Most business owners walk into a bank conversation hoping for the best. They ask for a better interest rate, a higher credit limit, or lower transaction charges — and then wait to see what the bank offers back.

In India, MSMEs contribute nearly 30% to the country’s GDP — yet their financial data often sits across disconnected systems, limiting real-time visibility into cash flow.

The businesses that consistently get better terms from their banks don’t just ask differently. They prepare differently. Specifically, they know their exact cash position across every account before they pick up the phone. Real-time balance visibility isn’t just an operational convenience — it’s the foundation of a serious bank negotiation strategy.

What Is a Bank Negotiation Strategy?

A bank negotiation strategy is a deliberate, data-backed approach to securing favorable terms from your banking partners — whether that’s lower fees, better credit rates, extended overdraft limits, or improved loan covenants.

It’s distinct from simply “asking your bank for a better deal.” A strategy involves knowing what you bring to the table: your average balances, your transaction volumes, your repayment history, and the total value of your relationship across all accounts and products.

Most finance teams think of bank negotiations as something that happens once a year, usually when a loan comes up for renewal. But the businesses that get the most out of their banking relationships treat it as an ongoing process — one that’s constantly informed by live financial data. The negotiation doesn’t start in the meeting room. It starts the moment you get full visibility into your own numbers.

Why Fragmented Account Views Weaken Your Position

Here’s a situation that plays out more often than finance teams would like to admit: a business has accounts across three banks — one for operations, one for payroll, and one for collections from a specific client segment. Each bank sees only a slice of the business. The operations bank assumes the company barely maintains its minimum balance. Meanwhile, ₹40 lakhs is sitting idle in the collections account at another institution.

When that business tries to negotiate a working capital limit with the operations bank, it’s negotiating blind. The bank sees a thin account. The business doesn’t have the numbers to prove otherwise.

This isn’t hypothetical — it reflects how banking relationships often play out when financial data is spread across multiple accounts and systems.

The problem compounds quickly. Without a consolidated view, you can’t accurately calculate your aggregate float, you can’t present your full transactional value, and you can’t make a credible case for better terms. Your negotiating position is only as strong as the data you can put on the table.

How Real-Time Balance Visibility Works as Treasury Leverage

Real-time balance visibility means knowing — at any given moment — exactly how much cash you hold across every account, in every bank, in one place. No logging into separate portals. No waiting for end-of-day statements. No mental arithmetic across spreadsheets.

The practical impact on negotiations is direct. When all data is centralized, conversations with banks become more productive. Instead of calling a bank representative to ask “What is my balance?” or “Did a wire clear?”, you already know the answer. This frees up time to discuss more important topics, such as increasing credit lines, optimizing interest rates, or exploring new investment opportunities.

More importantly, a company can generate reports showing transaction volumes by bank, average collected balances, and fee analysis — allowing it to ask the bank specific questions: “We are moving ₹X annually through your institution. What additional value can you provide?” This shifts the power dynamic slightly. The company is no longer just a client; it’s a strategic partner that understands its own value to the bank.

That shift — from passive account holder to informed strategic partner — is where treasury leverage actually comes from.

How to Use Multi-Account Visibility in Bank Negotiations

The mechanics are straightforward once you have the data. Here’s how to turn real-time balance visibility into actual negotiating power:

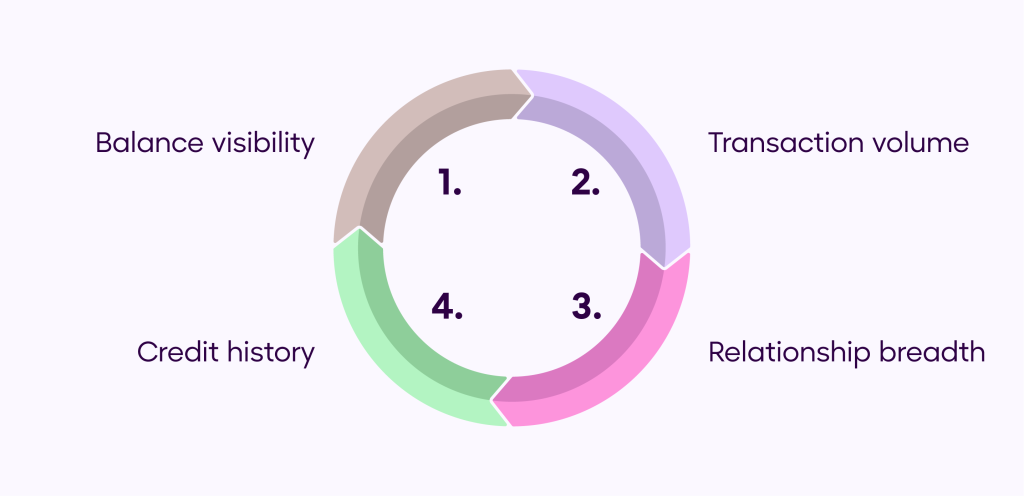

1. Calculate your total relationship value: Add up average monthly balances across all accounts at a given bank. This number is often higher than what the bank’s relationship manager sees on their screen. Present it explicitly. Banks price risk and offer concessions based on perceived relationship depth — if yours looks thin because it’s spread across multiple products without aggregation, you’re leaving leverage on the table.

2. Show transaction volume, not just balance: High-frequency businesses — those processing hundreds of transactions a day — have real value to banks beyond just their float. Transaction volume drives fee income and strengthens the overall banking relationship. Businesses using treasury systems spend far less time on reconciliation and reporting than those relying on spreadsheets. Coming to a negotiation with clean, structured transaction data signals that you’re a high-volume, low-friction client, making it easier for banks to justify better pricing, stronger service levels, and improved credit terms.

3. Time your negotiation to your strongest cash position: If you know your cash peaks mid-month after customer collections, that’s when you should present your balance data. Timing matters — stronger balances and healthier liquidity create a better negotiating position. Real-time visibility helps you plan these conversations intentionally, so you’re negotiating from strength, not necessity.

4. Use multi-bank data to introduce competition: Banks are more likely to negotiate when they know they have competition for your business. When you can show that another banking partner is handling a significant portion of your float or transactions, you create urgency without being aggressive about it.

5. Come prepared with fee benchmarks: Most businesses have no idea what they’re actually paying in bank charges until they look at three months of statements side by side. Real-time tools that consolidate fee data make it easier to identify where costs are adding up and approach the conversation with clarity on what needs to be revisited.

What to Look for in a Multi-Account Visibility Tool

Not all account aggregation tools are built the same. If you’re evaluating options to build your bank negotiation strategy on real data, here’s a comparison of what matters:

The key feature to prioritize is not just visibility, but actionable reporting — the ability to export data in formats that make sense in a banking conversation.

How Open Enables Smarter Bank Negotiation Strategy

Open’s connected banking platform gives you a unified view of your balances and transactions across linked accounts — so you always know where your money is and how it’s moving.

Instead of switching between multiple bank portals, finance teams can access consolidated account data in one place, track balances across banks, and review transaction activity by account or banking partner. This makes it easier to understand your overall relationship value and spot where funds or fees are concentrated.

With clearer visibility, bank conversations become more grounded in actual data — not assumptions.

Banking Relationship Management: What Most Businesses Get Wrong

The biggest mistake SMEs make in banking relationship management isn’t negotiating too hard — it’s not managing the relationship at all until something goes wrong.

Banks continuously assess their clients based on account behavior and transaction patterns. Clients who frequently overdraft, miss reconciliations, or show inconsistent cash flows are often seen as higher risk — even if the underlying business is stable.

On the other hand, businesses that maintain better visibility and control over their cash flows tend to have more predictable account behavior, which can support stronger banking relationships over time.

Proactive relationship management means showing up with data before problems arise. It means reviewing your banking costs annually, understanding what each bank relationship actually costs you, and knowing which partners deserve more of your business — and which ones don’t.

Good banking relationship management also means having a BATNA — a best alternative to a negotiated agreement. If you know another bank could offer you better terms, you’re no longer dependent on a single institution. That independence changes the dynamic of the conversation.

Conclusion

A bank negotiation strategy isn’t about being confrontational — it’s about being prepared. And preparation starts with having a clear understanding of what you bring as a client.

Real-time balance visibility across all your accounts turns scattered financial data into a more complete view of your relationship value. It gives you the clarity to ask specific questions, make informed requests, and evaluate whether the terms actually work for you.

The businesses that build stronger banking relationships don’t just bank harder — they bank smarter. They understand their float, transaction volumes, fee spend, and overall relationship value before any conversation begins.

Frequently Asked Questions

1. What is a bank negotiation strategy for small businesses?

A bank negotiation strategy is a structured approach to securing better terms from your bank — whether that’s lower fees, higher credit limits, or improved loan conditions. For small businesses, it starts with understanding your total relationship value: how much you hold on average, how many transactions you process, and what fees you’re currently paying. Going into any bank conversation with this data puts you in a much stronger position than simply making a verbal request.

2. How does seeing all my bank accounts in one place help with bank negotiations?

When your balances are fragmented across multiple portals, you only ever see part of your financial picture — and so does your bank. Consolidating all accounts into a single real-time view lets you calculate your actual relationship value, track transaction volumes by bank, and identify where fees are adding up. This data becomes your negotiating currency.

3. What is treasury leverage, and how do businesses use it?

Treasury leverage refers to the financial and informational advantage a business gains by having clear visibility into its cash position. When a business knows how much liquidity it holds, where it’s deployed, and what it costs to maintain, it can use that information to negotiate more favorable terms with banking partners — or credibly introduce competition from other lenders.

4. How often should a business renegotiate with its bank?

Most businesses only renegotiate when a loan comes up for renewal, but that’s a missed opportunity. A better practice is to review your banking costs and credit terms at least annually. If your business has grown significantly in transaction volume or average balance since your last review, that’s a strong case for initiating a conversation outside the standard renewal cycle.

5. Can a fintech platform really help with banking relationship management?

Yes, but not by replacing your bank. Platforms that consolidate financial data across multiple accounts give your finance team the clarity needed to have more informed conversations with bank partners. The goal isn’t to automate the relationship; it’s to ensure you’re never walking into a negotiation without the numbers you need.