Accounts Payable, traditionally, has been viewed as a cost center within an organization. There has been little interest in automating Accounts Payable (AP) management for cost-cutting in a rather paper-intensive domain.

However, AP management plays a key role in liquidity and working capital management and can be used as a tool for cost reduction through process efficiency. When managed well, accounts payable can contribute significantly to the bottom line.

This is just half the picture. Without a banking integration, AP management remains prone to inaccuracy and fraud. That’s because the ‘cost’ in cost centers ultimately gets credited via a bank account or a payments portal.

There’s little use for an AP automation solution without a good banking integration. It’s a car without wheels!

The Evolving Relationship Between Banking and Accounts Payable Management

For many startups and SMEs, accounts payable was a time-consuming process earlier, often leaving little time for other crucial tasks. As operations expanded, this issue only amplified. Finance teams were forced to do a lot of back-and-forth between multiple tools to ensure account accuracy.

When an AP automation solution gives access to banking and accounting records in a single place, the bridge in the gap saves time and effort, reduces errors, and helps build better client relationships.

Similarly, banking processes like Automatic Transfer Service ( ATS) and Real Time Gross Settlement (RTGS) have been slow to evolve. As digital payments take over, legacy payment systems and modes like cheques and RTGS are being replaced with accounts payable automation, banking integration, and instantaneous payments.

A progression can be seen in cost reduction as more electronic payments and automation are integrated into payable processing. This article digs deeper into the evolving camaraderie between Integrated banking and AP management and how it brings efficiencies to organizational processes.

The Benefits of Deep Banking Integration for Accounts Payable

Payment automation and electronic payments offer key cost-reduction opportunities compared to labor-intensive AP management.

Best-in-class companies with high Accounts Payable centralization, automation, and visibility achieved cost improvements, speed advantages, and accuracy improvements. For several reasons, CFOs are looking to migrate to a streamlined AP automation solution with integrated banking.

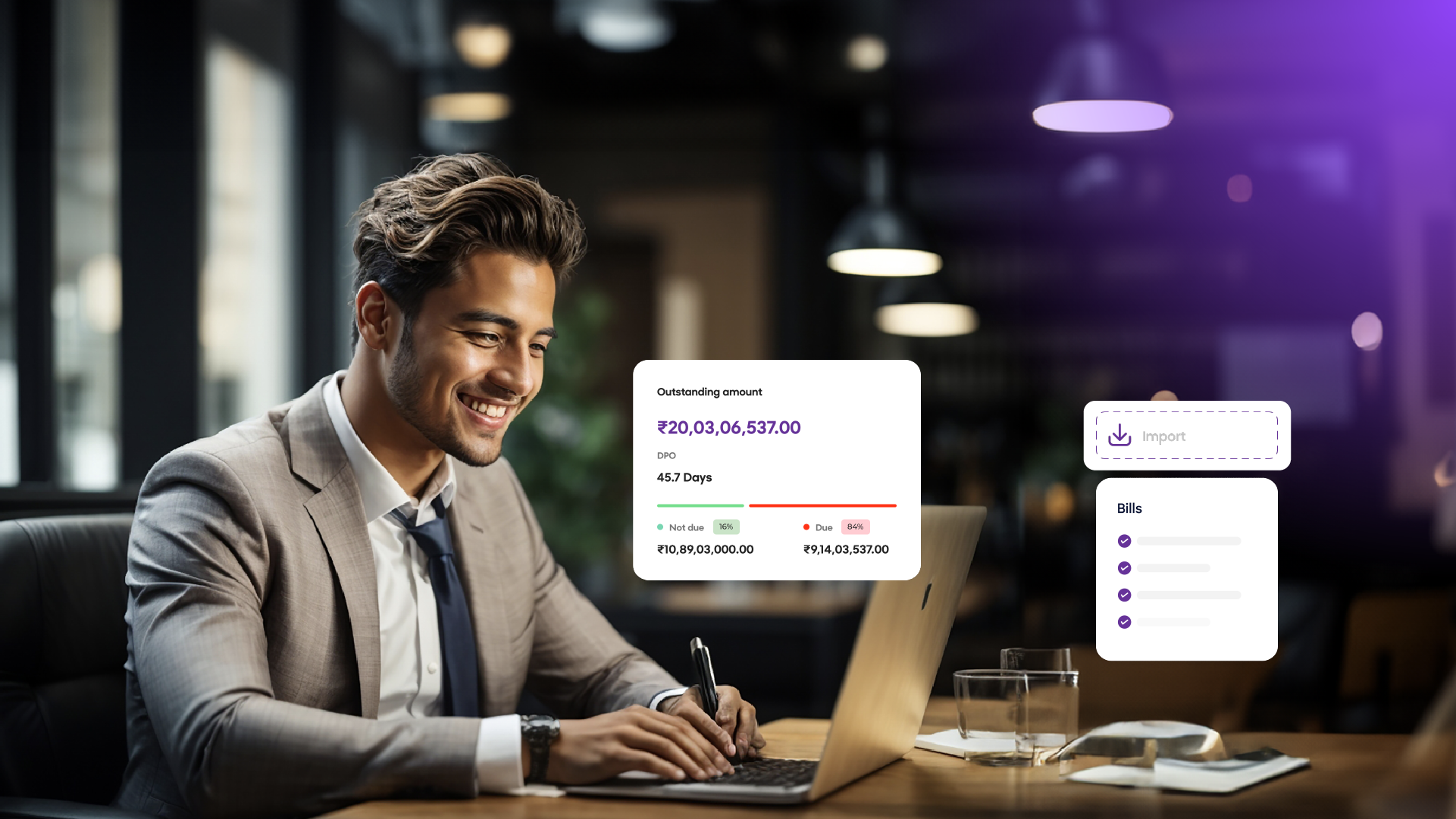

Real-time cash visibility and forecasting

Integrated banking Accounts Payable solutions allow real-time visibility of payment records and bank accounts, helping the finance team ensure enough cash in the organization at all times. With enough liquidity, payments can be smooth and timely.

Real-time visibility also ensures the:

- Elimination of duplicate invoices,

- Reduction in errors,

- Availing of rebates and discounts

- Audit trails

- Improved supplier relationships.

It provides real-time analytics that help identify trends and bottlenecks, monitor the volume of invoices and related documents, improve cash analysis and planning, and liquidity management.

Streamlined payment processing

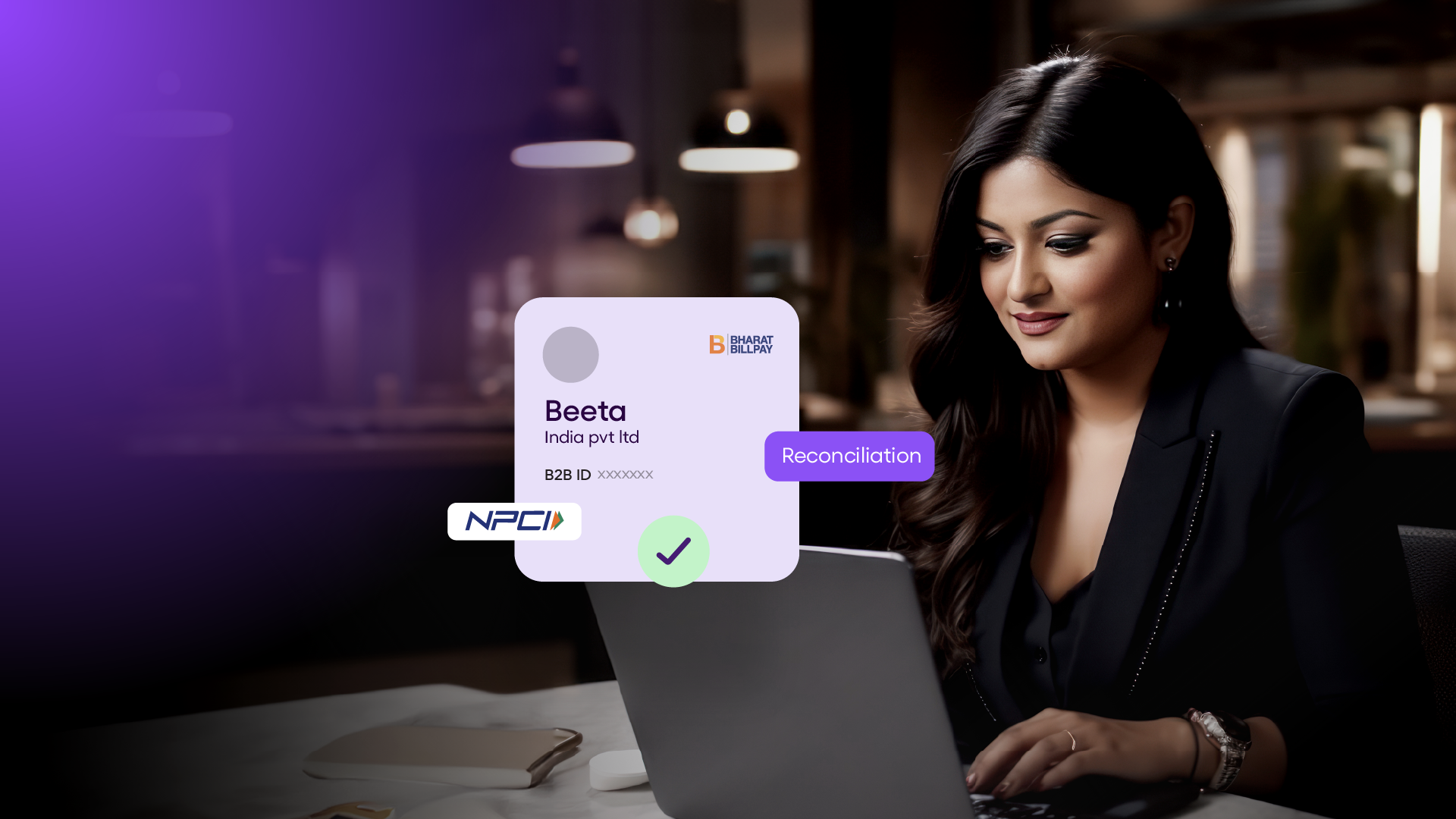

Businesses that automate enjoy additional efficiencies, such as reconciliation and analytics benefits. When payments are integrated with accounts payable management, payment reconciliation is organic.

When a transaction ID is loaded into the ERP, it flows with the payment information reporting from the previous day and can be automatically matched with the AP accounts. This can save a lot of time and manual effort.

With more time, the finance team can concentrate on more value-added activities and work towards a culture of continuous improvement.

Enhanced fraud detection and prevention

A 2020 AFP Payments Fraud and Control Survey Report reveals that 81% of companies experienced attempted or actual payment fraud attacks.

An integrated accounts payable automation system can reduce the risks of payment fraud. Most of these software require account verification and validation every time when:

- a new supplier is added

- supplier banking or personal information is updated for enhanced fraud risk mitigation.

Since the system is centralized and closed, common payment scams, such as business email compromise, can be detected and eliminated.

| Anuradha Somani, Head of Payments and Global Treasury Management at U.S. Bank, said, “Best-in-class AP automation solutions basically eliminate that risk because you’re dealing with a closed system. The data is being stored in a place where if there’s ever a request for a change to the account, it can be pre-validated before a payment goes out the door.” |

Improved supplier relationships

When suppliers get paid a little faster and also receive remittance data electronically, the need to process paper checks is eliminated. Streamlined and automated payments and prompt notification in case of delays can help strengthen buyer-supplier relationships. Both the parties in the transaction benefit from better user experience, communication, and reconciliation.

Notable AP automation providers such as OPEN Money are PCI DSS compliant to protect sensitive information within their secure systems. This prevents any data theft and helps improve the bottom line at the broader level.

Key Considerations When Integrating Banking Systems with Accounts Payable

Data security and compliance

When integrating banking with your Accounts Payable automation software, ensure that the program provides adequate data security and protects sensitive payment information. Confirm and verify where the bank stores this kind of information and confirm who is responsible for the compliance part.

The banking integration program should be in sync with the industry standards and regulations such as:

- PCI DSS (Payment Card Industry Data Security Standard)

- NACHA (National Automated Clearing House Association)

- OFAC (Office of Foreign Assets Control)

Scalability and flexibility

Before integrating any external program into the organization’s internal systems, ensure the program offers flexibility in payment methods, such as cards, ACH, digital payment, etc. Different suppliers may prefer different payment methods, so check with the bank to see if they provide their preferred or multiple methods. Also, ensure the banking integration and AP automation are well-equipped to tone up and tone down as the scale of activities fluctuates within your organization.

User experience and adoption

Check for the overall user experience and whether the finance operations are streamlined and synced with the banking integration. Finance teams can only check for accuracy and errors when real-time AP transactions are reflected in account books and bank statements.

Another consideration is the customer support and the training module, which will help employees learn and utilize the new software to their advantage.

Emerging Trends in Banking Integration for Accounts Payable

Open banking and API-driven integration

Open banking has long been a favorite of businesses and digital spaces. It refers to using APIs to share financial data and services with third parties.

This third party may be a fintech firm, automation software, or an app that provides financial services. Third parties use the shared financial data and services to provide technology, a service, or an app to the bank’s customers.

Since the shared data are the statements and transaction records belonging to the bank’s customers, this data cannot be made openly available. The data is available only at the explicit request of the customer.

Open banking provides the technological infrastructure and legal frameworks to facilitate consent-driven sharing with third parties on behalf of tier customers.

Blockchain-based payment solutions

Blockchain is a shared database that can store data immutably and transparently validate transactions via consensus. Given its encryption and decentralization, blockchain offers great security and transparency in AP processes.

Since the transactions are validated and recorded immutably on a blockchain, the scope for data tampering and fraud is reduced to a minimum. Thus, trust between suppliers and finance teams becomes automatic.

Blockchains like Ethereum deploy smart contracts that execute automatically when predefined instructions are met. Blockchain-based payment solutions are great AP management tools for streamlining payment workflows and reducing dependency on intermediaries.

Blockchain-based supply chain finance allows dynamic discounting and optimization, encouraging ecosystem collaboration.

Want to know more about AP Automation? Check out our latest e-book!

AI-powered cash flow optimization

Artificial Intelligence has emerged as the hottest tech trend since the introduction of OpenAI’s ChatGPT. However, AI isn’t a new phenomenon. Automation and AI have often been discussed when adding efficiencies to legacy processes.

Artificial Intelligence applies machine learning algorithms to data that these software solutions collect. AI-powered solutions offer advanced features such as

- Predictive analytics for cash flow management

- Supplier relationship optimization

- AI-powered chatbots for better user experience

- Provision of real-time support for queries around invoices, payments, and compliance

- Natural language processing (NLP) capabilities for seamless communication between stakeholders and the finance team

Actionable Steps for CFOs to Achieve Seamless Banking Integration in Accounts Payable

CFOs can consider putting certain steps into action for the seamless and frictionless integration of banking in Accounts Payable:

- Develop structured plans and strategies for engaging with key suppliers.

- Encourage a culture of feedback and use the feedback to improve supplier relationships .

- Invest in payment platforms and mobile solutions to ensure real-time transactions and digital footprint tracking with trusted banks offering superior payment capabilities and API integrations.

- Utilize the data collected to build real-time analytics .

- Use forecasting tools to build and improve cash flow management strategies.

- Communicate the benefits of integrating AP management software with teams and top management to ensure successful adoption.

- Keep yourself up to date on regulatory requirements and compliance.

- Establish governance frameworks to ensure the ethical and responsible use of AI, blockchain, cloud computing, and other technologies in AP operations.

- Allocate resources to upskill finance teams in operating and managing automated systems effectively.

OPEN offers AP automation with integrated banking for a superior experience. OPEN also provides access to real-time analytics and insights to simplify your finances and stay on top of cash flow. Connect bank accounts to pay vendors, receive payments, and reconcile effortlessly. It never gets easier and smoother than with OPEN.

Start your AP automation journey with OPEN today.