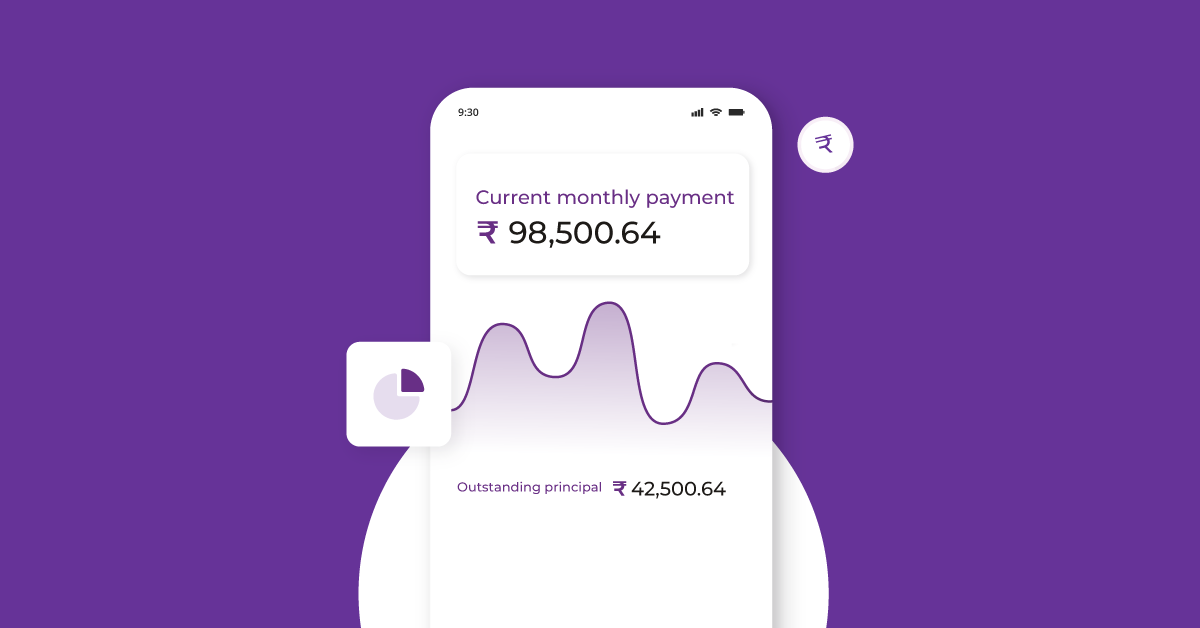

Daily, people’s lives are becoming increasingly automated as millions of algorithms make decisions and take actions on consumers’ behalf. The shift toward autonomous finance services starts with automated investment management, savings, and payments. Algorithm-based services lower the cognitive burden on users and strive to enhance financial results.

The customer experience (CX) has always been a priority for Financial Service Institutions (FSIs). However, in the wake of COVID-19, it has become a survival imperative and deprioritised CX, given the sudden impending need for digital services from clients. The FSIs set on the end of “business-as-usual” has left financial institutions scuffling with the twin challenge of conserving the financial health of their clients and preserving their own in a long period of financial uncertainty.

Financial Service Institutions are preparing for the year forward, and most realise that supporting customer retention is an intelligent bet. Research shows that building a customer-centric, digital-first financial institution is necessary, as customer-centric FSIs outshine their more-traditional counterparts. But what other trends should they pay close attention to that will help them stand out and keep their customers happy?

- 89 % of financial services leaders acknowledge that the first FSIs to deploy autonomous finance will carve out a sizeable competitive advantage and a niche for themselves;

- 60 % of financial institutions assume that autonomous finance improves personalisation and enhances customer experience (CX).

- As things stand right now, over 50 % of the finance and accounting activities are largely automated: processing transactions, procurement, preparing financial reports, planning/forecasts, etc.

Forrester Research defines autonomous finance as algorithm-driven financial services that make decisions or take action on a customer’s behalf.

Gaps in technology and customer expectations

We discussed in the previous blog how neobanks redefine the future of banking and how many traditional banks struggle to convert most of their offline services to digital ones. Traditional banks tied down with inflexible underpinnings have it even more difficult. Customers slowly begin to move towards fintech solutions that integrate their bank accounts with the facilitating neobank and provide all banking functions in one place.

“42 % of bank executives polled said that they were unsure about how to integrate and streamline office functions effectively from back to front, and 46 % said they are unsure how to embrace open banking, orchestrate the ecosystem or become a truly data-driven organisation.” – World Banking Report 2021.

Many customers switched as they felt that the traditional banks, with the immense resources available at their beck and call, could have given improved personalised services. The gap between the services offered by conventional banks and what customers expected from them widened.

Neobanks such as Chime, Open, and Affirm provide personalised solutions with the help of their partner banks. Partner banks such as Celtic Bank, ICICI Bank, and Green Dot Bank currently lead the pack in working with neobanks to deliver banking solutions. They are doing well by implementing autonomous finance to some extent; many, however, still struggle to capture the importance of serving excellent customer experience for long and sustainable growth. The pandemic has only made the gap between expectations and services offered.

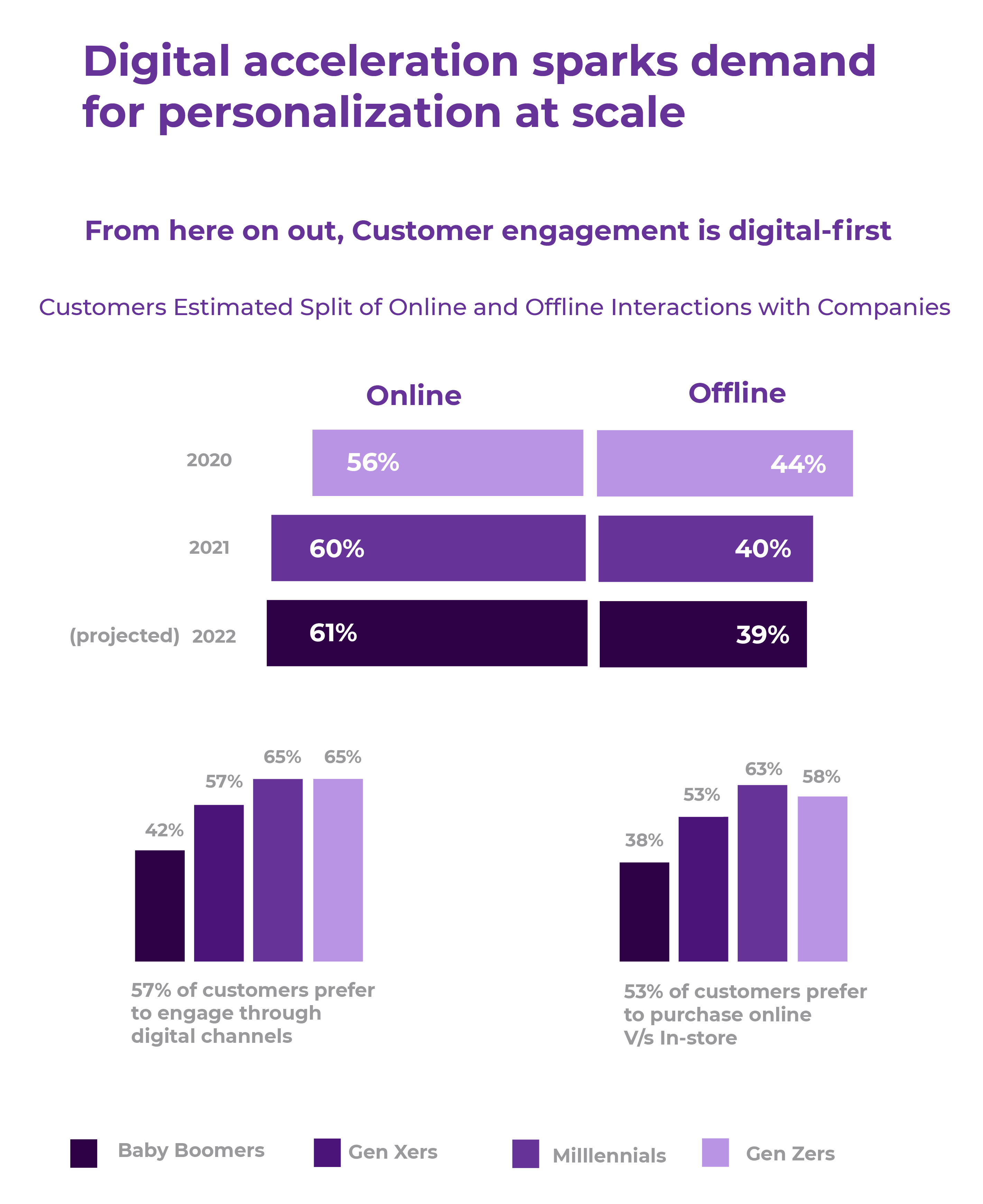

According to Salesforce, 68 % of customers’ expectations from digitally capable FSIs grew during Covid-19, yet many FSIs failed to meet the expectations. While rushing to meet customers’ fast-rising demands for digital services, FSIs pushed customer experience aside to implement new technologies to improve customer trust.

Filling the CX Gap: Long-Term vs Short-Term Goals

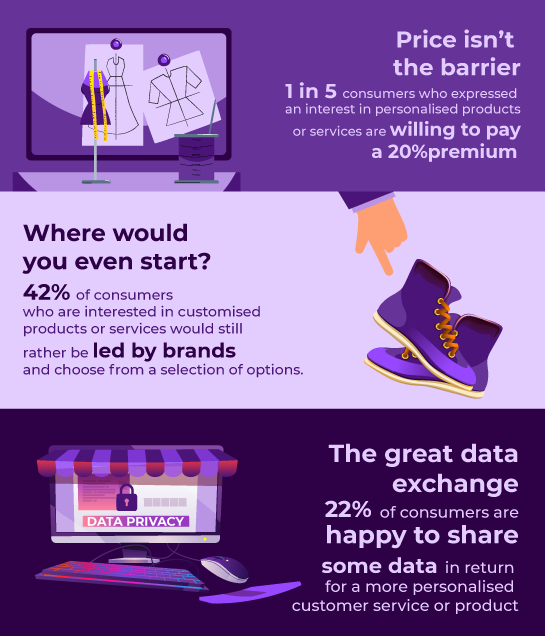

Business priorities change with time, but FSIs cannot ignore what customers want. Post-pandemic, customers have become increasingly critical of their expectations of the service the banks deliver and have become creators and critics who dictate what they want. Most customers are willing to pay a small premium to get personalised attention and services that cater to their needs.

Businesses need to understand that customers love attention like most other people. A puppy or a child would do anything to get attention from its parent, from messing around to throwing tantrums. Customers will do it by slowly ignoring the concerned business, which can cost them a lot in the long term. Therefore, companies must balance their short-term and long-term goals and activities and give customers well-deserved attention.

FSIs primarily indulge in two kinds of activities consistently:

- Stabilisers FSIs bend towards short-term activities that mitigate risks of urgent nature and focus on short-term wins.

- Growth-oriented FSIs focus on activities that build long-term relationships with customers.

Some FSIs are more focused on short-term goals than the long-term.

For example, the pandemic brought drastic changes in customer service request volumes for many FSIs. According to Asian Banker, large banks witnessed a 43.3 % increase in call volumes in 2020’s first quarter alone, with wait times averaging over 40 minutes. On average, customers use approximately nine channels, such as social media, web chats, emails, calls, etc., to connect with the FSIs to communicate their challenges. There are two ways to deal with it:

- Fix the issue, record it, and keep it safe. Then later, forget about it. (Stabilisers)

- Fix the problem, register it, learn from it, and make future-ready changes to the system so that no one ever faces the same challenges. (Growth-oriented)

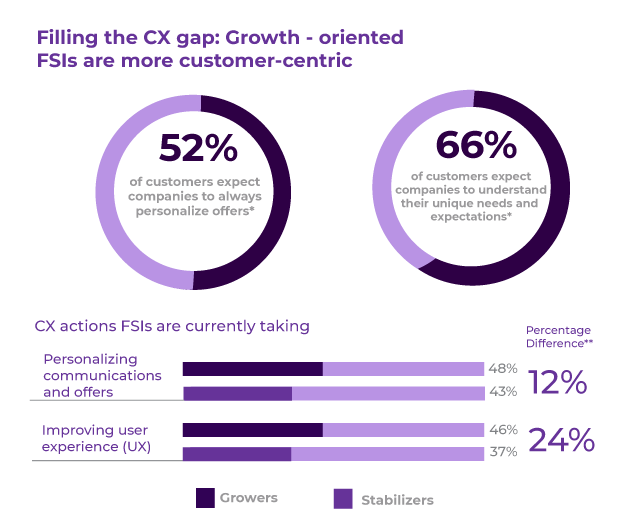

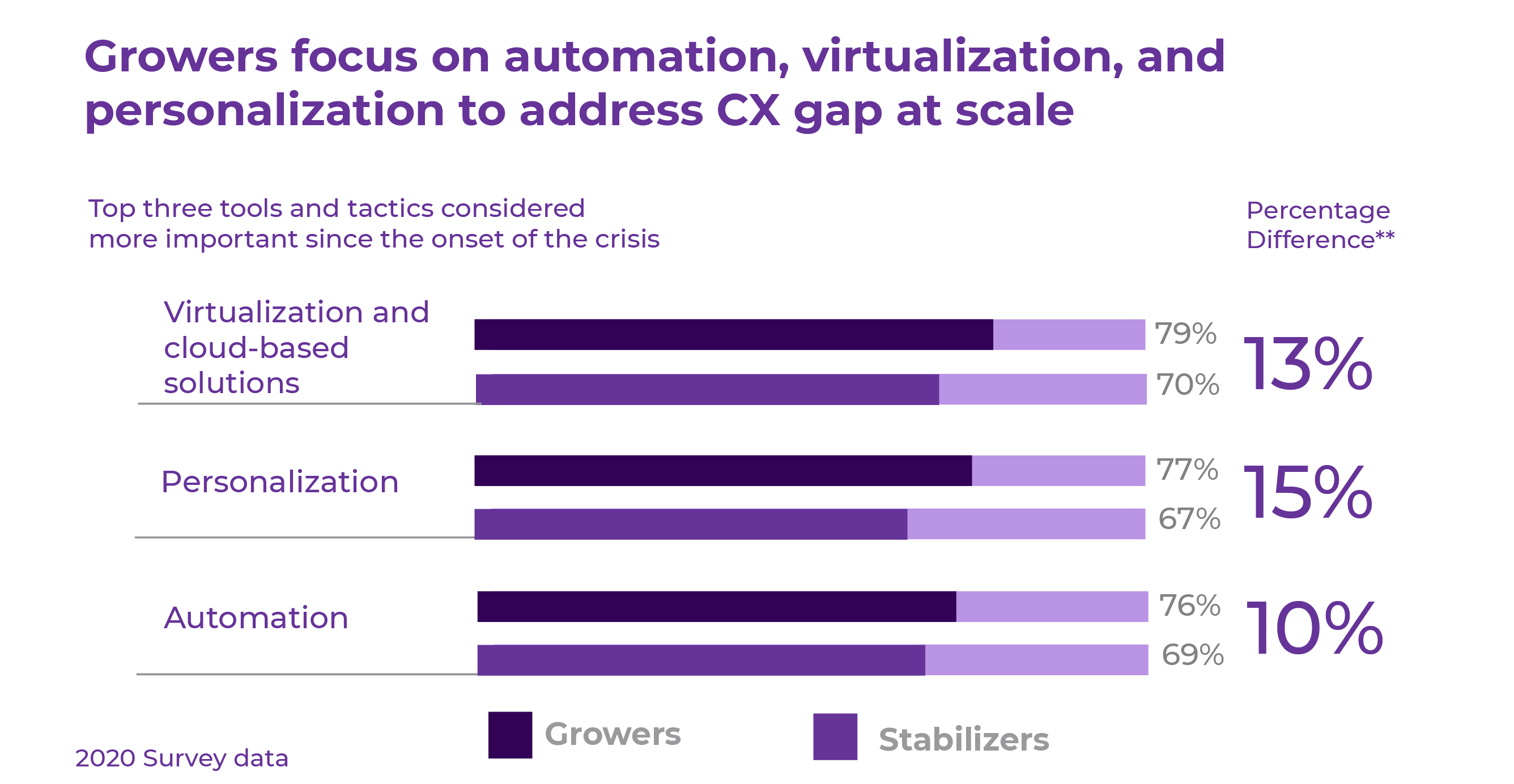

A type of fix FSIs choose for a problem is a choice they make based on their end goals which are again based on the mindset of the key stakeholders. Growth is something that all FSIs look for, but there are only a few that implement it. Comparing the stabilisers vs growth-oriented FSIs, the latter were 22 % more inclined to invest in omnichannel services and 15 % more likely to expand their support capabilities to new channels. Growth-oriented FSIs are 12% more likely than Stabilisers to personalise outreach and 24% more likely to improve their UX(Trends in Financial Services Report 2021, Salesforce).

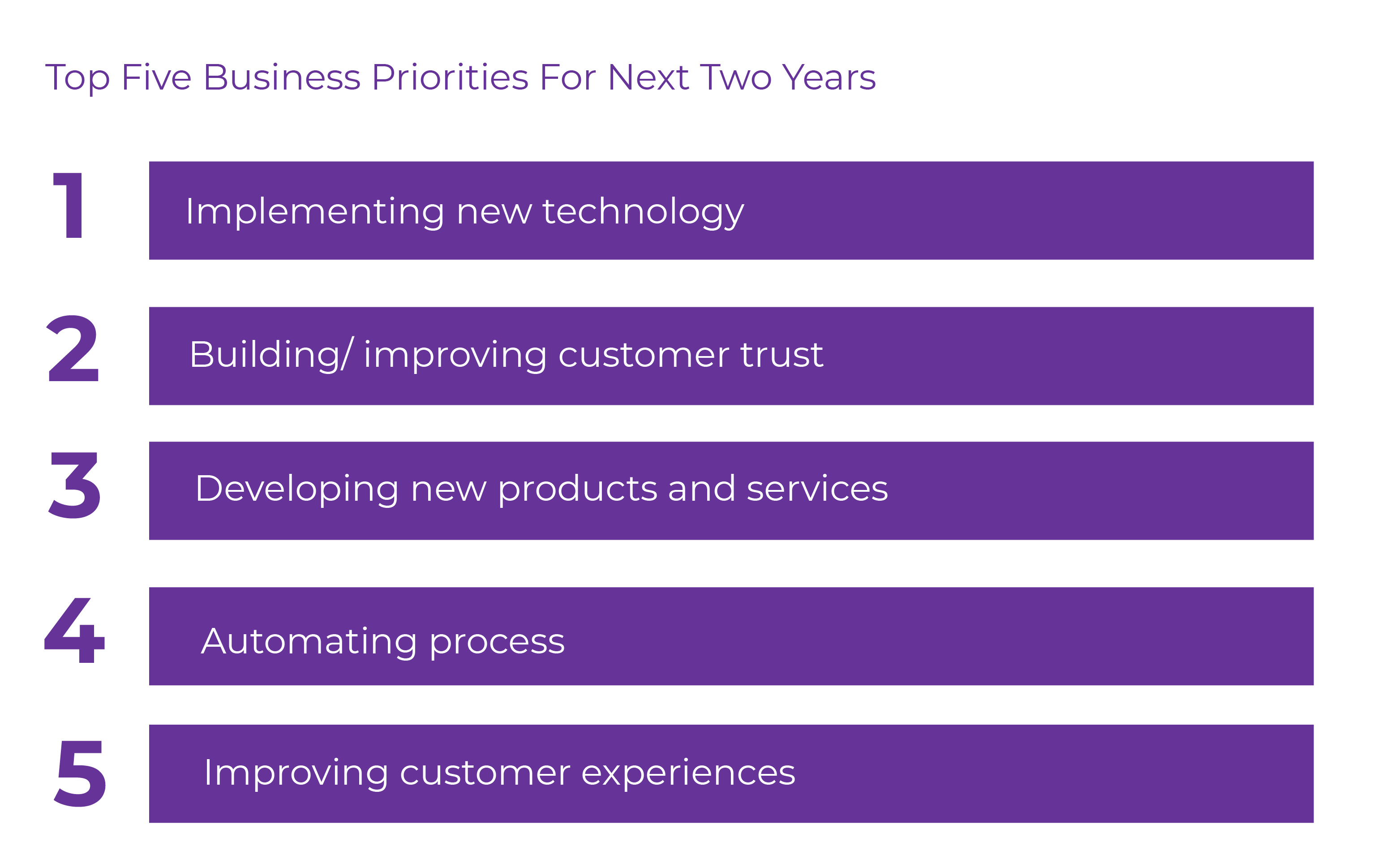

Growth-oriented FSIs have prioritised investing in personalisation, automation, virtualisation and cloud-based solutions to provide an intimate customer experience to every customer at scale.

Autonomous Finance: Lunging the CX Gap

Providing the best-personalised communication with highly customised UX for a better user experience for every customer at a scale can be challenging. Still, it’s not just a pipe dream for FSIs anymore. Even though FSIs invest heavily in the aforementioned technological capabilities, will autonomous finance be enough to bridge the CX gap created during these trying times?

Larger FSIs sit on a treasure trove of enormous amounts of valuable customer data, from buying histories to lending information to travel and medical information. Even with the newer data regulations about ownership, financial institutions are well placed to evolve into highly personalised data brokers in customers’ lives, even beyond financial services, and play a more profound role in tomorrow’s society. In this context, rebuilding trust is key to the bright future of financial services. Through autonomous finance, FSIs can learn and understand each customer’s behaviour.

Financial services should integrate more and more seamlessly with consumers’ lifestyles and devices, and organisations can use artificial intelligence to calculate personalised value analyses. The systems and technologies involved need to be highly trustworthy to succeed. The FSIs must understand that they must embrace customers’ goals more closely rather than solely focus on becoming a profit and growth powerhouse.

“Disruption will not be a one-time event, but rather a continuous pressure to innovate that will shape customer behaviours, business models, and the long-term structure of the financial services industry.”

– World Economic Forum.

Growth-oriented FSIs are inclined to leverage customer data for autonomous finance. It is powered by artificial intelligence to analyse consumer behaviour, mitigate fraud risk, and recommend relevant products and services to enhance customer experience. AI-powered bots will be available 24×7 and continuously feed on customer data to increase intelligence to deliver the right products and services to gain consumer trust. Even if scaling personalised offerings is challenging, autonomous finance can aid in bridging the gap between expectations and offerings.

“Autonomous finance is the organic convergence of all the technology innovation we’ve seen over the years, from AI to unprecedented access to data.”

– Rachid Molinary, SVP of Digital Strategy & Innovation at Banco Popular.

Customer expectations differ based on the product offerings of FSIs. Autonomous finance can use its capabilities to make automated decisions for customers.

- Retail bankers are focused on automatic account transfers. Based on customer behaviour, the AI can determine the frequency and amount of transfers subject to balance and goal-setting availability.

- Insurance leaders’ top use case is in processing claims, which can potentially reduce manual errors and resources required.

- For wealth management FSIs, autonomous finance will help foresee investment optimisation through automated savings, rebalancing portfolios, reinvesting dividends, or tax-harvesting strategies.

- SME banking can use it to automate fund allocation of a business by understanding departmental expenses, automatic timely tax payments with required paperwork submission, reinvesting profits in various avenues of growth, pre-approve and automatic business loan disbursal and multiple other functionalities.

Benefits of Autonomous Finance

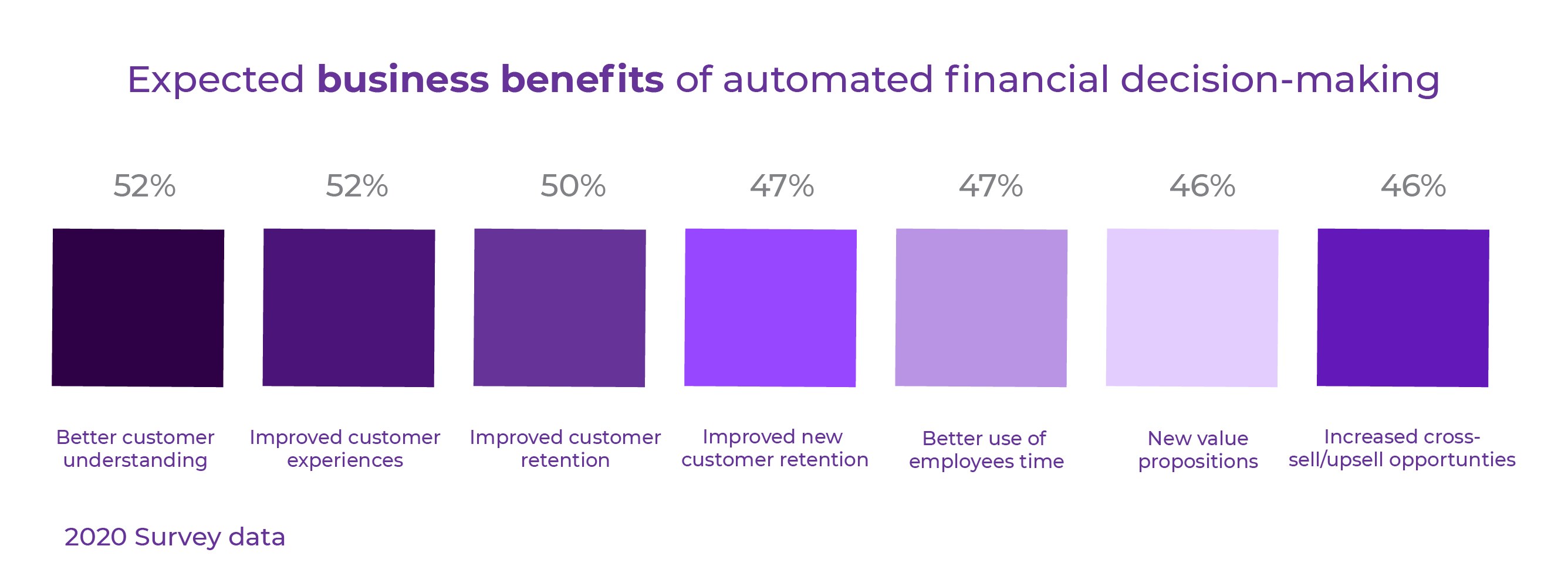

The customer benefits of autonomous finance emphasised so far is that it directly addresses the customer experience shortfalls worsened through the pandemic. Six in 10 FSIs deem better personalisation the maximum use of enforcing the new capability.

Moreover, autonomous finance strives to break down the complexity to produce better outcomes at scale. In times of economic turbulence, solutions that streamline financial decisions – like automated micro-savings tools – could be a blessing for consumers skimming through ways to increase their savings acquiescently.

The top reported business benefits also relate directly to the customer: autonomous finance’s top business benefit is associated with enhancing customer experience and providing businesses with a better insight into their consumers.

Future of Autonomous Finance

Consumers have become increasingly demanding from financial services providers, and there is a near consensus in the industry that autonomous finance will be a significant differentiator soon. According to 89% of financial services leaders, the first financial services companies to implement autonomous finance successfully will gain a substantial competitive edge.

While today’s top use cases concentrate on drastically improving process efficiencies, the next generation has the prospect of unlocking entirely new value-creation chains. Autonomous finance usage will gradually shift from operational refinements to net-new customer requisitions as the use evolves.

In the future, insurers could present new value propositions like modularising policies or creating and insuring new risk genera. For example, retail banks could instinctively pick and dispense budgets for higher education to the savings accounts of young parents. Similarly, for SME banking, banks can disburse pre-approved business loans at the time of need by understanding the business’s paying power or financial health.