Running a holding company with multiple subsidiaries means you’re always dealing with one uncomfortable truth: you have money, but you rarely know exactly where it is. One subsidiary has idle cash sitting in a current account earning nothing. Another is close to overdraft. A third just missed a vendor payment because the CFO was waiting on a fund transfer that took three days to process. This is the reality of cash management for holding companies that haven’t set up a centralized financial structure, and it’s more common than most founders will admit. In fact, Deloitte’s 2024 Global Corporate Treasury Survey found that cash visibility ranks among the most cited operational challenges for finance leaders — and that’s among companies that already have a treasury team in place.

The good news is that you don’t need a treasury team of six people and an enterprise TMS to fix this. With the right approach and the right tools, a lean finance team — or even just a CFO and an analyst — can get complete cash visibility and control across 10, 15, or even 20 entities.

What Cash Management for Holding Companies Actually Means

Cash management in a single-entity business is relatively straightforward: track what comes in, manage what goes out, and maintain a buffer.

For a holding company, the same logic applies — but across multiple subsidiaries simultaneously, with intercompany flows adding another layer of complexity.

At its core, cash management for holding companies is the process of monitoring, controlling, and optimizing liquidity across all entities from a central vantage point. It includes how money moves between subsidiaries, how idle balances are deployed, how payables and receivables are tracked across the group, and how the parent company makes funding decisions without losing visibility into each entity’s position.

What makes this different isn’t just scale — it’s structure. Each subsidiary may have its own bank accounts, payment cycles, and finance owner operating independently. Without a system that brings this together, the holding company is effectively managing its finances across multiple disconnected dashboards that don’t communicate with each other.

The goal, then, is simple: replace fragmentation with a single, consolidated view of cash — supported by timely data and the ability to act on it without relying on manual reporting.

Why This Problem Gets Worse as You Add Subsidiaries

When a holding company has two or three subsidiaries, manual coordination is uncomfortable but manageable. A weekly call with each CFO, a shared spreadsheet, and a few bank logins can hold things together — barely.

Add five more entities, and the spreadsheet becomes a liability. Add ten, and the system starts to break down.

Here’s where the problems typically show up:

- Idle cash accumulates unnoticed: Each subsidiary maintains a cash buffer “just in case.” Across ten entities, these buffers add up to significant idle capital that could otherwise be redeployed for growth, debt repayment, or inter-company lending.

- Intercompany fund transfers are slow and manual: When one subsidiary urgently needs liquidity, transferring funds often involves approvals, bank portal logins, and manual NEFT/RTGS instructions — adding hours of operational lag even when the transfer itself settles quickly.

- Reconciliation becomes a month-end nightmare: Finance teams spend the last week of every month untangling intercompany transactions, matching settlements, and trying to build a consolidated view of the group’s cash position. By the time the report is ready, the data is already outdated.

- No single source of truth: The parent company’s CFO receives numbers from each subsidiary finance head — often in different formats. Comparing them meaningfully, let alone making strategic decisions, requires significant manual effort.

How Holding Companies Typically Structure Cash Management

There’s no single right way to set this up, but most holding companies gravitate toward one of three models, each with its own tradeoffs.

| Structure | How it works | Best for |

| Decentralized | Each subsidiary manages its own cash independently. The parent reviews consolidated reports periodically. | Early-stage groups with 2–3 entities and strong subsidiary finance leads |

| Centralized (Cash pooling) | Surplus cash from subsidiaries sweeps into a master account at the holding company level. Funding flows down as needed. | Mature groups with 5+ entities and predictable cash cycles |

| Hybrid | Subsidiaries manage day-to-day operations independently, but a central dashboard provides real-time visibility, and intercompany transfers are managed centrally. | Growing holding companies that want control without fully centralizing treasury |

For most Indian holding companies without a dedicated treasury team, the hybrid model hits the right balance. It doesn’t require restructuring bank accounts across entities, but it does require a platform that aggregates data from all of them into one place.

The critical shift that makes the hybrid model work isn’t organizational, it’s technological. Once you can see all subsidiary balances in real time from a single dashboard, the decisions become obvious. Without that visibility, everything is reactive.

How to Build Treasury Capability Without a Treasury Team

This is where most holding company CFOs focus: how to achieve treasury-level control without a full treasury function.

The answer lies in replacing manual coordination with automated systems — and being deliberate about which decisions require human judgment versus which can be systematized.

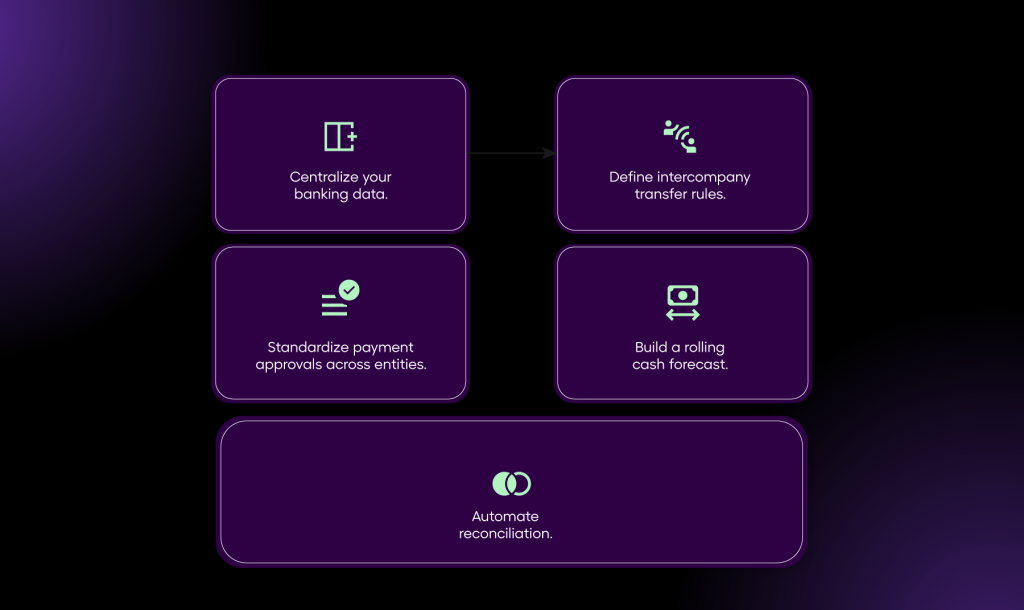

Step 1: Centralize your banking data.

Start by making all subsidiary bank accounts visible in one place. This can be done through platforms that aggregate balances via APIs or bank integrations, or by consolidating accounts with a common banking partner. The goal is a single dashboard showing live cash positions across entities.

Step 2: Define intercompany transfer rules.

Set clear thresholds. If a subsidiary’s balance drops below a certain level, it triggers a transfer. If it exceeds a buffer, surplus flows up to the parent. These rules can start manually, but should ideally be automated.

Step 3: Standardize payment approvals across entities.

Replace ad-hoc approval processes with a consistent maker-checker workflow. Payments above defined thresholds require parent-level approval, improving control without slowing operations.

Step 4: Build a rolling cash forecast.

Even a short-term rolling forecast — typically covering 4–6 weeks — provides the visibility needed to prevent liquidity gaps. With the right platform, AR and AP data can feed into forecasts automatically.

Step 5: Automate reconciliation.

Intercompany reconciliation is one of the most time-consuming tasks. Platforms that auto-tag and match transactions against ledger entries can reduce reconciliation time from days to hours.

None of these steps requires a treasury team, just a structured approach and the right platform.

How OPEN Gives You Control Over Multi-Entity Cash and Payments

Finance teams using OPEN can bring subsidiary bank accounts into a single environment — so you don’t just see balances, you can act on them without switching between bank portals or stitching together reports manually.

- Unified view of balances across entities and bank accounts

- Connected banking that reduces reliance on manual file uploads, token-based logins, and fragmented payment flows

- Intercompany and vendor payments executed from a single flow, with clear visibility into transaction status and UTR details

- Centralized tracking of all payouts with transaction-level visibility

- Beneficiary management with IFSC validation and auto-fetching of bank details to reduce errors

From intercompany fund transfers to vendor payouts across subsidiaries, your finance team gets better visibility and faster execution — without building a full treasury function.

Key Features to Look for in a Multi-Entity Banking Platform

Not every banking or fintech platform is built for the holding company use case. When evaluating tools, here’s what actually matters:

| Feature | Why it matters |

| Consolidated dashboard | View all subsidiary balances without multiple logins |

| Multi-entity account management | Manage accounts across entities under one profile |

| Role-based access control | Maintain subsidiary autonomy with parent-level oversight |

| Intercompany transfer capability | Move funds quickly with full audit trails |

| Automated reconciliation | Reduce the month-end workload significantly |

| AP/AR tracking per entity | Track payables and receivables in real time |

| Cash flow forecasting | Project liquidity across the entire group |

The one feature most holding companies underestimate is role-based access. When you give every subsidiary finance head a separate login with scoped visibility, you preserve subsidiary autonomy while maintaining parent-level oversight. It’s a small structural choice that prevents a lot of internal friction.

Conclusion

Cash management for holding companies isn’t about having a sophisticated treasury department; it’s about having the right visibility and the right structure. Most holding companies that struggle with subsidiary cash visibility aren’t under-resourced; they’re under-organized. Their cash exists across multiple accounts, multiple banks, and multiple teams — all operating without a shared system of record.

The shift from fragmented to centralized cash management starts with one decision: choosing a platform that aggregates your subsidiaries’ financial data in one place. From there, building treasury-grade control — forecasting, intercompany rules, automated reconciliation — becomes a natural next step rather than a major project.

OPEN is built for exactly this kind of business: holding companies and multi-entity groups that need enterprise-grade financial visibility without the complexity or cost of a traditional treasury management system. If you’re managing 5 or more subsidiaries and still piecing together cash positions from spreadsheets and bank emails, it’s worth seeing what a connected banking platform can do for your group.

FAQs

1. What is cash management for holding companies, and why is it different from regular cash management?

Cash management for holding companies involves tracking and controlling liquidity across multiple subsidiary entities, not just a single business. The key difference is the need for consolidated visibility — seeing all subsidiary cash positions in one place — plus managing intercompany fund flows, which don’t exist in a single-entity business. The complexity scales with the number of subsidiaries.

2. Do holding companies need a dedicated treasury team to manage cash effectively?

Many holding companies with 5–15 subsidiaries manage cash effectively with a lean team — often a CFO and a finance analyst — when supported by the right systems. A multi-entity banking platform can automate many operational tasks like reconciliation and visibility, reducing the need for a large treasury function.

3. What is cash pooling, and does every holding company need it?

Cash pooling is a structure where subsidiary cash balances are swept into a master account at the holding company level, allowing the parent to allocate funds where they’re needed. It’s useful for groups with predictable cash cycles and significant idle balances across subsidiaries. However, it adds banking complexity, so smaller or growing holding companies often benefit more from a visibility-first approach before implementing full pooling.

4. How do I get real-time cash visibility across all my subsidiaries?

The most practical approach is using a platform that integrates with your subsidiary bank accounts via APIs or bank feeds and aggregates balances into a single dashboard. This reduces the need to log into multiple banking portals or rely on manual reporting. Platforms like OPEN can support this by providing a consolidated view of accounts and transactions.

5. What’s the biggest risk of poor cash management in a holding company structure?

The most immediate risk is a liquidity mismatch: one subsidiary runs short while another holds excess cash, and the parent doesn’t catch it in time. This leads to emergency fund transfers, overdraft fees, or worse — missed vendor payments and strained supplier relationships. The underlying cause is almost always the same: no consolidated real-time view of cash across the group.