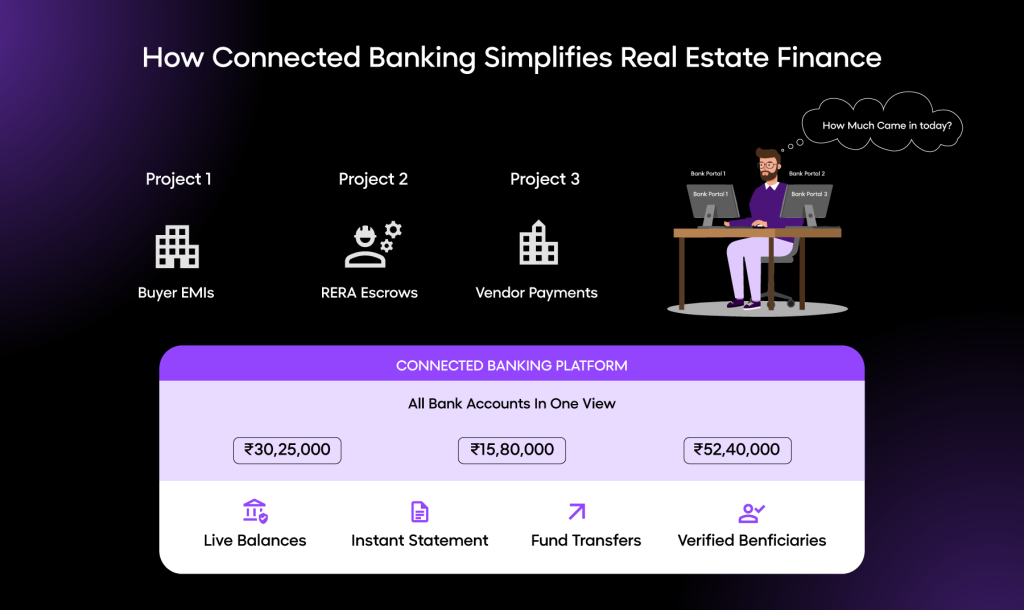

Three projects are running simultaneously. Buyer payments are landing across a dozen different bank accounts. A separate RERA escrow has to be maintained for each project. And somewhere in the middle of all this, a CFO is trying to answer one straightforward question:

How much actually came in today, and which project is it for?

For a growing real estate developer in India, this is not a crisis. It is a Tuesday morning.

The gap between what your bank portals show and what your business actually needs to know is not abstract. It shows up in delayed construction decisions, finance teams buried in reconciliation, and compliance risk that quietly compounds as your project pipeline grows. The infrastructure to close that gap exists, and this article explains exactly how it works.

Why Real Estate Treasury Management Is Uniquely Complex

Real estate development is structurally unlike most businesses when it comes to managing money. You are not collecting a subscription or settling a standard invoice. You are managing multiple payment types across multiple projects, each with its own compliance obligations, bank accounts, and reporting requirements.

On any given week, a mid-sized developer might be receiving:

- Booking amounts and token advances from new buyers—via NEFT, UPI, or home loan disbursals

- Construction-linked plan (CLP) instalments mapped to specific project milestones

- Bank loan disbursals into project-specific current accounts

- Vendor refunds and credit adjustments across different project entities

Layer RERA on top of this: at least 70% of every rupee collected from buyers must sit in a project-specific escrow account with a scheduled bank. Withdrawals are governed by certified milestone approvals from an engineer, an architect, and a chartered accountant. Every project is effectively its own financial system, and most developers are running several of them at once.

The result is a treasury operation that is fragmented by design. The question is whether your tools are built for it.

The Real Cost of Fragmented Banking

- 24–72 hour visibility lag before leadership has a reliable daily cash position.

- Finance teams manually reconciling inflows across multiple bank portals every day.

- RERA escrow thresholds tracked by hand—and compliance gaps discovered too late.

- Construction payments delayed because fund confirmations take too long.

- No consolidated view when reporting to lenders, boards, or investors.

The infrastructure to solve this already exists. It is called connected banking.

What Is Connected Banking for Real Estate Developers?

Connected banking does not replace your existing bank relationships. It connects them.

It sits across all your accounts—whether with HDFC, ICICI, SBI, Axis, Kotak, or any other scheduled bank and brings them into a single unified platform. For real estate developers, this means:

- All bank balances visible in one dashboard, updated in real time

- Statements and transaction history are accessible from one place, from the date of connection

- Fund transfers initiated directly from the platform—with a complete audit trail

- Beneficiary details managed centrally, with built-in account validation

Instead of logging into separate portals to reconstruct a daily cash position, your finance team works from a single source of truth. Reconciliation that once took hours now takes minutes. And leadership gets a live view of where every rupee sits across every project, every bank, every day.

How Open’s Connected Banking Works for Real Estate

Open is built for businesses that operate across multiple bank accounts and need unified financial control. Its Connected Banking layer is structured around four focused workflows.

1. Connected Bank Balances – Full Visibility, Instantly

All your bank accounts appear in one dashboard, each with a clear identifier name for the project or entity it belongs to. Open supports connectivity with ICICI, Yes Bank, Axis, SBI, Kotak, Standard Chartered, IDFC, HSBC, and HDFC through digital or offline onboarding. Every account, in one place.

2. Statements – Access On Demand, From Any Account

View and download statements or transaction history for any connected account filtered by credit, debit, date range, or account from the day of connection. No waiting on the bank, no manual requests. Ready when you need it for RERA filings, lender reports, or audits.

3. Transactions – Initiate and Track from One Place

Initiate payments directly from the platform. Select the source account, beneficiary, payment mode (NEFT, RTGS, or IMPS), and add remarks for context. Confirm with OTP. Every payment is logged in a dedicated transaction list, a searchable audit trail of every fund movement initiated through Open.

4. Beneficiaries – Centralised and Validated

All vendor and contractor accounts are saved centrally. Add a new beneficiary by entering the account number, and IFSC Open validates the bank details in real time. A display name makes payees easy to identify. No re-entry, no errors, no spreadsheets.

The RERA Compliance Layer: Why Real-Time Visibility Matters More Than You Think

RERA escrow compliance is one of the most operationally demanding requirements in Indian real estate. The mandate is clear: 70% of all buyer collections must be deposited into a project-specific escrow account, and withdrawals must be approved by three certified professionals: an engineer, an architect, and a chartered accountant.

In practice, most compliance issues do not arise from intent. They arise from visibility gaps. A batch of collections arrives a day late. A construction payment goes out based on yesterday’s figures. Without a real-time view of escrow balances across all projects, even well-managed finance teams can breach thresholds unintentionally and discover the problem only during a quarterly review or an audit.

Recent regulatory direction has moved clearly toward digital monitoring and API-enabled tracking for escrow compliance, reinforcing the expectation that developers have systems in place to track inflows and outflows continuously, not just periodically.

Connected banking directly addresses this. When all project accounts are visible in one platform, finance teams can monitor escrow balances daily, validate that collections are being routed correctly, and flag any threshold risk before it becomes a compliance problem.

What Real Estate Finance Teams Should Be Able to See—Every Day

→ Project-wise bank balances across all connected accounts

→ Daily collections vs. expected inflows by project

→ Outgoing payments with remarks and a complete audit trail

→ Validated beneficiary records ready for vendor payouts

→ Downloadable statements for RERA filings and lender reporting

Why This Matters More as Your Project Pipeline Grows

As developers scale, complexity increases in a predictable pattern: more projects, more buyers, more bank accounts, more compliance obligations. What cannot keep pace with that growth is manual effort.

The developers who manage this transition well are not the ones adding headcount to their finance teams proportionally. They are the ones building systems where one platform provides a complete, real-time picture across every account and every project, so decisions are made on current data, not yesterday’s reconciliation.

In one or two projects, fragmented banking is an inconvenience. At five or ten, it becomes a structural risk. Connected banking is how developers move from managing each project in isolation to running a portfolio with genuine financial clarity.

The Bottom Line

Real estate development in India has always been financially complex. Multiple banks, multiple projects, RERA obligations, and milestone-linked cash flows are not going away; they are the nature of the business.

What has changed is the availability of tools that can match that complexity. Connected banking gives developers something that was genuinely out of reach until recently: a single, real-time view of every bank account, every inflow, and every outgoing payment across all projects, from one platform.

The developers building this into their financial infrastructure today are not just solving a reconciliation problem. They are creating the operational foundation that allows them to take on more projects, manage compliance with confidence, and make faster, better-informed decisions at every stage of the development cycle.

If your finance team is still piecing together the daily cash picture from multiple portals, it is worth asking: What decisions are being made slowly or not at all because the visibility simply is not there?

Frequently Asked Questions

1. What is connected banking, and how is it different from my bank’s Netbanking portal?

Your bank’s NetBanking portal shows accounts within that one bank. Connected banking aggregates accounts across multiple banks into a single platform, giving your team a unified view of all balances, transactions, and statements, and the ability to initiate payments from one place.

2. Do I need to change my existing bank accounts to use connected banking?

No. Connected banking connects to your existing accounts; it does not replace them. Your RERA escrow accounts, project current accounts, and operating accounts stay exactly where they are. The platform adds a unified layer of visibility and control on top of your existing banking relationships.

Q3. Which banks are supported?

Open supports connectivity with ICICI, Yes Bank, Axis, SBI, Kotak, Standard Chartered, IDFC, HSBC, and HDFC, among others. Some banks connect digitally; others are onboarded through an assisted offline process. Your onboarding team will guide you through the right path for each bank.

Q4. How far back can I access transaction data once an account is connected?

Transaction data is available from the date of connection. This means your team can generate account-level statements for any period since onboarding—without depending on the bank to produce them, which is particularly useful for RERA quarterly filings, lender draw requests, and internal audits.

5. We manage projects through separate legal entities (SPVs). Can this work across entities?

Yes. Connected banking is designed to handle multi-entity structures. Open can aggregate accounts across multiple SPVs or legal entities, giving the leadership group-level visibility while keeping each entity’s accounts cleanly separated for compliance and reporting.