increasing your oversight effort, it is not solving the right problem.

The Bottom Line

Intelligence in finance is only valuable when it is reliable. And reliability requires design – not just deployment.

AI will define the next decade of finance leadership in India. The CFOs who win will not be those who adopted it fastest. They will be those who built it into a foundation of control, trust, and governance from day one.

The technology is ready. The question is whether the operational architecture around it is.

That architecture is yours to build.

How OPEN Enables Controlled AI Adoption in Finance

AI in finance cannot succeed in a fragmented environment. When data, approvals, payments, and reconciliation exist across disconnected systems, AI outputs lack context – and therefore reliability.

OPEN is built on a single principle: intelligence is only trustworthy when it operates inside a controlled financial system – not on top of one.

Most finance platforms give you tools. OPEN gives you an integrated financial operating layer – one where vendor onboarding, approvals, payments, and reconciliation share a single source of truth. When AI operates within that environment, every recommendation it makes is grounded in verified, complete data.

In practice, this means:

- Vendor data is verified before transactions are enabled – eliminating a category of payment fraud at the source

- Approvals are enforced at the point of execution – not as a downstream check, but as a precondition for payment

- Reconciliation is automated with UTR-level mapping – closing the loop between payment initiation and confirmation

- Compliance risks are surfaced in real time – GST mismatches, PAN discrepancies, and policy exceptions flagged before they become liabilities

- Audit trails are generated automatically – every AI-assisted action is logged, traceable, and explainable to your internal or external auditors

The result is an environment where AI does not sit on top of your operations – it operates within them. Intelligence enhances control instead of diluting it.

FAQs

What’s the biggest mistake CFOs make when deploying AI in finance?

Treating AI as a separate layer on top of existing workflows, rather than embedding it within the transaction lifecycle. This creates parallel systems that increase – not decrease – manual effort.

How do we maintain compliance while adopting AI?

By ensuring AI operates within existing control frameworks – not around them. Every AI-assisted action should generate an audit trail, and approval hierarchies must remain enforceable at the point of execution.

Where should we start with AI in finance?

Start with high-volume, structured, rule-based processes: invoice processing, bank reconciliation, anomaly detection, and vendor verification. These offer the highest confidence outputs with the lowest ambiguity – the right environment to build trust.

Why do finance teams resist AI adoption?

They resist uncertainty, not technology. The solution is operational clarity: defined accountability, phased rollout, and explainable outputs – not more change management workshops.

How long does it take to see ROI from AI in finance?

When deployed correctly – embedded in workflows with clear controls – organisations typically see a measurable reduction in manual verification effort within 60–90 days. Strategic value, such as improved financial predictability and faster close cycles, compounds over 6–12 months.