Every seasonal business owner knows the feeling. Peak season hits, money flows in fast, and everything seems under control. Then the slow months arrive — and suddenly, the same business that was flush with cash is scrambling to make payroll.

This isn’t a rare story; it’s the operating reality for many seasonal businesses across India, from tourism operators and wedding vendors to retail chains and agribusinesses. In fact, research widely cited across small business finance studies shows that 82% of small businesses fail because of poor cash flow management or a poor understanding of cash flow.

The root problem is often not just revenue, but visibility into it. When your cash sits across two, three, or even four bank accounts at different institutions, getting a clear picture of what’s actually available becomes difficult. Cash flow management for seasonal businesses demands more than a spreadsheet updated every few days. It requires real-time, consolidated visibility across every account — so decisions are based on facts, not assumptions.

What Is Cash Flow Management for Seasonal Businesses?

Cash flow management for seasonal businesses is the practice of planning, tracking, and controlling money movement across the full calendar year — not just during peak periods.

Unlike businesses with consistent monthly revenue, seasonal operators deal with predictable but significant swings: high inflows during a busy quarter, followed by months where fixed costs continue even as revenue slows.

What makes this different from standard cash flow management is the time compression. A seasonal business must effectively “earn and save” during a limited window, then deploy those reserves strategically across the rest of the year. This requires a structured view of cash positions across all bank accounts — not a mental tally or a bank statement reviewed after the fact.

Multi-bank visibility is a key part of this equation. Many growing seasonal businesses maintain accounts at more than one bank — for operational flexibility, vendor preferences, or access to credit. Without a consolidated view, finance teams often log into multiple portals, reconcile data manually, and make decisions based on incomplete information.

Why Seasonal Cash Planning Can Make or Break Your Business

Here’s where many finance teams go wrong: they treat the off-season as a cash conservation problem when it’s actually a planning problem. By the time cash runs short in February, the decisions that caused it were often made months earlier.

Research across small business ecosystems consistently shows that poor cash flow management — not just low revenue — is a leading contributor to business stress and failure. In India, the challenge is amplified by fragmented banking setups, where businesses operate across multiple accounts without a unified view.

The cost of poor visibility is tangible. It shows up as:

- Missed vendor payment windows that strain supplier relationships

- Over-borrowing during slow months due to unclear cash positions

- Under-investing during peak seasons out of fear of future shortfalls

- Reconciliation delays that result in decisions based on outdated data

Seasonal cash planning — done well — turns predictable revenue cycles into an advantage. You already know when money comes in. The real challenge is ensuring you can see it, move it, and plan around it effectively.

How Effective Cash Flow Management Works for Seasonal Businesses

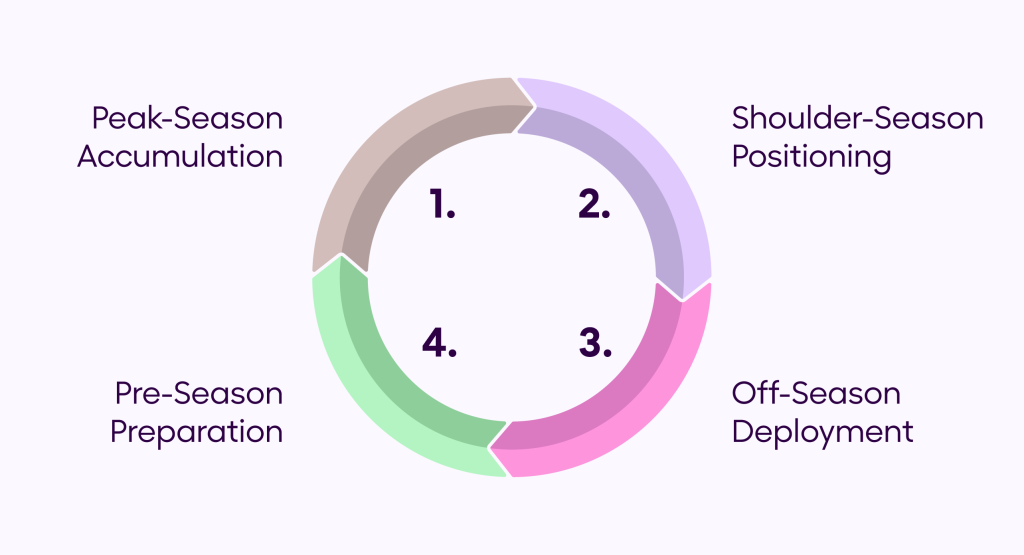

The mechanics of seasonal cash flow management break down into four phases. Most businesses focus only on the first — and get caught out by the rest.

- Phase 1: Peak-season accumulation: During high-revenue months, the goal is not just to collect payments but to direct surpluses intentionally. Finance teams should aim to build a reserve that typically covers 3–6 months of fixed costs, depending on the length and variability of their off-season, rather than simply watching the account balance rise. This requires knowing exactly how much is available across all accounts at any given moment.

- Phase 2: Shoulder-season positioning: As revenue begins to taper, expense alignment is critical. This is when businesses should be renegotiating vendor terms, staggering supplier payments, and ensuring working capital doesn’t get trapped in idle accounts at underused banks.

- Phase 3: Off-season deployment: During slow months, every outflow needs to be deliberate. Fixed costs — rent, salaries, loan repayments — should be funded from pre-set reserves. Variable spending should be reviewed weekly, not monthly. Businesses that track this at the account level catch shortfalls before they become crises.

- Phase 4: Pre-season preparation: The weeks before a peak season opens are often the most cash-intensive: inventory, marketing, staffing ramp-ups. Businesses that don’t have a clear view of what’s sitting across their accounts either underspend and miss the opportunity, or overspend and strain their off-season reserves.

What to Look for in a Cash Flow Tool for Your Seasonal Business

Not every financial tool is built for businesses whose revenue arrives in waves. Here’s what actually matters when evaluating a platform for seasonal cash flow management:

1. Multi-bank connectivity: If the platform can’t connect to all your banks in one place, it’s not solving the core problem. Look for tools that pull real-time balances and transaction data across all your current accounts — not just the primary one.

2. 12-Month cash flow forecasting: A monthly view isn’t enough. Seasonal businesses need a full-year projection, broken down by week during peak periods and by month during the off-season. Tools that integrate historical data with forward-looking inputs are far more useful than static templates.

3. Automated reconciliation: Manual reconciliation across multiple bank accounts consumes hours that seasonal finance teams don’t have — especially during peak weeks. Automated matching of inflows and outflows with accounting records reduces errors and saves time exactly when it matters most.

4. Real-time payment controls: Being able to initiate and approve payments from a single dashboard — regardless of which bank account the money sits in — gives seasonal businesses operational control they’d otherwise lack. This is especially important during high-volume peak weeks when payment volumes spike.

Here’s how the most common cash management approaches compare for seasonal businesses:

| Approach | Visibility | Manual Effort | Best For |

| Multiple bank portals | Fragmented | High | Businesses managing multiple bank logins |

| Spreadsheet tracking | Delayed | Very high | Micro and early-stage businesses |

| ERP with bank module | Partial to near real-time | Medium | Larger or process-heavy teams |

| Connected banking | Real-time, unified | Low | Seasonal & multi-bank SMBs |

How Open Enables Smarter Cash Flow Management for Seasonal Businesses

OPEN’s connected banking platform gives seasonal businesses a single dashboard to view balances, track transactions, and initiate payments across all their bank accounts — in real time. Instead of switching between multiple bank portals, finance teams get a clear, live view of their cash position whenever they need it.

With Open, teams can:

- View real-time balances across all accounts with multi-bank visibility

- Make instant payments through multiple payment methods from one unified dashboard

- Download account statements easily for faster tracking and reporting

- Automate reconciliation with accounting tools and ERPs

This eliminates manual tracking across systems and ensures decisions are based on current, accurate data — not delayed reports.

When you can see all your cash in one place, you stop reacting and start planning.

Six Practical Strategies for Seasonal Cash Flow Management

Visibility is the foundation — but it only matters if it drives action. Here are the strategies that work once you have a real-time view of your cash:

- Build a 12-month cash flow forecast early

Do this before peak season begins, using at least two years of historical data to project weekly inflows and fixed monthly costs. - Set a clear reserve target

Aim for 20–30% of peak-season revenue as a baseline to cover off-season expenses and pre-season ramp-up. - Align payables with your cash cycles

Negotiate supplier terms so larger outflows coincide with peak inflow periods. - Simplify your bank account structure

Close or consolidate underutilized accounts to reduce reconciliation effort and improve visibility. - Automate receivables follow-ups

Use reminders and payment links to keep collections on track during high-volume peak periods. - Use short-term financing strategically

It works best for pre-season investments like inventory or marketing — not for covering recurring off-season costs.

Conclusion

Cash flow management for seasonal businesses isn’t about surviving the slow season — it’s about using the peak season so effectively that the slow months become manageable by design. The businesses that get this right aren’t necessarily the ones with the highest revenue. They’re the ones that can clearly answer, at any moment, how much cash they have, where it sits, and what it needs to do next.

Multi-bank visibility makes that possible. When your cash position is consolidated and up to date, planning shifts from reactive to proactive.

Explore how real-time cash visibility can help you manage seasonal cash flow with greater clarity and control. → open.money

FAQs

1. What is the best way to manage cash flow for seasonal businesses?

The most effective approach combines a 12-month cash flow forecast, a dedicated off-season reserve built during peak months, and clear visibility across all bank accounts. Seasonal cash planning works best when you can see your full cash position in one place — not piece it together from multiple sources.

2. What is multi-bank visibility, and why does it matter for seasonal businesses?

Multi-bank visibility means viewing balances and transactions across all your bank accounts in a single dashboard. For businesses operating across multiple banks, this removes the need for manual consolidation and enables faster, more accurate financial decisions.

3. How does connected banking help with seasonal cash planning?

Connected banking platforms link bank accounts, payments, and accounting systems into one interface. This enables automated reconciliation, centralized payment control, and up-to-date cash position data, reducing manual effort and improving decision speed.

4. Can small seasonal businesses benefit from a multi-bank cash management platform?

Yes. Even with a few accounts, a consolidated view and automated workflows reduce manual effort and improve control. As the business grows, this becomes even more valuable, since complexity increases faster than revenue.