AI is reshaping how businesses access credit. But AI credit decisioning is only as reliable as the data on which it is built. For Indian SMBs and fintech platforms, this means one thing: without clean and unified banking data, even the most advanced AI models will struggle to deliver consistently accurate, fair, and scalable lending decisions.

This shift is already visible across the industry. Research shows that many machine learning adopters in India are able to expand credit access to underserved segments while also improving profitability through better risk prediction and reduced bad debt. However, these outcomes are not driven by algorithms alone—they depend heavily on the availability of clean, complete, and well-structured financial data.

In India’s fragmented financial ecosystem, where businesses operate across multiple bank accounts, payment gateways, and accounting systems, financial data often exists in silos. This fragmentation makes it difficult to construct a complete and reliable picture of a business’s financial health.

Before AI can effectively automate underwriting or risk assessment, it requires a structured, standardized, and trustworthy view of financial activity, increasingly enabled by API-driven integrations and frameworks such as the Account Aggregator system.

This blog explores why connected banking data and strong data quality in banking form the foundation of effective credit underwriting automation, and how Indian businesses can build for it.

TL;DR

- AI credit decisioning depends on high-quality data, not just advanced algorithms

- Fragmented financial data leads to inaccurate risk assessment and missed credit opportunities

- Unified, real-time banking data enables faster and more reliable underwriting

- The Account Aggregator framework enables secure, consent-based financial data sharing in India

- Clean data is essential, but model governance and transparency remain equally important

What is AI Credit Decisioning?

AI credit decisioning refers to the use of machine learning models to evaluate a borrower’s creditworthiness using real-time and historical financial and behavioral data.

In practice, this shifts lending from document-based underwriting to continuous, data-driven decisioning.

Unlike traditional underwriting—which relies heavily on credit scores and static financial statements—AI models analyze:

- Transaction-level banking data

- Cash flow patterns

- GST filings

- Invoice cycles and receivables

- Customer and vendor payment behavior

This enables:

- Faster loan approvals

- More dynamic and responsive credit limits

- More inclusive access to credit for SMBs

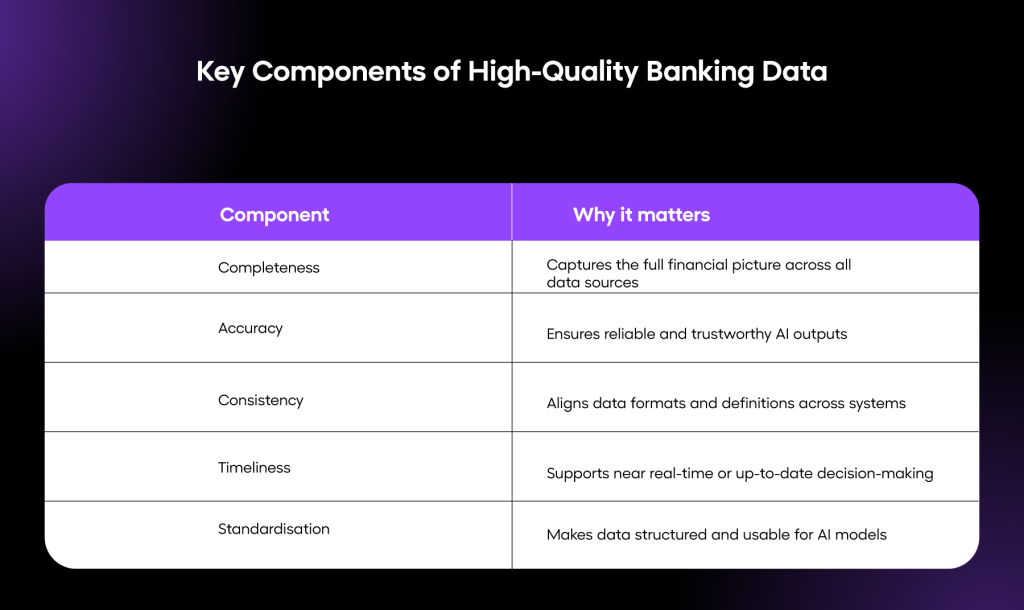

The Missing Link: Why Data Quality Matters More Than AI

AI is often positioned as the intelligence layer in lending. In reality, data quality is the foundation that determines how effectively AI systems perform.

1. Garbage in, garbage out

AI models are only as reliable as their inputs.

If your data is:

- Incomplete

- Duplicated

- Delayed

- Inconsistent across systems

Then outputs—such as credit scores, risk signals, and approvals—are likely to be unreliable or misleading.

Example:

An SMB using multiple bank accounts for collections and payouts may appear to have lower revenue if those data streams are not unified, leading to incorrect risk assessment.

2. Fragmented data breaks context

AI does not just analyze transactions; it interprets patterns over time.

Disconnected datasets fail to capture:

- True cash flow cycles

- Seasonal revenue fluctuations

- Payment recovery behavior

This can result in:

- Mispriced credit

- Lower approval rates

- Incorrect borrower categorization

3. Regulatory and compliance risks

In India, digital lending is governed by evolving frameworks from the Reserve Bank of India (RBI), with strong emphasis on:

- Borrower consent

- Data transparency

- Auditability of decisions

Poor data quality can lead to:

- Incomplete audit trails

- Limited explainability in AI-driven decisions

- Increased regulatory scrutiny

Regulators globally, including the RBI, have also highlighted the importance of transparency and accountability in automated decision-making, making clean and traceable data even more critical.

What is Connected Banking Data?

Connected banking data is an industry concept that refers to the aggregation and standardization of financial data across multiple sources into a unified and increasingly real-time view of financial activity.

This includes:

- Bank accounts

- Payment gateways

- UPI collections

- Card transactions

- Accounting and ERP systems

In India, this is enabled through a combination of regulatory frameworks and technology infrastructure:

1. Account aggregator (AA) framework

A consent-driven data-sharing system that allows businesses to securely share financial information with lenders and financial institutions.

- Financial Information Providers (FIPs): Banks, NBFCs

- Financial Information Users (FIUs): Lenders, fintech platforms

- Fully regulated by the Reserve Bank of India (RBI)

2. API-based banking infrastructure

APIs enable:

- Near real-time data access

- Seamless integrations across systems

- Continuous synchronization of financial data

3. Digital payment rails

Systems such as UPI generate rich transaction-level data that contributes to a more complete financial picture, even though they do not aggregate data by themselves.

Why Unified Banking Data is Critical for AI Credit Decisioning

1. Accurate cash flow analysis

Unified data provides a more complete view of a business’s financial activity, including:

- Visibility into inflows and outflows

- Reduced risk of revenue underestimation

- Clearer understanding of expense patterns

This supports:

- More accurate credit assessment

- Better-aligned loan limits

- Improved risk evaluation

2. Near real-time decisioning

Traditional underwriting is often slow because it depends on static documents.

With connected data:

- Transactions are continuously updated

- AI models can assess risk more dynamically

- Loan decisions can be significantly faster in well-integrated systems

Industry studies show that AI-led underwriting improves decision speed and operational efficiency, especially in high-volume lending environments.

3. Better risk segmentation

Clean, structured data allows AI systems to:

- Identify high-quality borrowers

- Segment businesses based on financial behavior

- Detect early warning signals

For example, a business with volatile revenue but strong recovery cycles may still be creditworthy—something AI can identify more effectively with high-quality, time-series data.

4. Reduced manual intervention

Without unified data:

- Teams manually reconcile financial records

- Errors are more likely

- Decision timelines increase

With integrated systems:

- Data flows directly into underwriting engines

- AI models operate on structured inputs

- Human effort shifts toward exception handling and oversight

How OPEN Money Enables Better AI Credit Decisioning

As discussed, effective AI credit decisioning depends on clean, connected, and continuously updated financial data. In practice, decisioning systems often fall short not because of weak models, but because the underlying data is fragmented, inconsistent, or difficult to trust.

OPEN Money is designed to solve this at the source.

By bringing together financial data into a single, connected system, OPEN helps transform scattered banking activity into a more structured and reliable data layer—one that underwriting and decisioning systems can effectively use.

With OPEN, businesses can:

- Access a unified view of balances across connected bank accounts

- Retrieve statements and transaction data from a single interface

- Track platform-initiated payouts with complete context

- Maintain validated beneficiary records through IFSC-based verification

- Organize and reconcile financial data more consistently across systems

This isn’t just about visibility. It’s about creating a consistent data foundation that supports better underwriting, faster decisions, and more scalable lending operations.

Build your data layer first. Then let AI do its job.

Important: Clean Data is Necessary, Not Sufficient

While clean and connected data is critical, it is not the only requirement for effective AI credit decisioning.

The reliability of AI-driven lending also depends on how models are designed, governed, and monitored over time.

Lenders must ensure:

- Model transparency and explainability

- Bias detection and mitigation

- Continuous model monitoring and performance tracking

Together, these factors ensure that AI systems remain accurate, fair, and reliable as they scale across different borrower segments and use cases.

How to Build a Strong Data Foundation for AI Credit Decisioning

How to Build a Strong Data Foundation for AI Credit

Aggregate all financial data

Use APIs and frameworks like the Account Aggregator system to consolidate data across bank accounts, payment systems, and accounting platforms.

Clean and standardize data

Remove duplicate entries, standardize formats, and categorize transactions consistently.

Enable near real-time data flow

Shift from static uploads to API-based data syncing and continuously updated data pipelines.

Structure data for AI use

Transform raw data into structured formats like cash flow summaries, risk indicators, and behavioural insights.

Integrate with AI models

Feed structured data into underwriting systems, monitor model performance, and refine based on outcomes.

Step 1: Aggregate all financial data

Use APIs and frameworks such as the Account Aggregator system to aggregate and consolidate data across:

- Bank accounts

- Payment systems

- Accounting platforms

Step 2: Clean and standardize data

- Remove duplicate entries

- Standardize data formats

- Categorize transactions consistently

Step 3: Enable near real-time data flow

Shift from static uploads to:

- API-based data syncing

- Continuous or frequently updated data pipelines

Step 4: Structure data for AI use

Transform raw data into structured formats such as:

- Cash flow summaries

- Risk indicators

- Behavioural insights

Step 5: Integrate with AI models

- Feed structured data into underwriting systems

- Continuously refine models based on outcomes

- Monitor model performance and validate outputs

Building a unified and reliable data foundation can be complex without the right infrastructure. Platforms like OPEN Money help businesses streamline financial data, improve visibility, and simplify integrations across banking and payments.

Common Mistakes to Avoid

- Treating bank statements as sufficient data

Relying only on static statements ignores real-time transaction flows and the broader financial context. - Ignoring missing or inconsistent data

Gaps or inconsistencies in data can lead to inaccurate risk assessment and unreliable AI outputs. - Using outdated financial information

Decisions based on stale data may not reflect current business performance or cash flow realities. - Overinvesting in AI models without fixing data pipelines

Advanced models cannot compensate for poor data quality or a fragmented data infrastructure.

Use Cases of AI Credit Decisioning in India

AI credit decisioning is increasingly being applied across lending use cases in India, where real-time financial data can replace static, document-heavy underwriting. By analyzing cash flow patterns, transaction behavior, and business activity, AI enables faster and more context-aware credit decisions.

1. MSME working capital loans

For working capital lending, AI models assess transaction-level banking data to understand actual cash flow patterns rather than relying only on financial statements. This helps capture revenue volatility, seasonality, and recovery cycles—leading to faster approvals and credit limits that are better aligned with real business performance.

2. Embedded finance

In embedded finance, credit is offered directly within platforms such as marketplaces, B2B networks, or SaaS tools. AI evaluates user activity—such as sales volume, order frequency, and payment behavior—to enable near-instant, contextual credit decisions without requiring a separate loan application.

3. Invoice financing

AI improves invoice financing by analyzing receivables quality, including payment cycles, buyer reliability, and invoice aging trends. This allows lenders to move beyond invoice value alone and make more accurate risk assessments, resulting in faster and more reliable access to funds.

4. Revenue-based financing

Revenue-based financing uses AI to continuously track revenue streams and cash flow trends. This enables flexible repayment structures where repayments adjust to actual business performance, making it particularly useful for digital-first and seasonal businesses.

Across these use cases, one thing remains consistent: the effectiveness of AI credit decisioning depends on access to clean, connected, and high-quality financial data.

Pro Tips for Indian SMBs and Developers

- Consolidate financial operations where possible

Reducing the number of disconnected systems helps create a more unified and reliable financial data layer. - Maintain clean and consistent records

Standardized and accurate data improves the quality of AI-driven insights and credit assessments. - Use platforms with strong API integrations

API-first systems enable seamless data flow across banking, payments, and accounting tools. - Regularly reconcile transactions

Frequent reconciliation helps identify discrepancies early and ensures data accuracy over time. - Adopt tools that support real-time financial visibility

Access to up-to-date financial data allows for faster, more informed decision-making.

Final Thoughts

AI is reshaping how credit is assessed and delivered, but its effectiveness ultimately depends on the quality of the data it operates on. For Indian SMBs and fintech platforms, adopting AI credit decisioning is only part of the equation—building a clean, connected, and well-structured financial data foundation is what enables these systems to deliver accurate, fair, and scalable outcomes.

As lending continues to shift toward real-time, data-driven models, businesses that invest in unified banking data and strong data practices will be better positioned to improve credit access, enhance risk assessment, and scale efficiently. The takeaway is simple: before optimizing AI models, optimize your data layer.

FAQs: AI Credit Decisioning and Banking Data

1. What is AI credit decisioning?

AI credit decisioning uses machine learning to assess borrower risk using real-time and historical financial data, reducing reliance on manual underwriting processes.

2. Why is banking data quality important?

High-quality data supports accurate risk assessment, faster approvals, and helps reduce the likelihood of incorrect lending decisions.

3. What is the Account Aggregator framework?

It is an RBI-regulated system that enables secure, consent-based financial data sharing between financial institutions.

4. Can AI replace traditional credit scoring?

AI can enhance or, in some cases, replace traditional models, but it still depends heavily on data quality, model design, and governance.

5. How does connected banking data help SMBs?

It provides a more complete view of financial activity, improving access to credit and enabling more appropriate loan assessments.