Recently, there was a lot of buzz around how the RBI has found four viable products for cross-border payments under its regulatory sandbox. Many of our readers and colleagues didn’t know/hadn’t heard of ‘Regulatory Sandbox. In this blog, we deconstruct what a regulatory sandbox is and how it shapes the disruption in the traditional financial sector. It means more innovative products become accessible, and whatever product these fintech giants have created is in line with the regulations that protect customers’ interests.

India is a hotbed for fintech innovation and houses more than 4200 fintech startups. With so many fintechs around, it was imperative to regulate fintech disruption so that the interest of the Indian consumers stays safe and innovations remain accessible, which gave birth to the regulatory sandbox.

So, we will discuss the regulatory sandbox in general, then gradually deep dive into the RBI’s regulatory sandbox journey. We will also discuss how it shaped the fintech industry we see today. However, if you want to jump into specific sections directly, you can use the content table at the top.

What is a Regulatory Sandbox?

Sandboxes operate under specific regulatory exemptions, allowances, or limited time-bound exceptions. The regulatory sandbox entered an era of rapid technological innovation in financial and BFSI markets. It manages the contentions between regulators’ urge to motivate and facilitate fintech innovation and regulatory goals such as economic resilience and consumer protection.

Simply put, a regulatory sandbox is a highly controlled environment provided by the central financial body to fintechs/financial institutions to test out newer concepts and innovations before launching to the majority of the public. Therefore, financial regulatory bodies of individual nations have set up sandboxes for fintech innovation within the regulatory boundaries.

Now that we understand the regulatory sandbox in definition, we will dive into the imagination and inception of the RBI Regulatory Sandbox.

RBI Regulatory Sandbox

After UPI’s launch and demonetization implementation, RBI saw 4 trillion UPI transactions and 55 trillion Aadhaar authentications. These events signaled that India was already at the cusp of completely digitizing its banking system. The nation won’t lag behind its international counterparts if proper steps are taken to grow financial technology. More importantly, it had to be done within the regulatory framework while keeping the best interest of the Indian population in mind.

Financial capitals like the UK, Europe, the USA, and many others were already in the advanced stages of their banking sectors’ digital transformation. They had created a structurally sound and flexible environment for businesses to test financial innovation called regulatory sandboxes.

2016 RBI Working Committee for Deciphering Fintech Regulatory Challenges

In July 2016, RBI set up a Working Committee consisting of 13 individuals to unearth the regulatory challenges faced by the fintechs and digital banks in India. The working committee submitted the report on November 23, 2017. Below are the recommendations submitted by the Working Committee:

- Before regulating this space, there is a need to have a deeper understanding of various FinTech products and their interaction with the financial sector and, thereby, the implications on the financial system.

- The regulatory actions may vary from “Disclosure” to “Light-Touch Regulation & Supervision” to a “Tight Regulation and Full-Fledged Supervision,” depending on the risk implications.

- There is a need to develop a more detailed understanding of risks inherent in platform-based FinTech.

- Financial sector regulators must identify sector-specific FinTech products and regulatory approaches.

- Adopting digital channels to replace time-consuming manual processes empowers the workforce of customers and the insurance sector.

- Innovation labs, including insurance companies, may be established to combine brand and product managers with technological and analytical resources.

- When Fintech players introduce any securities market products, regulators may assess the product and see whether SEBI or RBI can monitor it by registering them as an intermediary or through the activity regulations.

- Insurance companies may collaborate with “Insurtech” entities or startups to provide a better and more cost-effective customer experience.

- Financial sector regulators must engage with FinTech entities to chalk out appropriate regulatory responses and re-align regulation and supervision in response to the changing environment.

- A’ dedicated organizational structure’ within each regulator needs to be created to identify and monitor the challenges associated with developing significant FinTech innovations and respond to opportunities and risks arising for the financial system from these innovations.

- To provide an environment for developing FinTech innovations and testing applications/APIs designed by banks and FinTech companies.

- RBI may introduce an appropriate framework for a “Regulatory Sandbox/innovation hub” within a well-defined space and duration. The financial sector regulators will provide the requisite regulatory support to increase efficiency, manage risks and create new opportunities for Indian consumers within regulatory jurisdictions.

- Because of IDRBT’s unique positioning as a research and development institute, due to its activities, IDRBT is well placed to create and maintain a regulatory sandbox in collaboration with RBI to enable innovators to experiment with their banking/payments solutions for eventual adoption. The Institute may continue to interact with RBI, banks, and solution providers regarding testing new products and services and, over time, upgrade its infrastructure and skill set to provide a full-fledged regulatory sandbox environment. The Reserve Bank of India may actively engage with the Institute.

- Regulatory and legal reforms are essential for the sustainable development of the digital financial industry.

- Partnerships/engagements among regulators, existing industry players, clients, and FinTech firms will enable the development of a more dynamic and robust financial services industry.

- Regulators may explore using Reg-Tech to facilitate the delivery of regulatory requirements more efficiently and effectively than existing capabilities.

- RBI must reorient regulators’ organizational structure and human resources (HR) practices to meet innovation challenges regarding adapted HR hiring profiles, learning, and educational programs.

- There is a need for stand-alone data protection and privacy law in the country.

- Banks / Regulated entities may be encouraged to collaborate with FinTech/startups to improve their customer experience and operational excellence. They may also consider undertaking FinTech activity in payments, data analytics, and risk management.

- Models of engagement and checklist to be developed by each regulator for each activity.

- Given that FinTech companies are in their infancy but growing, the Government may consider introducing tax subsidies for merchants that accept a certain proportion of their business revenues from digital payments.

- All market regulators should highlight the requirement of increasing the levels of education/ awareness of customers.

- A self-regulatory body for FinTech companies may be encouraged.

The above recommendations laid the foundation for the first draft of the Indian regulatory sandbox. RBI launched the final framework for Regulatory Sandbox on August 13, 2019. That is how the regulatory sandbox for Fintechs, Insurance-techs, and Regtechs looking to make financial innovations came into being in India.

Cohorts and Choosing the Right Fintechs to Spearhead Innovation

Accordion to RBI, fintech companies, including startups, banks, financial institutions, and other companies partnering with or providing support to financial services businesses, can apply for entry into the regulatory sandbox. They will be subject to the below sandbox criteria.

The focus of the regulatory sandbox will be to encourage innovations intended for use in the Indian market in areas where:

- Required governing regulations are absent;

- There is a need to ease restrictions to enable the proposed innovation temporarily;

- The invention shows promise of easing/affecting the delivery of financial services in a significant way.

RBI chose to break down the schedule of intake of fintechs into cohorts. Each cohort will comprise a group of fintechs focused on innovation in specific sectors based on themes like retail payments, cross-border payments, MSME lending, and mitigating financial fraud. We can see an elaborate list of all the cohorts on the RBI website.

Recently RBI announced the list of fintechs that successfully exited the second cohort. The second cohort focused on enabling cross-border payments to exchange remittances quickly.

India accounts for 15% of the global share in remittances, making it the largest recipient of inbound remittances globally. In 2019, India received $83 bn, and in the first half of 2020 received $27.4 bn. The daily turnover of OTC foreign exchange instruments in India is approximately $40 bn. By leveraging new technologies faster, the cohort needed to spur innovations for a low-cost, secure, convenient, and transparent system for cross-border payments.

In this cohort, RBI selected eight entities to test the boundaries of cross-border payments technology in a sandbox environment. This test can last for seven months to a year. Each section is divided into four weeks, each lasting from 4 weeks to 12 weeks. The participating entities are supported(relaxing regulations) and scrutinized(gauging performance and profitability) during each section to ensure that RBI can form appropriate rules. IDRBT doesn’t tolerate any entities’ failure in any of the test sections. These stringent measures provide filtering and keep only a few capable fintechs that can drive innovation and create customer value.

In the second cohort of eight, only four fintechs passed the test:

- Open Financial Technologies Private Limited:

Open is an all-in-one business banking platform. Open helps manage banking, payments, accounting, expense management, taxes, and loans in one place. Open proposed blockchain-based frictionless and tamperproof monitoring capabilities for a cross-border payment system that leverages current infrastructure. - Fairex Solutions Private Limited:

Fairex is an aggregation platform of leading cross-border payment providers for outward remittance. - Nearby Technologies Private Limited:

‘Paynearby,’ a product of Nearby technologies, facilitates routing the inward cross-border remittance to the beneficiary’s Aadhaar number as a virtual bank account using the existing RDA mechanism. - Cashfree Payments India Private Limited:

Cashfree’s cross-border payment platform facilitates Indian investors to purchase assets like publicly listed shares and exchange-traded funds listed via local payment methods on foreign exchanges.

Impact of RBI Regulatory Sandbox

After introducing the RBI regulatory sandbox to the players in the fintech space, the fintech environment has undergone drastic changes. These changes are listed below:

Drive Innovation and Research

The Indian fintech industry has made a lot of innovations in the last few years, such as QR Codes, NFC enabled Cards, Instant Settlements, and Video KYC. The QR code, once used to track luggage, was repurposed and is now used to make instant UPI transactions. RBI introduced QR codes with much fanfare. It was slow to take off. However, now we see stickers stuck at every shop, taxi, and bus to make faster cashless payments.

Similarly, the NFC cards gained traction during Covid-19 when all the transactions were supposed to be contactless. Keep the card near the PoS terminal, and the correct amount of money will be deducted from the card balance.

Instant Settlement is a boon in disguise. With billions of transactions happening daily, it had become imperative to have a similarly fast settlement process. With UPI and IMPS from NPCI, settling accounts and making instant transfers to bank accounts instead of any wallet became easy.

Video KYC will be groundbreaking innovation for the credit card industry as identity verification is a vital process before disbursing credit. However, given the manual method, establishing an individual’s identity took a long time. The Video KYC process has made identity verification faster.

AePS or Aadhaar enabled Payment System is where biometrics information is integrated into the Aadhaar system, which is then linked to all the bank accounts that financial institutions can use for authentication and make faster payments.

Promote Growth

With all the innovative products in the market, the time required for tiring operations has become shorter, enabling SMEs and other businesses to have more time on their hands. With this extra time, they can focus on innovating their product or marketing, which needs a lot of mental space and time.

For example, if a business has a single place where they can manage their banking transactions, bills, invoices, payroll, accounting, and taxes would be so amazing. They could also take loans, and the ability to see how effectively they have been running their business when required will be bliss. The company can focus on activities promoting growth with the time saved.

Keep Customers’ Interests Intact

It is in the interest of the regulatory sandbox to pass the fintech or financial institutions that don’t dilute customers’ interest in innovation. Therefore, RBI puts necessary data privacy policies and regulations to protect customer data. Applicants for sandbox must comply with the following regulatory requirements to ensure the interests of consumers and the safety and soundness of the financial sector:

- Confidentiality of customer information

- Fit and proper criteria

- Handling of customers’ money and assets by intermediaries

- Prevention of money laundering and countering the financing of terrorism,

- The Number of customers

- Transaction volume

- Specific customer groups

- Information to customer

Expand Financial Inclusion

The regulatory sandbox aims to extend the financial instruments’ reach to the less privileged. Spreading awareness among customers to empower them with the latest tech and improve their life is something that RBI wants to achieve. Several fintechs target niche customer segments not only for competitive advantage but also as a part of the RBI sandbox guidelines.

India is the country with the second highest internet penetration globally. And yet, 1 out of 5 Indians don’t have access to essential banking services. It is a challenge and an opportunity to make financial services accessible to the unbanked. With innovations in technology, financial services are accessible after minimal paperwork, one of the biggest challenges that fintechs overcame. Take gold, for example. India privately holds $1.5 trillion in gold in assets, mainly acquired through unsecured loans. Therefore, it is an excellent opportunity to extend tech-driven credit services as it requires less investment from fintech and less paperwork to attract people to gold loans. Fintechs can explore one of many opportunities to make financial instruments more accessible.

Attract Investments

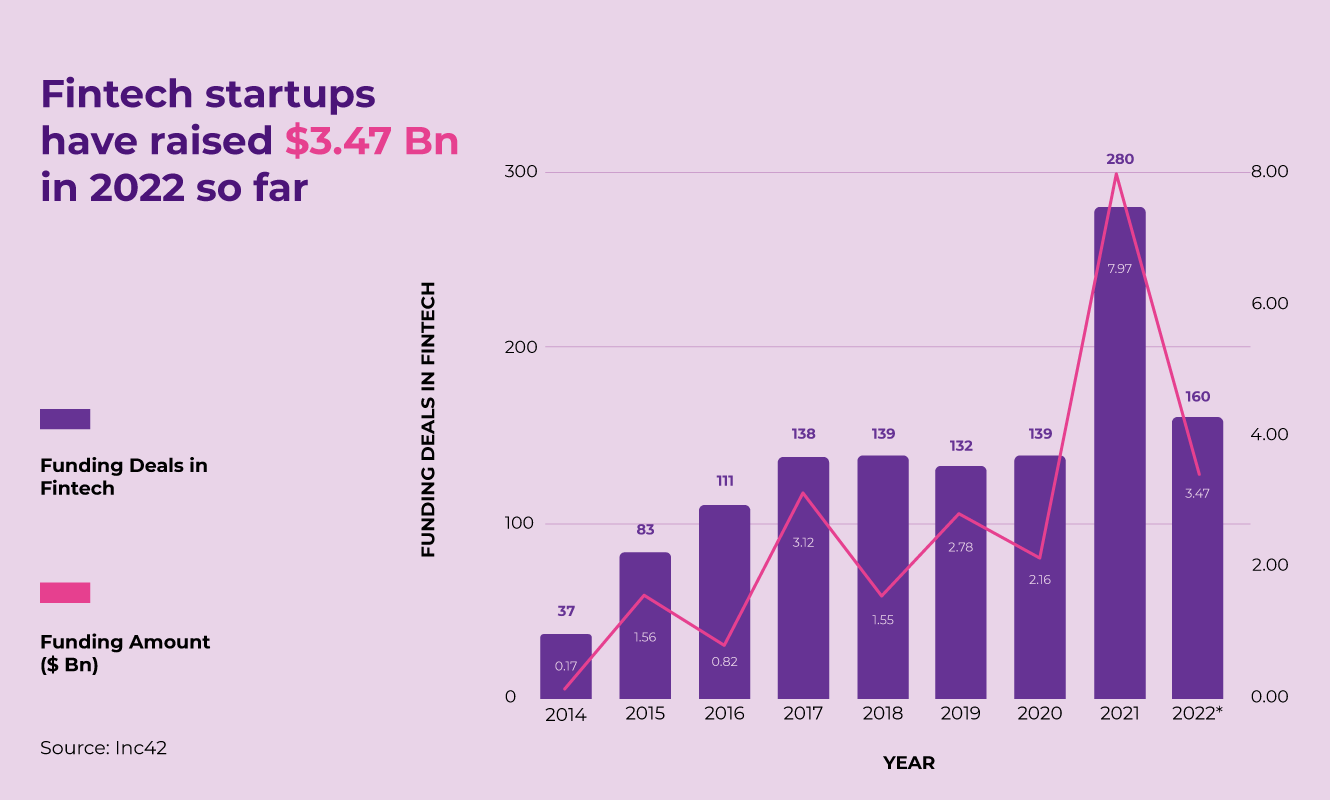

The fintech industry has received close to $23.6 billion between 2014 and 2022. The top 30 investors did 676 of the 1219 funding deals in the space, and 14 investors among these were from the US.

If you look closely at the graph, there was a steady rise in investments after 2016. RBI set up the Working Committee to understand the Fintech industry in 2016. As time progressed and RBI set up the regulatory framework in 2019, there was a slight dip because fintech regulations were still developing, and Covid-19 struck India.

Covid forced banks and financial institutions to evolve and make financial services accessible to the unbanked. It was a challenging as well as an excellent opportunity for fintechs to come up with innovative products and services. These immense opportunities attracted funding that exploded in the year 2021.

Build Sound Regulations

With great power comes great responsibility. Fintechs and other financial institutions reaped significant benefits in the opportunity created due to the pandemic and made financial instruments accessible to the unbanked.

The regulatory sandbox ensured that the fintechs delivered what was promised and never fell short of it. However, the regulatory sandbox also saw fintechs’ offerings, and if any, regulation became a hindrance rather than a support system. They made tweaks accordingly, keeping in mind the interest of fintechs and consumers.

Conclusion

RBI Regulatory Sandbox has played a significant role in shaping the fintech industry, nurturing and guiding the fintechs in the right direction while keeping the interest of the consumers in focus. The thematic-based framework is inspired by regulatory sandboxes across various financial capitals globally, and it never falls sort of any expectations so far. Moreover, the sandbox has helped financial institutions go in the right direction to empower the unbanked and draw the attention of suitable investors.

It has helped acquire not only newer technology but also deepened the market penetration of the financial instruments in the Indian market by offering services at lower prices.