If you stroll around a market in our country, you’ll find your path flanked by myriad stores – pharmacies, eateries and tea shops, trading agencies, home appliance stores, grocery shops, travel agencies, real-estate brokers’ offices and others.

Or it could even be a more formal space, like a shopping mall peppered with boutiques, showrooms and cafes – many of these establishments are run and managed by a single person, called the sole proprietor.

Since there is only one business head in this scenario, they are usually the recipient of all profit and the bearer of all risk. Sole proprietorship business is one of the most common forms of self-employment in India.

And like most other businesses, a sole proprietorship can benefit from a business loan in various ways, like paying rent or salaries, diversifying the product line or expanding operations, purchasing equipment or machinery, running marketing campaigns, or hiring new talent.

With the help of a business loan, a sole proprietor can take advantage of opportunities that may have been previously out of reach due to a lack of funds. Perhaps more importantly, a business owner in this category can use a timely loan to cover short-term expenses such as bills and employee salaries, even when the business may not be going well due to internal or external factors. This can help ensure the survival and growth of the venture.

Here’s how a sole proprietorship business can thrive with a business loan:

Emergency fund and safety net for unforeseen circumstances

If you’re a business owner, chances are you know how precarious it is to run a business. From rainy days to unforeseen economic circumstances, a sudden spike at peak season to personal emergencies, there are many factors which can drain resources, leaving your company vulnerable. A business loan in this context can be a useful safety net and soften the impact of such an event.

Retain full ownership of your business

Sole proprietors can access loans from various sources like investor funding, friends or family and banks. While the latter two might involve an interest to be paid, bringing in an investor can mean diluting your ownership of the business or reducing your decision-making power. This may not be ideal, since you may struggle to steer your business in the direction you want or influence outcomes.

Cover your operational costs easily

As in any other venture, a sole proprietorship business has several operations which incur expenses on a day-to-day, weekly or monthly basis like vendor transactions, infrastructural costs or employee salaries and bonuses. A business loan can help ensure that your short-term operational costs are covered while you focus on growing your revenue.

Diversify and expand

Any business-owner would aspire to grow and expand their business in a sustainable way. With a timely business loan, you can purchase equipment and machinery or invest in marketing and publicity campaigns to boost your venture’s growth.

Now that we’ve enumerated the many ways in which a business loan can aid a sole proprietorship business, let’s look at the hurdles some of them face in accessing funds.

Obstacles and Risks

High interest rates: Traditional lenders are known to disburse loans at high interest rates, often regardless of the health of your business. Whatever may be the financial behaviour, credit score, the turnover or the nature of the company, high interest rates can invariably restrict a sole proprietorship business.

Hefty pre-closure charges: As a sole proprietor, you may dislike the burden of a loan. Perhaps your business is going well and you want to pay it back far before the term ends to become debt-free. However, many lenders impose foreclosure charges on single complete loan repayment, somewhere between 2-5% of the loan amount.

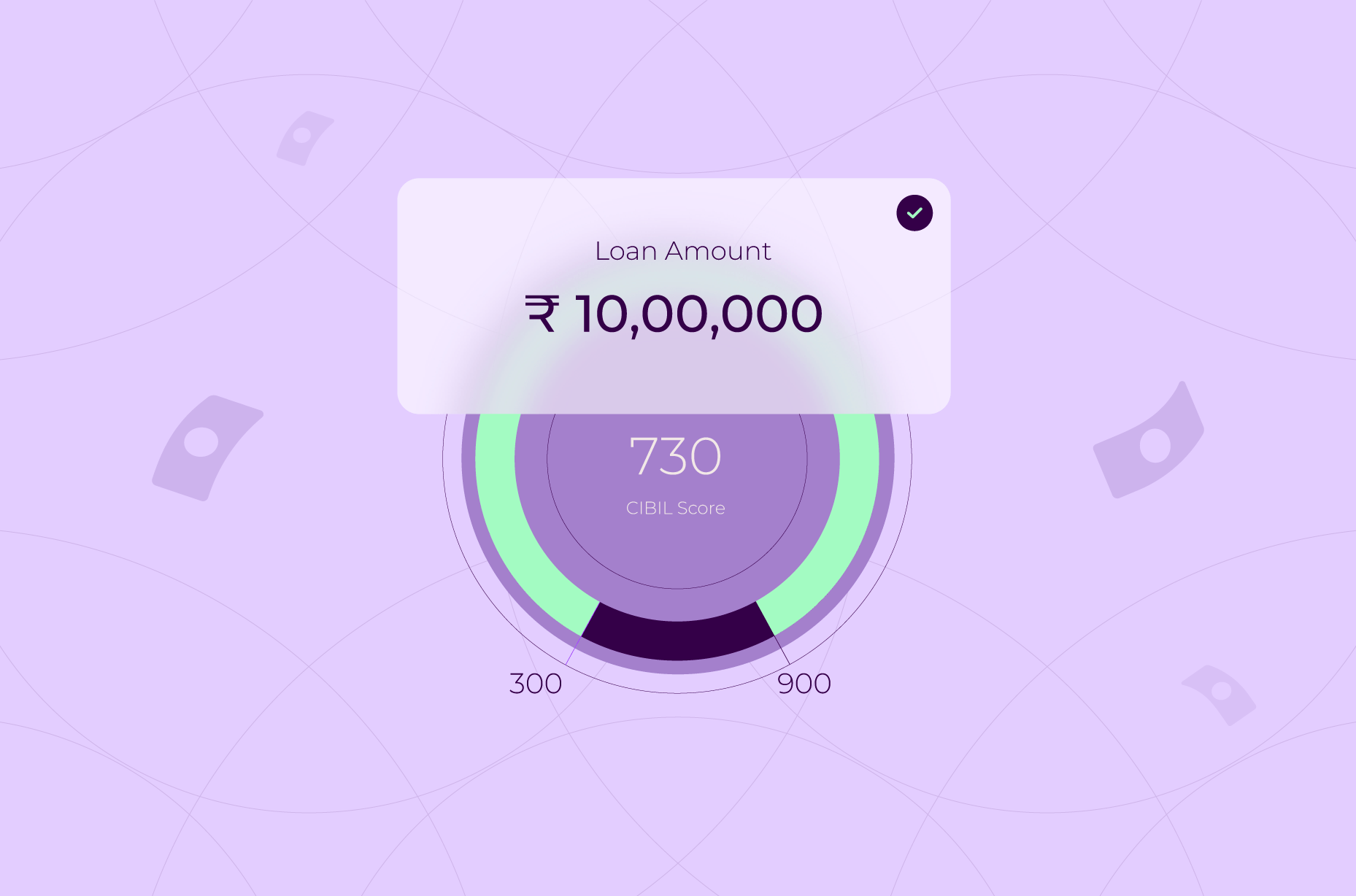

Inability to meet the lender’s acceptance criteria: It can be stressful for sole proprietors to produce collateral or strong credit histories if they are new in the market or lack financial data. Having to convince branch managers, filling out paperwork, long turnaround time for disbursement, and complicated application processes – all these can create hurdles for your business.

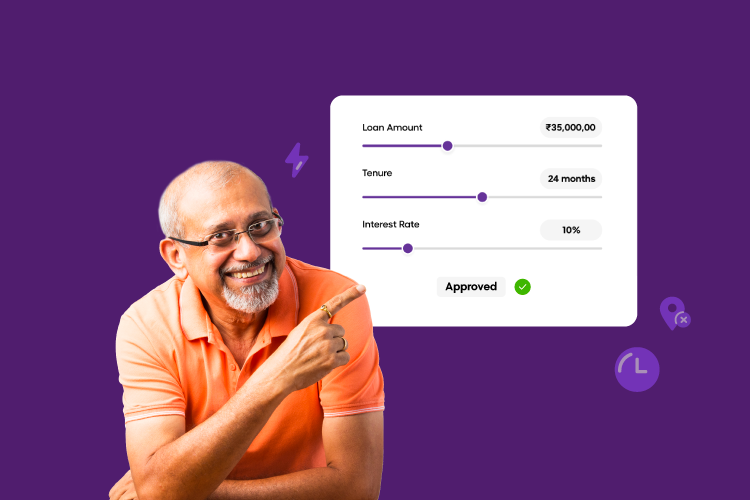

As one of India’s foremost business banking partners, OPEN powers over 3 million businesses. We understand how critical it is for growing businesses to access loans, and so we offer a holistic solution for easy loan application for sole-proprietorship businesses such as yours, covered in 3 simple steps.

OPEN Capital loans are collateral-free and come at low interest rates (as low as 1% per month) and no pre-closure charges.