Cash flow management has always been central to finance operations. But in most enterprises, it is still reactive.

Despite the growing focus on AI in finance, adoption remains limited. According to the Economic Survey of India, based on Reserve Bank of India findings, only 21% of Indian financial institutions are actively implementing or developing AI for core operations. For most teams, the challenge is not intent but the lack of connected, real-time financial data needed to make AI effective.

Finance teams log into multiple bank portals, reconcile transactions at the end of the day or week, and often discover cash gaps only when payments are delayed or fail. At a smaller scale, this approach works. At enterprise scale, it breaks.

Because by the time you act, the problem has already occurred.

This is where the shift to predictive cash flow management begins—not by adding more reports, but by combining AI cash flow forecasting with real-time treasury visibility.

Why Predictive Cash Flow Management Requires Real-Time Visibility

Predictive cash flow management depends on one thing: accurate, real-time data.

In reality, most finance teams operate in fragmented environments. Bank accounts are spread across entities, transactions sit in disconnected systems, and reconciliation is still heavily manual. What should be a simple question—“What’s our cash position right now?”—often requires multiple logins, downloads, and manual consolidation.

This fragmentation does more than slow teams down. It introduces risk into everyday financial decisions.

Cash flow blind spots delay vendor payments. Idle balances sit unnoticed in one account while another runs short. Capital allocation decisions are made on partial visibility, not complete data.

At this point, faster reporting doesn’t solve the problem. What finance teams need is real-time treasury visibility across all bank accounts, without switching systems.

The Limits of Reactive Cash Flow Management in Multi-Bank Environments

Reactive cash flow management is built on historical data. You look at what has already happened and decide what to do next.

That model starts to break down in multi-bank environments, where cash positions change continuously, and payment activity is distributed across systems. By the time data is consolidated, it is already outdated.

At enterprise scale, this delay compounds quickly. Missed payment cycles, idle capital, and last-minute fund transfers become recurring patterns—not exceptions.

The issue is not effort. Most teams are already doing the work. The issue is that the data needed for decision-making is not connected in real time.

What Is Multi-Bank Data Integration in Cash Flow Management

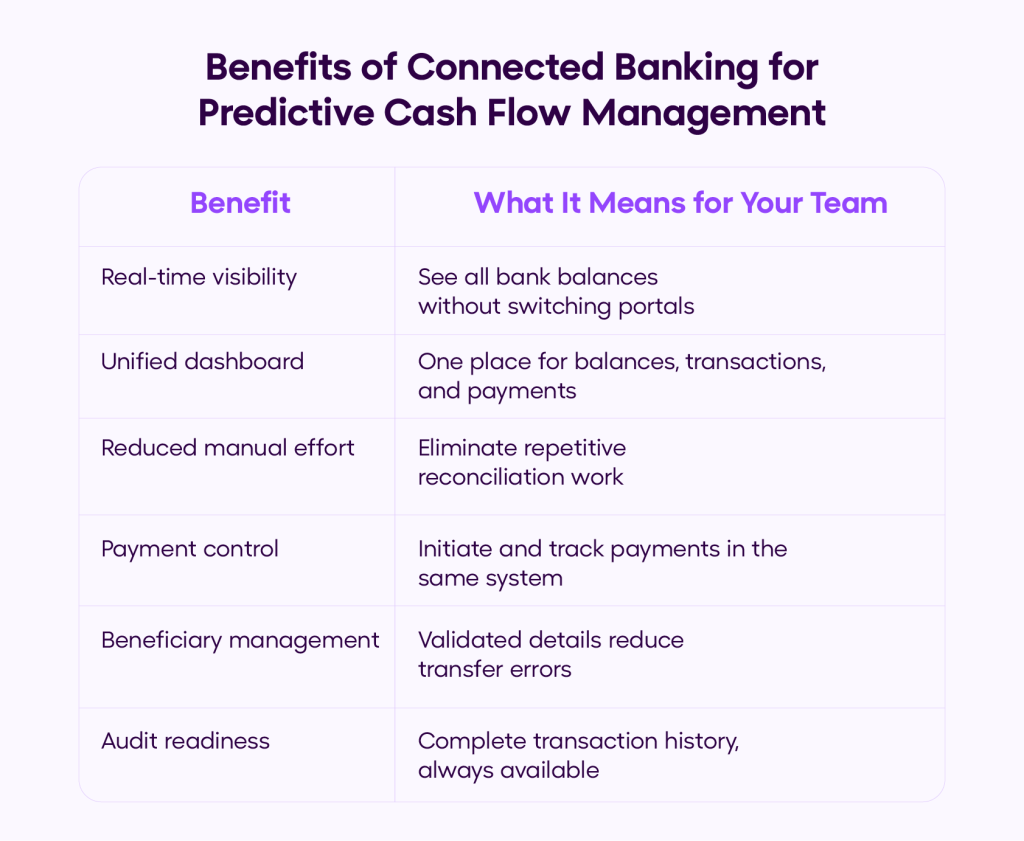

Multi-bank data integration connects all your bank accounts into a single platform, enabling centralized access to balances, transactions, payments, and statements in real time.

This is where connected banking becomes critical. It creates a unified layer across all your banking relationships, without requiring teams to rely on multiple portals or fragmented workflows.

In practice, this changes how finance teams operate:

- Centralized control: All bank accounts are managed in one place

- Automated workflows: Payments and reconciliation no longer depend on manual effort

- Real-time visibility: Live access to balances and transaction status

- Standardized access: A single interface replaces multiple banking systems

How Connected Banking Enables Real-Time Treasury Visibility

Connected banking replaces fragmented banking operations with a unified system.

Instead of logging into multiple bank portals, finance teams operate from a single dashboard that brings together balances, transactions, and payments across accounts. This creates a consistent, real-time view of cash positions across the organization.

The impact is immediate. Teams no longer spend time gathering data before making decisions. They operate with a clear, current view of liquidity—and can act within the same system.

The result is not just efficiency.

It is clarity and control over cash flow in real time.

How AI Cash Flow Forecasting Works with Unified Financial Data

Once visibility is solved, the next step in predictive cash flow management is intelligence.

AI cash flow forecasting works by analyzing unified financial data across accounts, transactions, and payment patterns. But its effectiveness depends entirely on data quality and timeliness.

In fragmented environments, forecasting remains limited. When financial data is connected in real time, AI becomes significantly more accurate and actionable.

With the right data foundation, AI can:

- Forecast short-term liquidity gaps

- Identify idle funds across accounts

- Detect anomalies in transaction behavior

- Predict delays in payments or collections

This is the shift from visibility to foresight—where finance teams can act before issues occur.

What This Looks Like in Practice

Consider a finance team managing multiple bank accounts across entities.

Without connected systems, their workflow involves logging into multiple portals, downloading statements, and consolidating data manually. By the time decisions are made, the information is already outdated.

With connected banking and AI-driven forecasting, the same workflow changes.

Balances are visible in real time across all accounts. Upcoming obligations are factored into projections. Potential shortfalls are identified early, allowing teams to reallocate funds proactively. Reconciliation happens automatically in the background.

The difference is not the amount of work.

It is when the team finds out and what they can still do about it.

From Reactive to Predictive: What Actually Changes

| Dimension | Reactive | Predictive |

|---|---|---|

| Cash position | Assembled after the fact | Live, across all accounts |

| Forecasting basis | Historical, delayed data | Real-time financial inputs |

| Liquidity gaps | Discovered during execution | Identified in advance |

| Idle capital | Unnoticed across accounts | Actively identified and deployed |

| Payments | Initiated across multiple portals | Unified workflow |

| Reconciliation | Manual, time-intensive | Automated, near real-time |

| Risk detection | Reactive | Proactive |

This shift is not just operational. It changes how finance teams make decisions.

The Compliance and Audit Case for Connected Banking

Most discussions of connected banking focus on efficiency and forecasting. The compliance case is equally strong and often more persuasive to CFOs evaluating enterprise platforms.

In fragmented banking environments, audit trails are assembled after the fact. Statements are pulled from multiple portals. Payment records are matched manually. Beneficiary details are stored inconsistently across systems. When an auditor or regulator asks for a complete transaction history, the answer involves days of manual work.

Real-time, connected banking changes this by design:

- Every transaction is logged the moment it occurs, with user-level attribution — who initiated it, when, from which account.

- Beneficiary bank details are validated at setup — IFSC verification pulls and confirms account information automatically, reducing the risk of fraud and erroneous transfers.

- Statements are available on demand for any account, any date range — no portal logins, no emailed requests, no waiting.

- Role-based access controls ensure that payment initiation, approval, and audit access are separated — creating the kind of internal control structure that auditors look for.

For enterprises managing across multiple states, entities, or regulatory jurisdictions where GST reconciliation, TDS compliance, and RBI reporting overlap, having all transaction data centralized and timestamped is not a convenience. It is a requirement.

Also, Connected banking provides the operational foundation required for predictive finance.

Individually, these improvements increase efficiency. Together, they make predictive cash flow management achievable at scale.

How OPEN Enables Connected Banking for Enterprises

Closing the gap between visibility and prediction requires a system where financial data and workflows are inherently connected.

OPEN provides that layer.

Instead of working across fragmented systems, teams operate in one consistent environment—where visibility and execution come together.

One platform. Every bank account. Real-time control.

Final Thoughts

AI is often positioned as the future of finance. But it is not the starting point.

The real shift begins with connected, real-time financial data.

Without that foundation, forecasting remains reactive, decisions remain delayed, and finance teams operate with partial visibility. But when data across bank accounts, transactions, and payments is unified, the nature of cash flow management changes entirely.

Visibility becomes immediate. Decisions become proactive. Risk becomes manageable.

Predictive cash flow management is not just about better forecasting. It is about operating with clarity, confidence, and control in real time.

And for enterprises managing multiple bank accounts, connected banking is what makes that possible—today.

FAQs

What is predictive cash flow management?

Predictive cash flow management uses real-time financial data and AI to forecast future cash positions, enabling finance teams to anticipate risks, optimize liquidity, and make proactive decisions — rather than reacting to problems after they occur.

How does AI improve cash flow forecasting accuracy?

AI improves forecasting by continuously analyzing transaction data, AP/AR aging, payroll schedules, and historical patterns — updating projections in real time rather than relying on static models. The more unified and current the input data, the more accurate and actionable the forecasts become.

Why is real-time data critical for cash flow forecasting?

Without real-time data, forecasts are built on yesterday’s numbers. By the time a gap is identified, there may not be enough lead time to act. Real-time visibility means projections reflect actual cash positions as they are — not as they were when statements were last downloaded.

What is the difference between connected banking and ERP integrations?

ERP integrations typically sync bank data periodically — often once daily — and route payments through multiple systems. Connected banking provides a direct, live link to the bank: balances are current the moment you check, and payments are executed within the same platform without additional routing.

Can predictive cash flow management reduce idle capital?

Yes. By identifying surplus balances across accounts and forecasting upcoming cash requirements, finance teams can reallocate funds more efficiently and reduce idle capital.

How quickly can enterprises implement connected banking?

Implementation timelines vary, but modern connected banking platforms are designed to integrate with multiple banks and systems with minimal disruption, enabling faster adoption compared to traditional ERP-led approaches.