A simple question most teams can’t answer instantly

If your CFO asked right now, “What is our exact cash position across all accounts?”—would your team be able to answer immediately, with confidence?

In most enterprise setups, the answer is no.

Not because teams lack capability, but because the system they operate within doesn’t support it. Getting to that number still involves logging into multiple bank portals, downloading statements, and stitching together a consolidated view. By the time it’s ready, it reflects a position that has already moved.

This isn’t an isolated issue. According to a survey by EY, nearly two-thirds of Indian treasury teams cite weak reporting and dashboarding as a challenge, making real-time visibility difficult to achieve.

This is a pattern we see across finance teams. Visibility isn’t missing because it’s overlooked. It’s missing because it has historically been hard to solve, in large part because enterprises have lacked a unified, connected banking layer across their accounts.

And yet, it sits at the center of everything finance is trying to do today—whether that’s optimizing liquidity, improving forecasting, or adopting AI-led decision-making.

Why fragmentation persists as companies scale

Multi-bank complexity is not an exception. It’s the default outcome of growth.

As enterprises expand, they build relationships with multiple banks—driven by acquisitions, geographic requirements, and regulatory needs. Over time, this creates a distributed financial environment where each bank operates as its own system, with its own interface and data structure.

The challenge is not just the number of banks. It’s the lack of standardization across them.

Each additional relationship introduces variation in:

- Data formats and reporting structures

- Connectivity and access methods

- Reconciliation workflows

This is what treasury teams refer to as connectivity fragmentation, a state in which financial data exists but is not immediately usable.

Historically, solving this required complex integrations and long implementation cycles. So most organizations didn’t eliminate fragmentation—they adapted to it.

That adaptation now shows up as a daily operational pattern: teams logging into multiple systems, exporting data, and manually building a view of cash. It works, but only to a point—and always with a delay.

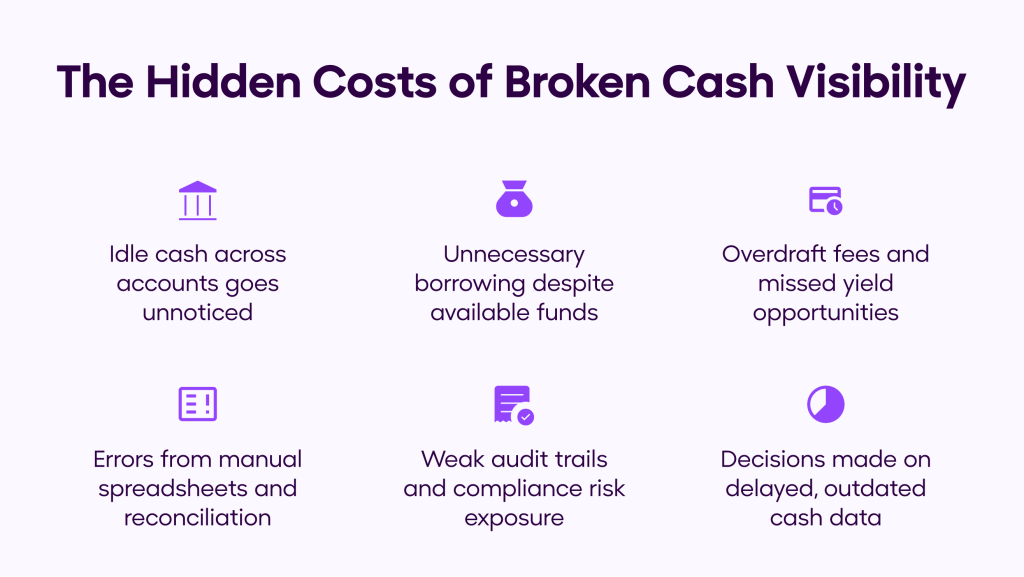

The hidden cost of not knowing your cash position

The effort of manual consolidation is visible. The financial impact is not, at least not immediately.

It shows up in smaller, recurring inefficiencies that compound over time.

Idle cash remains underutilized

When visibility is incomplete, surplus funds in one account often sit untouched while another part of the business faces a shortfall. The issue isn’t availability, it’s awareness.

Borrowing decisions become suboptimal

Organizations may take on short-term debt to meet obligations, even when sufficient funds exist elsewhere. At the same time, they may incur overdraft fees in one account while maintaining idle balances in another.

Manual workflows introduce operational risk

Spreadsheets and offline systems bring familiar challenges: version mismatches, formula errors, and incomplete audit trails. These issues often surface at the worst possible time, during audits or reporting cycles.

Decisions rely on outdated information

Perhaps the highest cost is timing. When accurate cash positions are only available after reconciliation, key decisions on payments, allocations, and liquidity are made without full context.

Individually, these may seem manageable. Collectively, they reflect a deeper issue: capital is not being deployed as effectively as it could be.

When workarounds quietly become the system

What makes this problem persistent is how it evolves.

Most teams don’t start with fragmented processes. They build workarounds to bridge gaps, shared templates, consolidation sheets, and reporting routines. Over time, these workarounds become embedded in how the team operates.

They begin to feel reliable. Familiar. Good enough.

But that “good enough” comes at a cost. Because the more these processes solidify, the harder it becomes to question them—even when the limitations are clear.

This is why many organizations continue to operate with partial visibility, despite recognizing its impact. The barrier is no longer just technical. It’s operational inertia.

What changes when visibility becomes real-time

Real-time visibility is often described as a feature. In practice, it changes how finance operates.

At its simplest, it means having a continuously updated view of all bank accounts—across entities and institutions in one place. No manual data movement. No dependency on end-of-day reports.

When that foundation is in place, the shift is immediate.

Cash management becomes more proactive. Teams can identify idle balances and reallocate funds based on current positions, rather than reacting to shortfalls.

Payment decisions become more precise. With accurate, real-time data, finance teams can manage disbursements and working capital without uncertainty.

Reconciliation becomes part of the workflow, not a separate exercise. Transaction data flows into a unified system, reducing the need for manual matching at month-end.

And importantly, forecasting improves. As finance teams explore AI-driven planning, the quality of outcomes depends entirely on the quality of inputs. Fragmented data limits what these systems can deliver. Unified, real-time data makes them effective.

This is why visibility is no longer just an operational concern. It’s becoming a strategic prerequisite.

How OPEN Enables Unified Multi-Bank Visibility

For enterprise finance teams, this is the gap OPEN’s Connected Banking platform is designed to close.

OPEN Connected Banking brings all your bank accounts into one platform—so your team can see, manage, and move funds in real time, without switching between systems.

Here’s what that looks like:

- Connected Banking Dashboard

See balances across all your bank accounts in one place, with custom identifiers for each account across 16+ supported banks. - Statements on Demand

Access and download account-level statements and transactions (credit or debit) anytime from the day of connection. - Transactions & Payments in One Flow

Initiate single fund transfers using IMPS, NEFT, RTGS, or UPI, and track every transaction end-to-end with complete details and an audit trail. - Validated Beneficiary Management

Add beneficiaries once using the account number and IFSC. Bank details are auto-fetched and validated, reducing errors during payouts.

Also Read: Connected Banking: Meaning, Benefits & How It Works

From operational visibility to strategic finance

The role of treasury is changing.

Increasingly, finance teams are expected to do more than track cash. They are expected to optimize it, supporting better capital allocation, improving returns, and enabling faster, more informed decisions.

That shift depends on one thing: having a reliable, real-time view of liquidity.

Without it, the treasury remains reactive, focused on assembling information. With it, teams can focus on using that information to drive outcomes.

This is why real-time visibility continues to rank as a top priority in treasury transformation. It is not a standalone improvement. It is the foundation that makes everything else possible.

The case for rethinking the status quo

For many organizations, visibility improvements are positioned as a future initiative—something to address after a larger system upgrade or as part of a broader transformation roadmap.

But the cost of waiting is not neutral.

Every cycle without unified visibility means:

- Capital is not fully optimized

- Decisions are made with incomplete information

- Finance teams spend time on processes that add limited strategic value

At the same time, the barrier to solving this problem has changed. Modern connected banking platforms are designed to work within existing environments, without requiring long implementation cycles or major system disruption.

This makes the decision less about transformation and more about removing a long-standing operational constraint.

Final thoughts

Finance leaders know the visibility gap exists. Most teams have adapted to it, building workarounds that keep operations running, but quietly become the process.

The real question is whether that’s still good enough.

Because fragmented, delayed visibility doesn’t fail loudly—it compounds over time. In idle capital that isn’t deployed. In avoidable borrowing and mispriced risk. In hours spent assembling data instead of acting on it.

The organizations solving this aren’t waiting for a larger transformation cycle. They’re closing the gap now using connected banking to get real-time, unified visibility without disrupting existing systems.

Unified multi-bank visibility isn’t a feature to add later. It’s the foundation modern finance depends on.

And for teams still managing that foundation manually, it’s worth asking:

What would change if “What is our cash position right now?” had an immediate, reliable answer?

Ready to see your complete cash picture? Book a Free Demo

FAQs

Why do large enterprises still lack unified multi-bank visibility?

Historically, each bank operates as its own system with different data formats and connectivity protocols. Building unified visibility traditionally required months of complex integrations. Connected banking platforms like OPEN now solve this significantly faster, without displacing existing banking relationships.

How does OPEN Connected Banking differ from a standard ERP treasury module?

ERP treasury modules typically require deep system integration and still rely on end-of-day bank feeds. OPEN creates a unified, real-time operational layer across multiple bank accounts without requiring ERP reconfiguration, making it faster to deploy and immediately effective.

Is unified visibility a prerequisite for AI-driven cash forecasting?

Yes. AI forecasting is only as accurate as the data feeding it. Fragmented, manually consolidated bank data produces inconsistent, unreliable outputs. Unified, real-time data is what makes AI-driven treasury intelligence actually actionable.