Ask any finance head at a multi-branch EdTech company what their most stressful week looks like, and they’ll describe month-end. Different branches. Different payment modes. Different bank portals. And somewhere in the middle of it all, a spreadsheet that’s already three days out of date.

Connected banking for EdTech exists to end exactly that. Instead of chasing collections branch by branch, a single-view banking approach pulls every transaction — UPI, NACH, net banking, payment links — into one live dashboard, reconciled in real time and visible to everyone who needs it.

This guide breaks down how it works, what to look for, and why getting the underlying banking infrastructure right matters more than adding another fee software layer on top.

What Is Connected Banking?

Connected banking links all your bank accounts, payment channels, and transaction data into a single operational layer. Instead of logging into separate bank portals for each branch or manually stitching together settlement reports, every account, every inflow, and every payout is visible and controllable from one place — in real time.

For multi-branch EdTechs, this is the infrastructure layer that makes everything else — fee collection, reconciliation, settlement routing — actually work at scale.

What Is Multi-Branch Fee Collection Management?

Multi-branch fee collection management refers to a centralized system that lets an EdTech company oversee, track, and reconcile fee collections across all its locations from a single platform rather than managing each branch’s finances in isolation.

The distinction matters. Most EdTechs start by solving the collection problem at the branch level: a payment link here, a payment gateway there. Each branch gets something working. What they don’t get is visibility at the head office level. Finance teams end up with ten working collection setups that produce ten separate data streams, none of which talk to each other without manual intervention.

A multi-branch fee collection system changes the architecture. Fee structures are defined centrally and pushed to all branches. Payments hit individual virtual accounts assigned per branch, student, or fee head. Reports roll up automatically. The head office doesn’t need to call each center to know what was collected today; it’s already there, updated by the minute.

According to the UDISE+ 2024–25 report by India’s Ministry of Education, the country has over 1.47 million schools and 246.9 million students. As EdTech companies scale to serve this population across cities and states, the gap between a branch-level collection setup and a connected financial infrastructure becomes a real operational bottleneck.

Why Fee Collection Across Branches Breaks Down

The problem isn’t that individual branches can’t collect fees. Most can, and reasonably well. The problem surfaces the moment you need a consolidated picture or when something goes wrong.

Here’s where multi-branch fee operations consistently break down:

No single source of truth for collections. When Branch A uses a payment gateway, Branch B uses a standing instruction mandate, and Branch C still receives demand drafts, there’s no natural aggregation point. Finance teams manually pull reports from each and stitch them together, a process that introduces lag, entry errors, and reconciliation gaps every single cycle.

Reconciliation is retroactive, not real-time. Most finance teams match payments against dues at the end of the week or month, not as transactions come in. That means defaulters go unidentified for days, and the cash flow picture the leadership sees is always a version of the past.

Fee structure inconsistencies across branches. When fee structures live in branch-level spreadsheets or ERPs instead of a central system, local teams often apply incorrect amounts, miss penalties, or offer unauthorized discounts. There’s no single place to push an update.

Settlement routing becomes a manual job. If tuition fees and transport fees need to be settled into different accounts or if a franchise model requires splitting collections between the parent company and the operator, someone on the finance team is doing that transfer manually. Every cycle.

This is where most EdTechs hit a ceiling—not due to weak collections, but because the underlying banking infrastructure can’t scale with them.

How Connected Banking Solves Multi-Branch Fee Collection

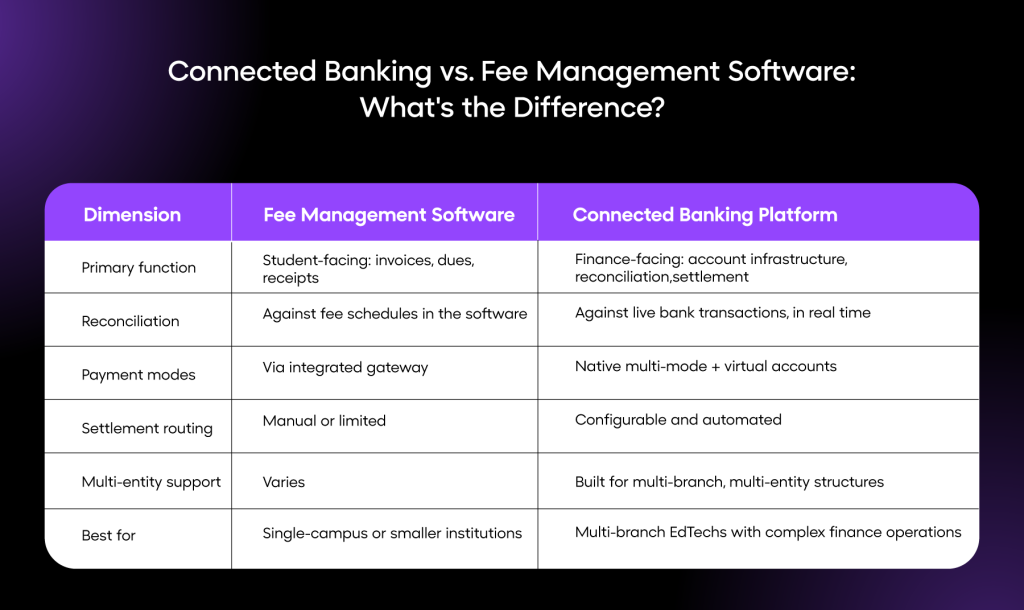

Fee management software and connected banking are often confused for the same thing. They’re not. Fee software manages the student-facing side — invoices, reminders, and due dates. Connected banking manages the financial infrastructure behind it, how money moves, where it lands, and how it’s reconciled against what was expected.

For a multi-branch EdTech company, the connected banking layer is where the real operational leverage lives:

1. Virtual Account Assignment per Branch or Student: Each branch, batch, or individual student is assigned a unique virtual account number (VAN). When a payment arrives, it’s auto-tagged — no manual matching required. Finance knows instantly who paid, from which branch, against which fee head, and whether it’s a partial payment or full settlement.

2. Unified Collection Across Banks and Payment Modes: Whether a payment comes in via UPI, NEFT, IMPS, net banking, NACH mandate, or a WhatsApp payment link, it flows into the same system — regardless of which bank it routes through. No separate silos, no bank-by-bank chasing.

3. Real-Time Branch-Wise Dashboard: Head-office finance teams see branch-level collection summaries live, not in a batch report that arrives 48 hours later. If a branch is underperforming against its collection target on the 10th of the month, that’s visible now, not after the cycle closes.

4. Automated Reconciliation Against Expected Dues: Rather than matching bank statements row by row, the system reconciles continuously against the fee schedule. Exceptions — failed mandates, partial payments, excess credits — surface automatically and are flagged for action, not buried in a spreadsheet.

5. Configurable Settlement Logic: Tuition fees can settle to one account, transport to another, and franchise remittances to the operator’s account — all from a single inflow. The splitting logic is defined once and runs automatically, eliminating inter-account transfers as a manual recurring task.

Key Features to Look For in a Connected Banking Platform for EdTech

Not every platform that calls itself a connected banking solution is built for the operational complexity of a growing EdTech. Evaluate on these dimensions:

| Capability | What to Actually Check | Why It Matters |

| Virtual Account Depth | Can VANs be created per student, per branch, and per fee head? | Eliminates manual payment matching across high transaction volumes |

| NACH / Auto-debit | Is e-mandate creation native or a third-party add-on? | Critical for EdTechs running EMI or instalment-based fee models |

| Payment Mode Coverage | UPI, NEFT, IMPS, cards, payment links — all in one? | Ensures consistent collection experience regardless of branch or payer preference |

| Automated Reminders | WhatsApp and email reminders triggered by due dates? | Reduces admin follow-up burden, especially in branches where one person handles multiple functions |

| Settlement Configurability | Can you define routing rules per fee type or entity? | Essential for multi-entity structures and franchise models with split settlements |

| ERP / LMS Integration | Webhook or API? What’s the data latency? | Prevents duplicate data entry and keeps fee records in sync across systems |

| Reversal Handling | Do failed mandates and refunds surface in real time? | Catches collection gaps before they compound into cash flow problems |

One question that rarely gets asked during vendor evaluation but matters significantly is: What happens when a mandate fails? Platforms that only flag failed NACH debits in a batch report, rather than triggering an immediate alert and retry workflow, silently cost EdTechs’ collection revenue every cycle.

Automated Communication: The Underrated Driver of On-Time Collections

The technology that runs the collection infrastructure matters. But so does what happens when a student or parent misses a due date.

One capability that sits outside most feature checklists but drives significant collection outcomes: automated communication. Reminders sent via WhatsApp and email at defined intervals before and after due dates can reduce the manual follow-up burden on branch administrators. In branches where a single admin handles fee collection alongside three other functions, automated outreach is the difference between a functioning collection process and a chaotic one.

The most effective communication setups are event-driven: a reminder fires when a due date is five days away, another when it passes, and a receipt is sent the moment payment is confirmed. No manual triggering. No dependence on a branch staff member remembering to send a message.

For EdTechs with a large student base spread across branches, this also standardizes the payment experience. Every branch delivers the same payment experience — same prompt, same link, same instant receipt — regardless of which admin happens to be on duty

How Open Enables Connected Banking for EdTech

Open gives multi-branch EdTech finance teams a single place to view balances, track transactions, and manage payouts across all bank accounts—eliminating the need to switch between multiple bank portals or rely on manual reconciliation.

- Unified visibility across accounts: Connect multiple bank accounts and view real-time balances in one dashboard, with clear identifiers for each use case—collections, payroll, refunds

- On-demand statements and history: Access transaction-level data anytime, filter by credits or debits, and download reports without waiting on bank requests

- Seamless, controlled payouts: Initiate refunds, faculty salaries, vendor payments, and franchise remittances from one place with OTP-based authorization and full traceability

- Verified beneficiary management: Add and validate recipients instantly using account number and IFSC, ensuring faster and error-free repeat transfers

- Clarity on data reliability: Distinguish between real-time synced accounts and those updated via offline methods, so finance teams always know what to trust

Connected Banking vs. Fee Management Software: What’s the Difference?

This distinction comes up often—and it’s worth being clear about, because choosing the wrong layer to invest in means you end up solving only half the problem.

The honest answer is that growing EdTechs need both, but the connected banking layer is what makes the fee software’s data trustworthy.

Without it, fee software shows you what students owe. Your bank shows you what actually came in. And reconciling the two becomes someone’s full-time job.

Conclusion

Multi-branch fee collection management isn’t a problem you solve once. It’s an infrastructure decision that either pays dividends as you scale or generates compounding friction as new branches, new fee structures, and new payment modes pile on.

Connected banking for EdTech addresses it at the right level — not by adding more software on top of a fragmented banking setup, but by fixing the underlying financial architecture so that every collection, from every branch, flows into one accurate and live picture.

If your finance team is still closing the books by pulling reports from multiple sources, the question isn’t whether to change the approach. It’s how quickly you can.

[Explore Open’s connected banking platform for EdTech →]

FAQs

What is connected banking for EdTech companies?

Connected banking is a financial infrastructure model where all bank accounts, payment channels, and collection points across an EdTech’s branches are linked into a single operational layer. It gives finance teams real-time visibility into collections, automates reconciliation, and enables configurable settlement routing—without logging into each bank or branch system separately.

How does branch-wise fee collection management work with virtual accounts?

Each branch, batch, or student is assigned a unique virtual account number (VAN). When a fee payment is made, it is routed to that VAN and automatically tagged with the corresponding branch code, student ID, and fee head. This eliminates the manual matching step that finance teams typically spend hours on during every reconciliation cycle.

What’s the difference between fee management software and connected banking?

Fee management software handles the student-facing side—invoices, reminders, due dates, and receipts. Connected banking handles the financial infrastructure behind it—how money moves, where it settles, and how it reconciles against actual bank transactions. Both are useful, but the connected banking layer is what makes the fee software’s data reliable at scale.

Can connected banking handle NACH and EMI-based fee collections?

Yes. Platforms with native NACH support automate e-mandate creation, debit scheduling, and failed-mandate alerts. This is particularly important for EdTechs running no-cost EMI or instalment-based fee models, where a failed debit that isn’t caught immediately can create a collection gap that compounds over time.

Is connected banking suitable for EdTechs with franchise or affiliate models?

It’s especially well-suited. Franchise models require collections to be split between the franchisor and franchisee accounts, often with different rules per location. Connected banking platforms with configurable settlement logic handle this automatically, so the inter-account transfer process that typically involves manual approval chains runs seamlessly in the background.