Managing finances across multiple bank portals is a daily reality for many Indian businesses. What seems like a routine task — logging into different bank accounts, downloading statements, and checking balances — often comes with hidden operational overhead in the form of time spent, fragmented data, and delayed visibility.

As businesses grow, their banking setup becomes more complex. Collections, vendor payouts, payment gateway settlements, lending relationships, and compliance requirements often lead to multiple accounts across banks and platforms. While this structure supports operational needs, managing these accounts across disconnected systems adds layers of complexity that can slow down workflows and reduce overall efficiency.

This blog explores the real cost of these fragmented workflows — and how businesses can move toward more efficient, scalable financial operations.

TL;DR: The Real Impact of Multiple Bank Portals

- Managing multiple bank portals creates fragmented financial workflows

- Lack of centralized bank account visibility slows decision-making

- Manual treasury operations increase reconciliation effort and error risk

- Finance teams spend valuable time on low-value, repetitive tasks

- Connected banking enables more efficient, scalable financial operations

What Are Multiple Bank Portals?

In practice, managing multiple bank portals means finance teams operate across separate systems — logging into different bank interfaces, payment gateway dashboards, and financial platforms to access and manage financial data.

Typical scenario:

- One bank account used for collections

- Another account for vendor payouts

- A payment gateway holding settlement balances

- Loan or credit accounts with NBFCs or lenders

Each of these systems operates independently, requiring:

- Separate logins and access credentials

- Different data formats and reporting structures

- Manual consolidation of financial information across platforms

Why Indian Businesses Operate Across Multiple Bank Accounts

Using multiple bank accounts is often a practical necessity for growing businesses, driven by operational, integration, and compliance requirements.

Common reasons include:

- Diversifying banking relationships to reduce dependency on a single institution

- Managing different payment flows, such as collections and vendor payouts

- Integrating with multiple payment gateways and financial platforms

- Meeting compliance requirements, including the use of escrow or nodal accounts

For example, the Reserve Bank of India requires structured fund flows for certain entities, such as payment aggregators. This often involves designated accounts, such as nodal or escrow accounts, to manage settlements in a controlled and compliant manner.

While this structure supports regulatory compliance and operational flexibility, it also introduces additional complexity in day-to-day financial management.

The Hidden Costs of Logging Into Multiple Bank Portals

1. Time loss that adds up quickly

Accessing financial data across multiple systems is rarely instantaneous.

Finance teams often spend time:

- Logging into different portals

- Downloading statements

- Verifying balances across accounts

Individually, these tasks seem minor. But over time, they can add up to dozens of hours each month, especially for businesses managing high transaction volumes.

2. Fragmented bank account visibility

Without a unified view, even basic financial questions become difficult to answer:

- What is the total cash position today?

- Which accounts have available balances?

- Are upcoming payouts fully funded?

This lack of bank account visibility can lead to:

- Idle funds sitting unused in certain accounts

- Overdrafts or shortfalls in others

- Inefficient allocation of working capital

3. Manual treasury operations increase complexity

When treasury workflows rely on spreadsheets and manual processes:

- Data must be copied across systems

- Transactions are matched manually

- Reports are created from fragmented inputs

This introduces challenges such as:

- Delayed reconciliation

- Data inconsistencies

- Increased risk of human error

Manual reconciliation is time-consuming and prone to errors—especially at scale. As transaction volumes increase, matching entries across systems and identifying discrepancies requires significant manual effort, slowing down workflows and increasing the risk of inconsistencies.

4. Slower financial decision-making

Timely decisions depend on timely data.

When financial information is spread across multiple bank portals:

- Teams must consolidate data before analysis

- Reporting cycles become slower

- Real-time cash flow visibility is limited

This can result in:

- Delayed vendor payments

- Inefficient cash flow planning

- Reduced agility in responding to business needs

5. Reduced finance team productivity

Highly skilled finance teams often spend a disproportionate amount of time on operational tasks such as:

- Logging into banking portals

- Downloading and organizing data

- Updating spreadsheets

This reduces the time available for:

- Financial planning and analysis

- Cash flow optimization

- Strategic decision-making

Improving finance team productivity requires minimizing dependency on manual, repetitive workflows.

6. Increased compliance and audit effort

Fragmented financial data makes compliance more demanding:

- Audit trails are spread across multiple systems

- Supporting documents take longer to compile

- Reconciliation gaps can delay reporting

For Indian businesses managing GST, TDS, and other regulatory requirements, this adds avoidable operational overhead and increases audit complexity.

Managing multiple bank portals shouldn’t take up your team’s time.

OPEN’s Connected Banking helps you unify accounts, automate workflows, and improve financial visibility—all in one place.

Book a quick demo.

Manual vs Efficient Treasury Management

As businesses scale, treasury operations often evolve from manual, fragmented processes to more centralized and automated systems.

| Aspect | Manual Treasury | Efficient Treasury |

|---|---|---|

| Access | Multiple bank portals | Single unified dashboard |

| Data handling | Manual downloads | Automated syncing |

| Reconciliation | Manual matching | Automated process |

| Visibility | Fragmented, delayed | Real-time, consolidated |

| Decision-making | Slower, report-dependent | Faster, data-driven |

| Scalability | Becomes inefficient with volume | Scales with growth |

How manual treasury operations typically work

In a traditional setup, finance teams manage multiple systems independently:

- Log in to each bank portal to access account data

- Download transaction statements from different platforms

- Consolidate data into spreadsheets or internal trackers

- Match transactions manually across systems

- Update accounting records

- Generate reports for reconciliation and review

This approach works at a small scale, but as transaction volumes grow, it becomes time-intensive, error-prone, and difficult to scale efficiently.

What efficient treasury management looks like

A modern approach replaces fragmented workflows with a centralized and integrated system.

Instead of switching between multiple bank portals, businesses operate through:

This shifts treasury operations from manual tracking to real-time, data-driven financial management.

Benefits of Moving Beyond Multiple Bank Portals

1. Real-time cash visibility

Get a consolidated, real-time view of balances across all accounts, enabling faster and more accurate cash position tracking.

2. Faster reconciliation

Automate transaction matching to reduce manual reconciliation time, improving speed and accuracy.

3. Better cash flow decisions

Access unified financial data to make informed decisions on payouts, investments, and working capital allocation.

4. Improved productivity

Free up time spent on repetitive operational tasks, allowing teams to focus on analysis, planning, and strategic initiatives.

5. Lower operational risk

Reduce dependency on manual processes, minimizing errors, inconsistencies, and reconciliation gaps.

Together, these benefits enable businesses to move from reactive financial management to a more proactive and controlled approach.

Practical Steps to Reduce Dependency on Multiple Bank Portals

1. Rationalize bank accounts

Review all existing bank accounts and identify those that are redundant or inactive. While multiple accounts may be necessary for operations or compliance, eliminating unused ones can reduce complexity.

2. Standardize financial processes

Establish consistent formats for tracking transactions, reconciliation, and reporting across all accounts to reduce confusion and manual rework.

3. Automate data collection

Where possible, replace manual downloads with automated data flows using integrations or APIs. This ensures timely and consistent access to financial data.

4. Centralize financial data

Bring data from all bank accounts into a single system or dashboard to create a reliable, unified view of financial activity.

5. Review and optimize workflows regularly

Periodically assess treasury workflows to identify bottlenecks, delays, or repetitive tasks, and refine processes as transaction volumes grow.

Common Mistakes to Avoid

- Many businesses assume that manual processes will scale with growth, but what works at a smaller scale often leads to delays and inefficiencies as transaction volumes increase.

- Over-reliance on spreadsheets is another common issue, as they become difficult to manage and more error-prone as financial operations grow in complexity.

- Delaying investment in financial infrastructure can create long-term challenges, since temporary workarounds often turn into inefficient systems that are harder to replace later.

- Ignoring reconciliation delays until audits can lead to accumulated discrepancies, making compliance more complex and increasing the risk of errors.

Simplifying Multi-Bank Operations with Connected Banking

As businesses scale, managing multiple bank portals manually becomes increasingly difficult and inefficient.

Connected banking offers a more integrated approach by bringing fragmented financial operations into a single, unified system.

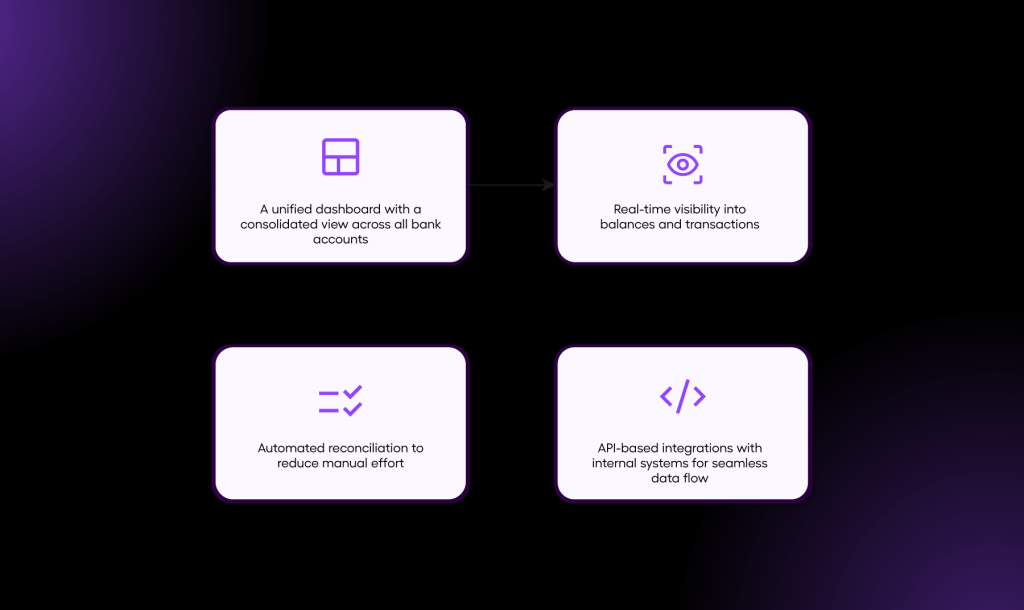

Instead of switching between multiple platforms, businesses can:

- Consolidate all bank accounts into one interface for easier access and control

- Gain real-time bank account visibility across balances and transactions

- Automate reconciliation workflows to reduce manual effort and errors

- Enable seamless financial operations through integrations with internal systems

What this means in practice

- Less time spent navigating between systems

- Faster access to accurate financial data

- Improved control over cash flow and operations

- Greater efficiency as the business scales

How OPEN Money Simplifies Multi-Bank Operations

Managing multiple bank portals doesn’t have to remain a manual, fragmented process.

OPEN Money provides a connected banking platform designed for businesses operating across multiple banking relationships, helping bring financial operations into one place.

Instead of switching between separate systems, businesses can move away from the friction of multiple logins and fragmented data and operate through a more unified approach.

- Access and manage multiple bank accounts through a single interface — without logging into multiple portals

- Track balances and transactions with improved visibility, eliminating the need to piece together data across systems

- Reduce manual effort in reconciliation and reporting workflows, minimizing errors and delays

- Integrate banking workflows more seamlessly into operations, improving overall efficiency

This connected banking approach helps eliminate the inefficiencies of multiple bank portals, improves finance team productivity, and simplifies manual treasury operations—while giving businesses better visibility and control over their finances.

Conclusion

As businesses grow, managing finances across multiple bank portals can quickly become a bottleneck rather than a necessity. What starts as a practical setup often leads to fragmented workflows, limited visibility, and increasing operational overhead. Moving toward a more connected approach not only simplifies day-to-day operations but also enables better financial control, faster decision-making, and improved scalability. For businesses looking to operate efficiently at scale, rethinking how banking workflows are managed is no longer optional — it’s a strategic priority.

FAQs

1. Why are multiple bank portals a problem for businesses?

Managing multiple bank portals can create fragmented financial workflows, limit visibility across accounts, and increase manual effort. As transaction volumes grow, this often leads to delays in reconciliation, slower decision-making, and reduced operational efficiency.

2. What is bank account visibility?

Bank account visibility is a consolidated, up-to-date view of balances and transactions across all bank accounts. Improved visibility helps businesses track cash positions more accurately and make faster financial decisions.

3. How do multiple bank portals affect finance teams?

When financial data is spread across multiple bank portals, finance teams spend more time on repetitive operational tasks such as logging in, downloading data, and reconciling transactions. This reduces the time available for strategic activities like planning and analysis.

4. What are manual treasury operations?

Manual treasury operations involve managing financial workflows using spreadsheets and disconnected systems, rather than automated or integrated tools. These processes are typically time-consuming, error-prone, and difficult to scale.

5. Can small businesses benefit from connected banking?

Yes. Connected banking can help small and growing businesses manage multiple accounts more efficiently by improving visibility, reducing manual effort, and enabling better control over cash flow as operations scale.