The Covid-19 pandemic has profoundly impacted the economy and placed gig and hourly wage workers at disproportionate risks. They are under a microscope and in the spotlight. This is because the job loss and financial insecurity during the pandemic have pushed people to seek new or additional sources of income. And this large influx of gig workers is largely unbanked or doesn’t have a stable source of income. As this market is highly untapped, it has attracted the attention of the banks to understand the needs and challenges and closely monitor the workings of the gig economy.

Economic uncertainties of the gig economy pose a considerable risk for most of the bigger banks, preventing them from extending their financial services. This is the core reason most mainstream financial institutions have not yet met the unique financial requirements of gig workers. This has led to opportunities for neobanks to develop and offer unique offerings to the gig economy.

The global gig economy’s estimated worth in 2021 was 347 billion dollars. According to the estimates of the Brodin.com survey, the gig economy is expected to grow from 204 billion dollars in 2018 to 455 billion dollars in 2023 at a Compound Annual Growth Rate (CAGR) of 17.4%.

This astronomical growth of the gig economy can be attributed to few developed and developing economies where the pandemic impacted livelihood the most. As of 2023, the US has 73.3 million gig workers, estimated to reach 90.1 million by 2028. In the United Kingdom, gig workers doubled to 4.7 million from what they were in 2019.

The questions now remain: what is this gig economy, why it is so lucrative, what are the challenges they face, and how neobanks are improving their lives? We will answer all these questions as you progress through the blog.

But if you want to jump directly into the topics:

[ez-toc]

What is the gig economy?

The gig economy is where independent contractors and freelancers replace full-time employees for temporary, flexible jobs with businesses. A gig economy breaks the notion of a traditional economy filled with full-time workers focused on career development. The gig economy runs on flexible, temporary, or freelance jobs, often connecting with clients or customers online.

The gig economy benefits gig workers, businesses, and consumers by making work more adaptable to gig workers’ momentary needs and flexible lifestyle demands. At the same time, the downside of a gig economy is the corrosion of traditional economic dynamics between employees and companies/clients.

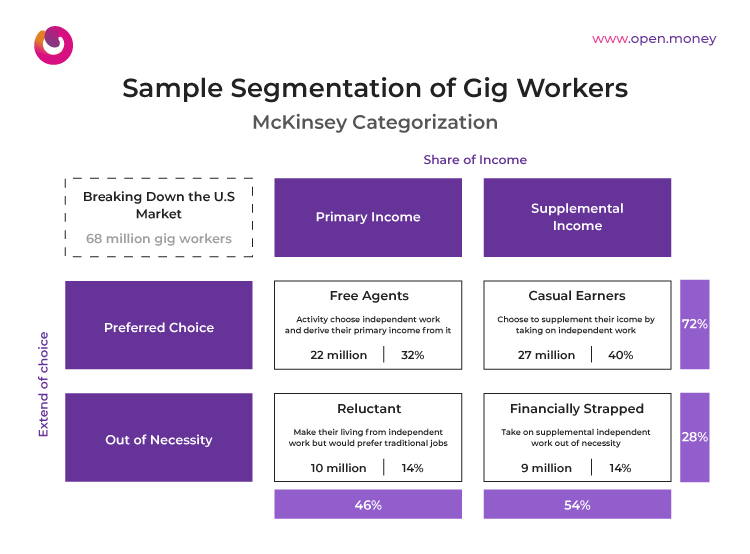

To understand the gig economy better, we can take a leaf out of the US in how they have segmented their gig workers.

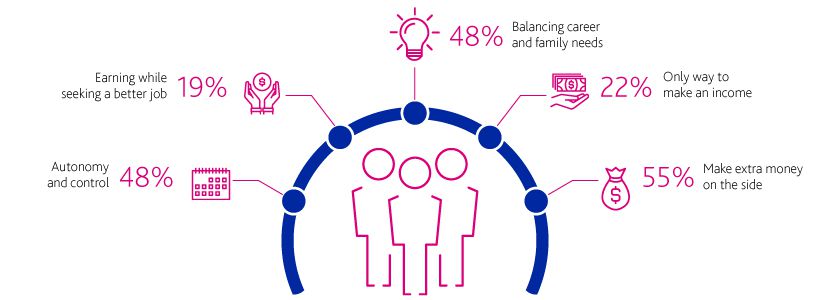

The count of gig workers increased because:

The count of gig workers increased because:

- People searched for alternate or new sources of income.

- Closure of large established businesses that had large employee bases.

- Rising unemployment due to restructuring of companies.

The gig economy has become a choice of income source given the more challenging times. What makes it lucrative is the freedom of lifestyle, and the control gig workers seek over how they want to spend the day. Even after gigs increased in popularity, one cannot deny the enormous challenges gig workers face. They have only come to the forefront now and are visible more vividly.

Financial challenges of the gig workers

The gig economy has grown at an alarming rate during the pandemic for various reasons, but gig workers’ financial challenges haven’t changed over the years. The sudden growth spurt of gig workers or the gig economy has brought these issues to the forefront.

In the words of Zack Smith, CEO of Jobble (A gig worker marketplace),

” Gig and hourly workers stepped up behind the scenes across the nations, keeping warehouses stocked, delivering goods, and helping people stay safe at home.”

Emphasizing the problem gig workers face, Smith continues,

“Many gig workers are underbanked and lack access to resources that can grow their financial wellness. From savings and investment accounts to reliable access to their funds, gig workers deserve to be served like the hard workers they are. Many also lack benefits or access to programs that can keep them healthy and supported.“

Here are some of the financial challenges that the gig economy faces:

1. High cross-border currency exchange and transaction fees

Historically, international payments have been slower and more expensive than local transactions. The delays and conversion cost hurt gig workers; businesses must circumvent these issues to keep workforces happy and avoid costly churn.

- High forex fees: Currency conversions incur fees, creating a headache and reducing gig workers’ margins.

- High transaction fees: Gig workers’ margins are further reduced by the disproportionate impact of transaction fees, especially on small value transactions.

- Volatile exchange rates: The volatility of exchange rates is also a problem, with fluctuations delaying payments and reducing value for the recipient.

2. Complex international taxation and regulations

The legal status of gig workers varies from country to country. Global businesses need to handle regulatory nuances and flex around local legal requirements. Companies must keep in mind:

- Contractor vs. employee status: This year, the UK and Spain have reclassified Uber drivers as Uber employees, giving them additional rights and benefits. If other countries follow suit, gig employers must catch up with the trends and develop something better.

- Tax requirements: Uncertainty of the legal status of gig workers can leave companies unsure of their tax liabilities and juggle payments across various jurisdictions. It creates a dangerous situation since they may breach the law by inadvertently withholding benefits.

- International payments: Unfamiliarity with regulations can increase the chance of problems arising around international payments. It elevates the probability of transfer mistakes, leading to delayed or dropped payments and worker frustration.

3. Cultural differences and worker preference

Workers, irrespective of wherever they are, want faster and consistent payments free from extra charges. But each worker across multiple geographies has different expectations and preferences for payment methods that gig employers should understand and address. Businesses must consider:

- Faster payments: Gig workers do not have a steady cash flow, and your irregular payments can restrict them, so having minimal delays is vital to avoid unnecessary stress. In a survey, two out of three gig workers said they would work extra in the gig economy if businesses could assure them of faster payments.

- Banking the unbanked: Developing economies have more workers relying on cash payments, making fast transfers a tough choice. They rarely have bank accounts with e-banking services. Electronic wallets and virtual cards have gained popularity, minimizing cross-border payment issues. Thus, making international transfers almost at par with the local payments.

- Payment preferences of the gig workers: In Europe and the USA, direct-to-bank payments are preferred, but they’re still slow and expensive due to a lack of proper payment infrastructure. In some places, gig workers prefer other payment methods, such as digital wallets or virtual cards. Businesses relying on gig workers need to listen to workers’ voices and address their needs with an offering of a range of payment options to fit.

The challenges of the gig economy are many and varied. The neobanks have stepped up their efforts in making banking effortless for the gig workers by empowering them with essential banking and lending services. These services have become the bedrock of the gig economy’s financial stability.

How are neobanks helping gig workers in managing their finances?

The pandemic made gig work a primary source of income for many who viewed it as a side hustle or supplement to the reduced income. This type of transition can only mean people are trying to adapt to the loss of benefits, plus there is an increase in income fluctuations.

However, uncertainty in income sources and cash flow makes it difficult for the traditional banks to serve the gig workers with consumer loans and mortgages. The gig workers chose the neobanks after seeing conventional banks’ unavailability during their times of need. Therefore, to cater to the financial needs of the gig workers, neobanks have stepped up to provide various solutions. They are:

Advances on Paychecks

In recent years, fintech providers have offered benefits to gig workers through all types of advances on paychecks. These are short-term loans on the future salary agreed by an employer and the employee (gig worker in this case). The employee agrees to pay off the loan through deductions from future wages. These are the optional benefits that can help gig workers in their emergencies.

Instant Cross-Border Payments

Some platforms offer instant cross-border payments for gig workers to instantly receive remuneration from their employers across borders. Boundaries do not limit gig work, but cross-border payments are a highly regulated space for their inherent reasons (fraud and money laundering, interbank payments regulations like SWIFT, etc.).

The neobanks have established relations with various countries’ real-time payments infrastructure and SWIFT’s Global Payment Initiative Instant (GPI- Instant). With GPI-Instant, the banks can easily track and manage payments. It empowers the gig workers to get paid and settle the accounts with their employers settled abroad quickly.

Visa Business Cards for Freelancers

Some neobanks also empower the gig workers with VISA business cards to manage their expenses. The gig workers subscribe to various tools and tech for making their work easier. They usually pay it from their accounts, separating business from personal expenses a mess. A VISA business card with in-built expense management can help them track and manage their business expenses. Moreover, VISA card is accepted universally across the globe, making it easier for gig workers to make cross-border payments.

Tax Compliant invoices with an integrated payment link

Many freelancers design or pay for tools to create invoices compliant with the tax authority guidelines. Apart from tracking and managing expenses, generating tax-compliant invoices consume a lot of time for gig workers. They get access to localized tax regulatory compliant invoices with in-built payment links for hassle-free payouts.

Auto-Accounting and integrated payment gateway

Additional features such as automated accounting and integrated payment gateway can make the life of gig workers easier. Integrated payments gateway helps gig workers to get remunerations from employers against invoices directly without sharing any account-related details. Automated accounting enables gig workers to manage their accounting sheets automatically as they make payments and generate invoices. I also auto reconciles invoices by tracking bank payments which is an excellent help during taxation. They do not need to do the tedious task of matching the transaction with invoices manually and then share it with their accountants.

Overall, the neobanks are trying to create a healthy financial ecosystem for the largely unbanked gig workers and lessen their struggle with funding, taxation, and regulations.

Conclusion

Shutting down of businesses and people searching for alternative sources of income pushed the gig economy’s growth across the globe during the pandemic. G g workers were already reeling under financial stress, but financial institutions didn’t focus on these issues.

However, the sudden growth spurt in the count of gig workers has made them hotcakes of investments by banks. T e neobanks are trying to provide faster cross-border payments, industry-regulated invoicing and accounting solutions, secure payment gateways, lower the high transaction fees, and much more. Many neobanks have made strides in giving gig workers a better life.

The gig workers primarily suffer from volatile income, the cost that they pay for seeking freedom. T is volatility also prevents large banks from focusing on such niche markets. The question now remains how far are the neobanks willing to go for the gig workers to offer them better financial security. That, only the time will reveal.