Every time you transfer money online, there’s a small but critical detail that ensures it reaches the right bank account—the IFSC code. Issued by the Reserve Bank of India (RBI), this code helps identify the exact bank branch involved in a transaction.

From NEFT, RTGS, to IMPS payments, IFSC codes act as a digital routing system that ensures secure and error-free fund transfers. Whether you’re adding a beneficiary or verifying bank details, understanding how IFSC codes work can help you avoid delays and failed transactions.

What is an IFSC Code?

The Indian Financial System Code (IFSC) is an 11-character alphanumeric code that uniquely identifies specific bank branches in India. Each IFSC code is unique to a branch, ensuring that money transfers are error-free and accurate.

This unique code is assigned to each bank branch participating in the country’s electronic payment system. Its primary purpose is to streamline digital transactions such as NEFT, RTGS, and IMPS, making them faster, safer, and more efficient.

Key Facts About IFSC:

- Length: 11 characters (alphanumeric)

- Issuing Authority: Reserve Bank of India (RBI)

- Uniqueness: Every bank branch has a unique IFSC

Scope: Applicable across all electronic payment systems in India

How IFSC Codes Work in NEFT, RTGS, and IMPS

Here’s a simple step-by-step look at how IFSC codes work in online bank transfers:

Step 1: Enter Recipient Details

To initiate a transfer (NEFT, RTGS, or IMPS), you need:

- Account number

- Account holder name

- IFSC code of the bank branch

Step 2: IFSC Identifies the Bank Branch

The IFSC code helps the system identify the exact bank branch where the funds need to be sent. This ensures accurate routing and prevents errors.

Step 3: Transaction Is Processed Based on Transfer Type

- NEFT (National Electronic Funds Transfer):

Processes transactions in batches, making it suitable for regular transfers. - RTGS (Real-Time Gross Settlement):

Processes transactions individually in real time, typically used for high-value transfers that require immediate settlement. - IMPS (Immediate Payment Service):

Enables instant fund transfers 24/7, including weekends and holidays.

Step 4: Funds Are Routed Securely

Once the IFSC code is verified, the system routes the funds to the correct bank branch. If the IFSC is incorrect, the transaction may fail or get delayed.

Step 5: Transaction Completion

The transfer is completed under the supervision of the Reserve Bank of India (RBI), ensuring secure and reliable fund movement.

Where to Find an IFSC Code?

Finding the IFSC for your account is quite simple:

- Chequebooks: The IFSC is printed on the top of every chequebook.

- Bank statement: Most banks include the IFSC in their bank statements.

- Online banking portal: Branch-specific IFSC codes can be found on their official websites.

- Reserve Bank of India website: The RBI keeps a list of IFSC for all registered banks and branches to facilitate secure and reliable electronic transactions.

Importance of IFSC Code

The IFSC code is essential to modern banking, guaranteeing safe and precise transactions. It distinguishes a branch uniquely, making sure no one gets confused while sending funds, thus preventing fraud. IFSC help in making electronic payments faster and easier, thus reducing time for both banks and customers.

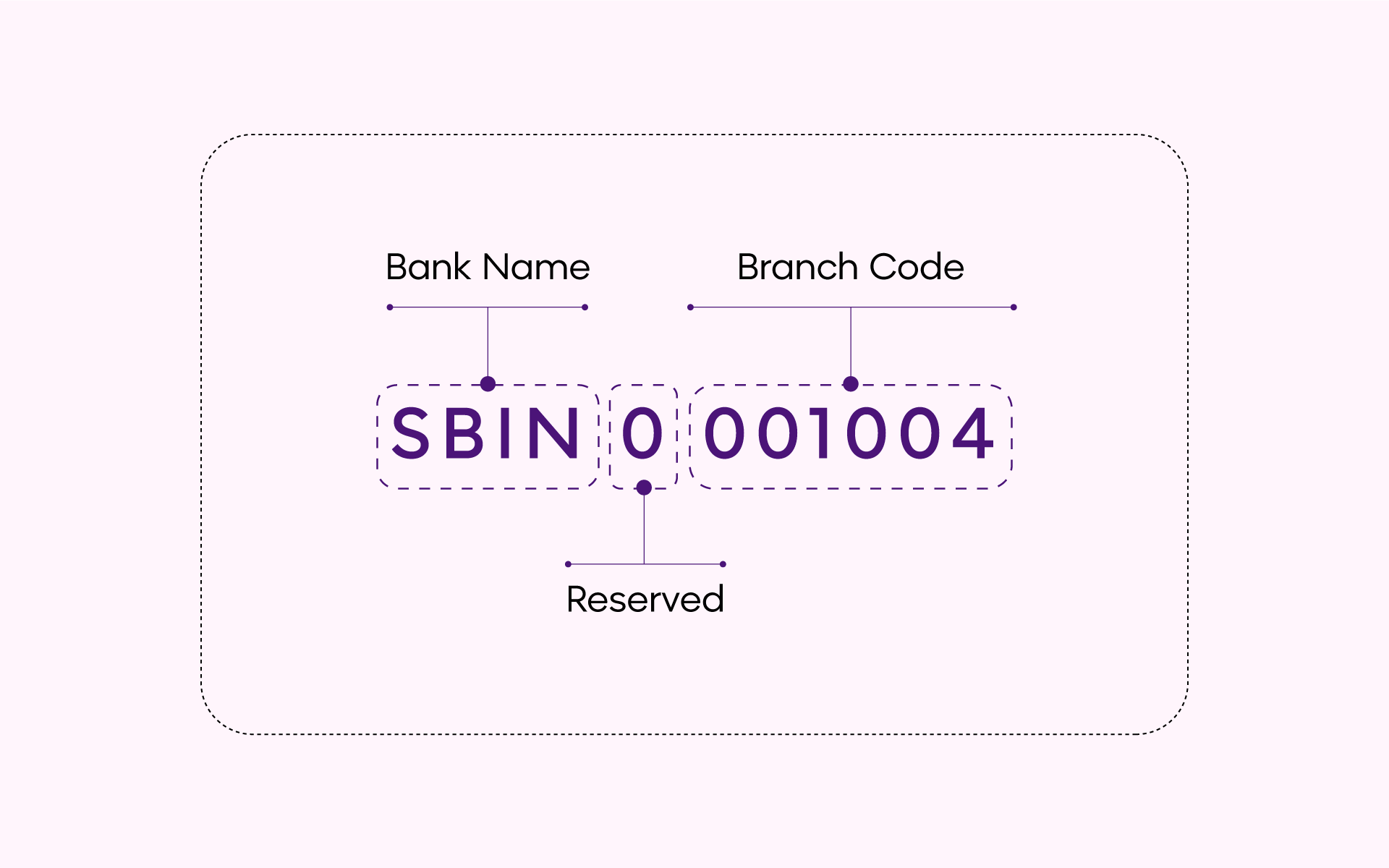

Structure of an IFSC Code

An IFSC code is carefully structured—each segment carries specific information about the bank and branch. It is not a randomly generated code.

Example IFSC Code: SBIN0001004

| Position | Characters | Meaning | Example |

| 1-4 | Bank Code | Bank Name (4 letters) | SBIN = State Bank of India |

| 5 | Zero (0) | Reserved for Future Use by RBI | 0 |

| 6-11 | Branch Code | Specific Branch (6 digits) | 001004 = Specific Branch Location |

Breakdown of Components:

First Four Characters (Bank Code): Represent the name of the bank in a 4-letter abbreviation.

- SBIN = State Bank of India

- HDFC = HDFC Bank

- ICIC = ICICI Bank

- AXIS = Axis Bank

- UTIB = Axis Bank

- UBIN = Union Bank of India

Fifth Character (Reserved Zero): Always a zero (0) and is reserved for future use by the Reserve Bank of India. This character maintains consistency in the code structure.

Last Six Characters (Branch Code): Represent the particular branch of the bank, typically in alphanumeric format, identifying the specific branch location.

- 001004 = Specific branch number

- Location-specific identifier

- Unique within each bank

Did You Know?

As of November 15, 2024, over 1,70,000 bank branches in India are enabled with Indian Financial System Codes (IFSC) to ensure precise and secure electronic fund transfers!

Conclusion

The IFSC code is an essential part of India’s banking system, ensuring online transactions are secure and accurate. Whether you are sending money, paying bills, or receiving money, it’s important to ensure that your funds reach the right destination. Understanding its structure and importance makes digital banking easier and helps you manage your finances effectively.

Today, business banking platforms like Open simplify how IFSC codes are used by auto-validating beneficiary details, reducing manual entry, and minimizing transaction errors—especially at scale.

As digital transactions grow, having the right systems in place can make all the difference in accuracy and control.

Explore smarter business banking with Open and simplify your payments workflow.

FAQs

1. What is the full form of IFSC?

IFSC stands for Indian Financial System Code.

2. How many digits/alphabets are there in the IFSC code?

An IFSC code is an 11-character alphanumeric code that is unique to each bank branch in India.

3. How can I find my IFSC code?

You can find your IFSC in your chequebook, online banking portals or even from the RBI official website.

4. Is the IFSC code required for online transactions?

Yes, the IFSC code is required for certain types of online transactions like NEFT, IMPS and RTGS.

5. What is the difference between an IFSC code and an MICR code?

An IFSC is a 11 character alphanumeric code used for fund transactions whereas an MICR code is a 9 digit code used for cheque clearance.

Visit open.money for more insightful content on banking and finance!

5. What is the difference between an IFSC code and an MICR code?

An IFSC is an 11-character alphanumeric code used for fund transactions, whereas an MICR code is a 9-digit code used for cheque clearance.