The Problem No One Talks About at the Leadership Table

It’s the 5th of the month. Your collections team is chasing repayment confirmations across multiple bank portals. Your finance controller is still reconciling disbursement records from escrow accounts, trying to explain a cashflow gap in the settlement report without real-time numbers to back it up.

Sound familiar?

This isn’t a technology failure. It’s an operational blind spot, one that quietly grows as NBFCs scale.

Add more banking partners, co-lending setups, and LSP relationships, and suddenly tracking money isn’t straightforward anymore. Where did it go? When did it move? Did it come back?

Instead, teams are left stitching together MIS reports, hopping across multiple bank portals, and manually tagging transactions — a process that was never built for this kind of scale.

This is exactly the problem that connected banking for NBFCs is designed to solve. And with the RBI mandating direct fund flows between lenders and borrowers, real-time visibility into disbursements and repayments isn’t just a nice-to-have anymore — it’s a compliance requirement.

What Is Connected Banking for NBFCs?

Connected banking is the integration of multiple bank accounts, current accounts, escrow accounts, and co-lending settlement accounts into a single API-driven infrastructure. Instead of managing each bank relationship in isolation, connected banking brings all fund movements under one operational layer.

For an NBFC, this translates to:

- Disbursement instructions triggered from a single system, executed across multiple banks

- Repayments from borrowers landing in the correct NBFC account, tracked and tagged in real time

- Co-lending settlements are handled automatically, without manual split calculations

- Reconciliation that runs continuously, not overnight, in a spreadsheet

It’s the financial operating system that sits beneath your LOS (Loan Origination System) and LMS (Loan Management System), ensuring every rupee is accounted for, in motion, or flagged for action.

Why Multi-Bank NBFC Operations Create Visibility Gaps

Most NBFCs don’t choose complexity; they grow into it. One bank relationship is manageable at 500 disbursements a month. But as lending volume scales and product types multiply, you end up with multiple accounts across different banks for different use cases, multiple LSPs routing collections differently, and a compliance mandate requiring every fund flow to stay strictly between the borrower and the NBFC.

The result is fragmented visibility:

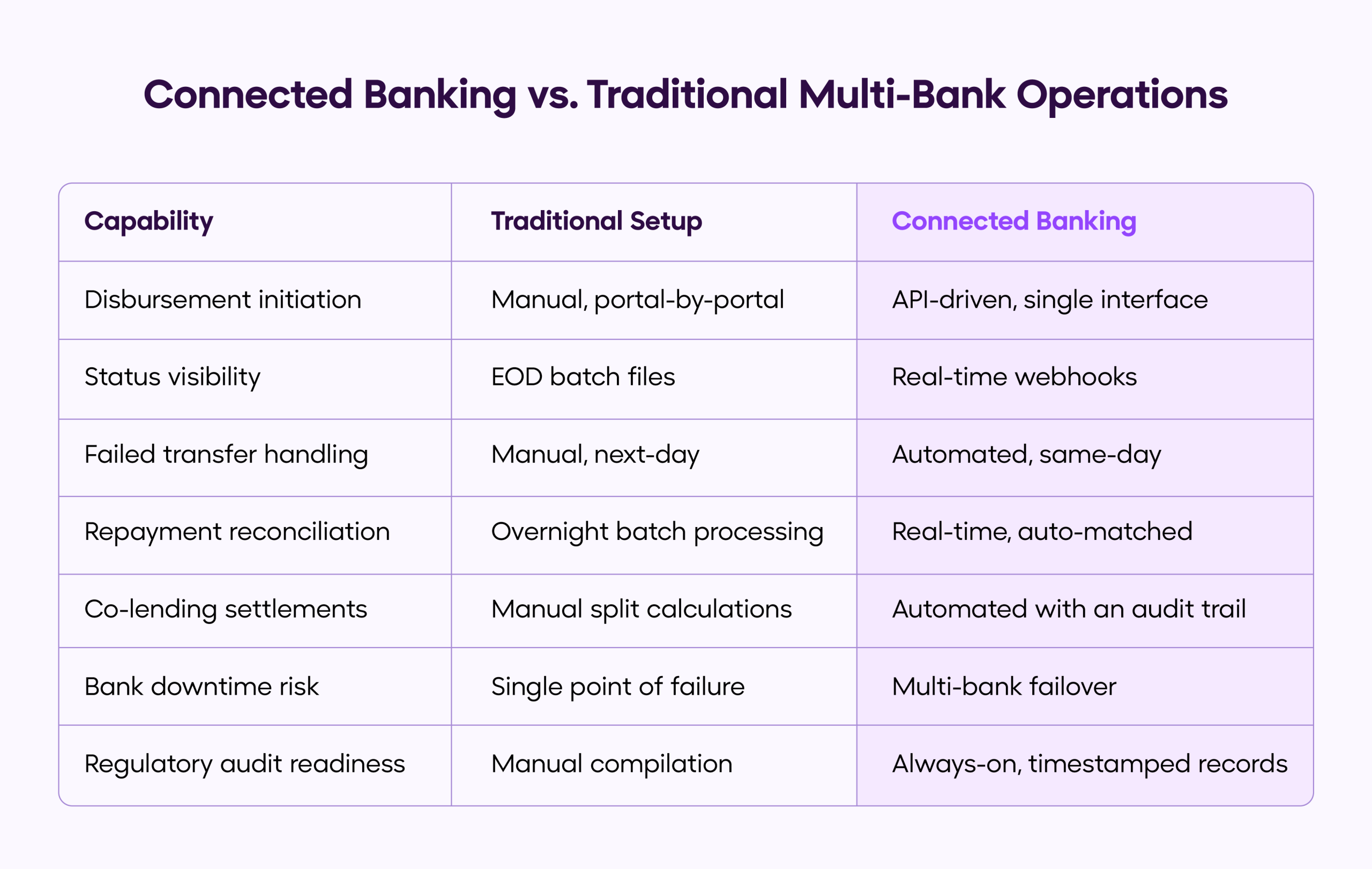

| Operational Challenge | The Manual Reality |

|---|---|

| Disbursement confirmation | Download statements from each bank portal, cross-check LMS manually. |

| Repayment tracking | Wait for EOD batch files from banking partners. |

| Failed transfer reconciliation | Manual calls, next-day resolution. |

| Co-lending settlements | Separate manual reconciliation run per partner. |

| Regulatory reporting | Pieced together from multiple disconnected data sources. |

Every hour spent here is an hour not spent on underwriting, collections strategy, or portfolio growth.

The RBI Compliance Angle

Connected banking isn’t only an efficiency story; it’s a regulatory one.

Under the RBI’s Digital Lending Directions (updated May 2025), the rules are unambiguous: loan disbursements must be made directly into the borrower’s bank account, and repayments must flow directly to the NBFC’s account. No pass-through accounts, no LSP-controlled fund movement, no exceptions outside of a few specific co-lending carve-outs.

In practice, this means:

- Every disbursement must be traceable from instruction to execution

- Every repayment must land in the NBFC’s account with same-day reconciliation capability

- Any routing error or failed transfer must be caught and corrected immediately

- Co-lending transactions require precise split accounting between lending partners

NBFCs relying on EOD batch files and manual tagging to demonstrate compliance are exposed. A verified, timestamped audit trail, not a morning report, is what holds up under regulatory scrutiny.

Key Capabilities: What Real-Time Visibility Actually Requires

Effective disbursement tracking and repayment visibility across banks isn’t just API connectivity. It requires a layered approach:

Multi-Bank Payout Infrastructure: Route disbursements from a single interface across multiple banking partners, with automatic failover if one bank faces downtime.

Pre-Disbursement Account Verification: Verify borrower bank accounts before any transfer is initiated, through penny drop or UPI validation, to prevent failed credits and reversal delays.

Real-Time Status Webhooks: Instead of waiting for batch files, receive disbursement status initiated, processing, credited, or failed the moment it changes, directly into your LMS.

Automated Reversal Reconciliation: Failed transfers should trigger automatic reversals and re-attempts, with human review reserved for exceptions only.

NACH/UPI AutoPay Integration: Real-time mandate status, bounce notifications, and repayment-to-loan auto-matching so collections teams know about NACH failures at 9 AM, not the following morning.

Co-Lending Settlement Engine: Automatic repayment splits between NBFC and co-lending partners in the agreed ratio, with settlement records maintained for both sides.

The scale of this problem is only growing. According to CRISIL MI&A, NBFC credit is projected to grow at a CAGR of 15–17% between FY2024 and FY2027 — and as disbursement volumes increase, the cost of manual fund flow management grows disproportionately more staff, more errors, slower MIS, and higher compliance exposure. The operational leverage of automated, real-time visibility compounds with scale.

Connected Banking vs. Traditional Multi-Bank Operations

The difference isn’t marginal. It’s the difference between managing operations reactively and leading them with precision.

How Open Helps NBFCs Take Control of Fund Flows

Managing fund flows across multiple banks shouldn’t require your team to live across multiple portals. Open’s connected banking platform brings all your bank accounts, transactions, and payments into one unified layer — giving you real-time visibility and control from a single interface.

- Unified visibility: Track balances and transactions across multiple banks from a single dashboard

- Centralized payments: Initiate disbursements and payouts via IMPS, NEFT, RTGS, or UPI with complete audit trails

- On-demand statements: Access and download account statements anytime, without relying on bank portals

- Faster reconciliation: Consolidated transaction data reduces manual effort and speeds up reconciliation

- Audit-ready records: Every transaction is timestamped and logged for easy reporting and compliance

- Multi-bank control: Operate across 16+ banks through one interface, without added complexity

Bring clarity and control to your multi-bank operations.

FAQs

1. What is connected banking for NBFCs?

It’s the integration of multiple bank accounts, disbursement, escrow, and collection through APIs into a single operational layer. NBFCs can manage all fund flows, track disbursements, collect repayments, and reconcile across banks without portal-hopping or waiting for batch files.

2. How does disbursement tracking work across multiple banks?

Disbursement instructions are issued centrally and executed through the appropriate bank via APIs. Status updates — credited, failed, or reversed are returned in real time through webhooks, and all movements are logged with timestamps for audit purposes.

3. Can repayment visibility work for NACH and UPI AutoPay?

Yes. Connected banking platforms integrate with NACH and UPI AutoPay infrastructure, providing real-time mandate status, payment confirmations, and bounce notifications. Repayments are auto-matched to loan records without manual intervention.

4. How does this support RBI digital lending compliance?

The RBI mandates that all disbursements and repayments flow directly between the borrower’s and NBFC’s bank accounts, with no intermediaries. A connected banking platform enforces this routing and maintains immutable transaction logs that demonstrate compliance during audits.

5. Can co-lending repayment splits be automated?

Yes. Repayments can be automatically split between the primary NBFC and its co-lending partner in the agreed ratio, with settlement records maintained for both parties at the time of receipt, not retrospectively.

6. What happens if a banking partner has downtime?

Connected banking platforms with multi-bank support include automatic failover. If the primary bank is unavailable, disbursements are routed through a configured backup bank, ensuring continuity without borrower-facing delays.